B. Lending and credit activities

Table 2.3: Loan balance table of NCB - Hai An Branch

Unit: Million VND

Target

2017 | 2018 | 2019 | ||||

Balance | (%) | Balance | (%) | Balance | (%) | |

Total outstanding debt loan | 1,626,206 | 100% | 1,918,562 | 100% | 1,815,391 | 100% |

Short Loan limit | 1,392,481 | 85.6% | 1,640,879 | 85.5% | 1,544,173 | 85.1% |

Loan by VND | 1,372,145 | 84.4% | 1,611,763 | 84.0% | 1,521,056 | 83.8% |

Loan by foreign currency | 20,336 | 1.3% | 29,116 | 1.5% | 23,117 | 1.3% |

Loan medium, long term | 233,725 | 14.4% | 277,683 | 14.5% | 271,218 | 14.9% |

Loan by VND | 181,611 | 11.2% | 210,442 | 11.0% | 210.104 | 11.6% |

Loan by foreign currency | 52,114 | 3.2% | 67,241 | 3.5% | 61,114 | 3.4% |

Maybe you are interested!

-

Some Business Performance Results of the Branch

Some Business Performance Results of the Branch -

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1 -

Business Performance of the Company in the Period 2009–2011 Table 2.1. Business Results of Viet Holiday Travel Company

Business Performance of the Company in the Period 2009–2011 Table 2.1. Business Results of Viet Holiday Travel Company -

Company's Business Performance Results for 3 Years (2018-2020)

Company's Business Performance Results for 3 Years (2018-2020) -

Production and Business Performance Results of La Nga Forestry Company Limited

Production and Business Performance Results of La Nga Forestry Company Limited

(Source: NCB Accounting Balance Sheet – Hai An Branch)

Looking at the table above we see:

- Outstanding loans increased unevenly from 2017 to 2019. In 2018, outstanding loans were VND 1,918,562 million, an increase of VND 292,356 million compared to 2017.

- In 2019, outstanding debt reached VND 1,815,391 million, down VND 103,171 million compared to 2018.

- The increase in outstanding loans in 2018 - 2019 shows that the Bank's lending has had good results. The increase in lending will increase the Bank's profits. However, in 2019, outstanding loans decreased significantly, showing that NCB has not had the right solution or direction to increase lending capital.

In terms of loan structure:

- By term: short-term loans always account for a larger proportion of total outstanding loans. Specifically, in 2017, short-term loans accounted for 85.6%, medium and long-term loans were 14.4%. In 2018, short-term loans accounted for 85.5%, medium and long-term loans were 14.5%. In 2019, short-term loans accounted for 85.1%, medium and long-term loans were 14.9%.

- By currency: VND loans always account for a large proportion of both short-term, medium-term and long-term loans compared to foreign currency loans.

- In general, credit quality is guaranteed. Although the bank's business operations still face many difficulties, NCB's lending activities

– Hai An branch in the period 2017 - 2019 is showing a downward trend but not too much.

C. Business performance

Table 2.4: Business performance of NCB – Hai An Branch

Unit: Million VND

Target

2017 | 2018 | 2019 | Compare years 2018/2017 | Compare years 2019/2018 | |||

Amount | Amount | Amount | Amount | (%) | Amount | (%) | |

Total revenue | 208,666 | 221,418 | 217,880 | 12,752 | 6.11% | -3.538 | -1.6% |

Total cost fee | 187,514 | 198.125 | 199,145 | 10,611 | 5.66% | 1,020 | 0.5% |

Profit before tax | 21,152 | 23,293 | 18,735 | 2.141 | 10.12% | -4.558 | -19.6% |

(Source: NCB's business results table - Hai An Branch)

Through the table above, we can see that the total revenue of Hai An branch has an unstable increase trend over the years. In 2018, total revenue reached 221,418 million VND, an increase of 12,752 million VND (equivalent to 6.11%) compared to 2017. In 2019, the total revenue of the branch decreased by 1.6% to 217,880 million VND. The decrease in income is due to a sharp increase in mobilized capital while credit activities have a decrease in loan sales; but in return

In addition, revenue from banking services increased, helping the Branch ensure profits in 2019.

The branch's pre-tax profit has been unstable over the past three years. In 2018, the branch's profit increased by VND 2,141 million (equivalent to 10.12%) compared to 2017. By 2019, the pre-tax profit had decreased by VND 4,558 million (equivalent to a decrease of 19.6%) compared to the profit in 2018.

2.2. Analysis of the current status of capital mobilization activities at National Citizen Commercial Joint Stock Bank - Hai An Hai Phong Branch

2.2.1 Overview of capital mobilization fluctuations of NCB – Hai An Hai Phong

Capital is very important in commercial banks as well as the National Bank, capital mobilization is very important to the bank. To ensure business development, the Bank needs a strong capital base. Because in order to conduct business, lending and investment, the Bank mainly takes from capital mobilization activities. The Bank's motto is "borrowing to lend", diversifying capital sources by diversifying forms of mobilization, measures, and channels of capital mobilization from all sources in all socio-economic sectors.

National Citizen Bank - Hai An Hai Phong Branch has implemented its operational direction well and continuously achieved high results. The transaction office conducts capital mobilization activities through the following forms:

- Mobilizing capital from people's savings deposits

- Mobilizing capital from deposits of economic organizations

- Capital mobilization from issuing valuable papers

- Mobilizing capital from other sources

Graduation thesis

Table 2.5: Structure of mobilized capital of NCB – Hai An Hai Phong

Unit: Million VND

STT

Target | 2017 | 2018 | 2019 | ||||||||

Amount | Ratio weight | Amount | Ratio weight | Amount | Proportion | Amount | % | Amount | % | ||

Total capital mobilized | 1,610,568 | 100% | 2,050,822 | 100% | 2,265,041 | 100% | 440,254 | 27.3% | 214,219 | 10.4% | |

I | By term | ||||||||||

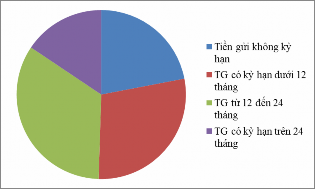

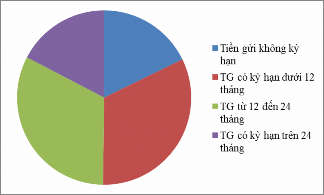

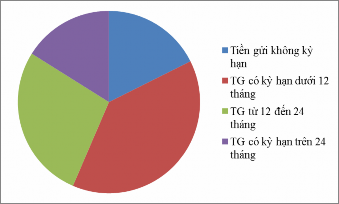

1 | Deposit no term | 354.145 | 22.0% | 364,714 | 17.8% | 399,147 | 17.6% | 10,569 | 3.0% | 34,433 | 9.4% |

2 | Term Deposit under 12 months | 459,099 | 28.5% | 664,855 | 32.4% | 879,897 | 38.8% | 205,756 | 44.8% | 215,042 | 32.3% |

3 | Age from 12 to 24 month | 546,214 | 33.9% | 665.141 | 32.4% | 621,441 | 27.4% | 118,927 | 21.8% | (43,700) | -6.6% |

4 | Term Deposit over 24 months | 251,110 | 15.6% | 356.112 | 17.4% | 364,556 | 16.1% | 105,002 | 41.8% | 8,444 | 2.4% |

II | By subject | ||||||||||

1 | Residential deposits | 1,058,441 | 65.7% | 1,204,112 | 58.7% | 1,401,223 | 61.9% | 145,671 | 13.8% | 197.111 | 16.4% |

2 | Institutional deposits Economy | 502.103 | 31.2% | 791,351 | 38.6% | 798,471 | 35.3% | 289,248 | 57.6% | 7,120 | 0.9% |

3 | Money from papers have price | 2,514 | 0.2% | 3.012 | 0.1% | 3,651 | 0.2% | 498 | 19.8% | 639 | 21.2% |

4 | Deposits of the credit institution | 47,510 | 2.9% | 52,347 | 2.6% | 61,696 | 2.7% | 4,837 | 10.2% | 9,349 | 17.9% |

( Source: NCB Summary Report – Hai An Hai Phong)

Chart 2.1. Deposit structure by term in 2017

Chart 2.2. Deposit structure by term in 2018

Chart 2.3. Deposit structure by term in 2019

Through the table of data on capital structure, we see:

Demand deposits in 2018 increased by 3% compared to 2017 and in 2019 increased by 9.4% compared to 2018. The reason for the sharp increase in demand deposits in 2019 compared to the previous year was mainly through businesses and organizations paying income to employees and partly due to the deposit needs of the population.

The most numerous and higher-growing term deposits are term deposits under 12 months. In 2018, 12-month term deposits increased by 44.8% compared to 2017.

compared to 2017 but by 2019 increased by 32.3% compared to 2018. Because the amount of money that customers deposit for a 12-month term has a time quite suitable for the needs of residents and businesses due to the average time with the savings deposit period, flexibility and high interest rates.

The deposits that the bank mobilizes the most are from socio-economic organizations and from residents. The average annual rate of deposits from residents has increased steadily over the past 3 years and has a fairly stable trend. Although the mobilized capital is not a major source of loan capital, it has decreased every year, in 2018 it decreased by 19.8% compared to 2017, in 2019 the amount of capital mobilized from this source increased by 21.2% compared to 2018. However, the value of this type of capital compared to the total mobilized capital of the Branch is still quite limited.

Residential deposits still account for a large proportion of the total mobilized capital of the Branch and have tended to increase steadily over the past three years with a value increasing steadily over 140 billion VND each year. This shows that the Branch's capital mobilization capacity is quite stable and that the Branch has done a good job of promoting and attracting deposits from residents.

2.2.2 Analysis of capital mobilization activities from residential deposits

Looking at Table 2.5, residential deposits from 2017 to 2019 increased from 13.8% to 16.4%. This is an encouraging number when the amount of savings of people trust to deposit at NCB - Hai An Hai Phong. In 2018, the amount of savings of people increased by 145,671 million VND (equivalent to an increase of 13.8%) compared to 2017; by 2019, this number increased to 197,111 million VND (equivalent to an increase of 16.4%) compared to 2018. NCB - Hai An Hai Phong based on many years of operating experience in the area, proposed solutions to mobilize at each time in a reasonable way so that capital is concentrated in the Bank. The bank has based on the ceiling lending interest rate of the State Bank, increasing interest rates in stages such as in March 2019, the bank interest rate was 7.23%/year for 6-month deposits, but at the same time in March 2018, the 6-month interest rate of NCB - Hai An Hai Phong mobilized was 5.8%. This has helped the bank mobilize more capital from the people. In addition, NCB - Hai An Hai Phong coordinated with local authorities to mobilize individuals

Resettlement workers receive compensation money but have not used it to save. That is a way to help people make a profit and spend money more scientifically. NCB - Hai An Hai Phong Branch also actively establishes relationships with individuals who are production and business households, retirees, and deploys each product and service on mobilizing savings. Complete the list of customers who open deposit accounts at the transaction office and customers who deposit savings with large balances to assign tasks to each employee to manage, monitor and have a good care plan.

2.2.3 Analysis of capital mobilization activities from deposits of economic organizations

Looking at Table 2.5, deposits from economic organizations increased sharply from 2018 but by 2019 only increased by a small percentage and tended to be stable. This is the largest amount of capital mobilized in the total number of subjects that NCB - Hai An Hai Phong mobilized capital.

In 2018, the amount of capital mobilized from economic organizations was 1,204,112 million VND, an increase of 289,248 million VND (equivalent to 57.6%) compared to 2017; in 2019, it reached 1,401,223 million, an increase of 7,120 million VND (equivalent to an increase of 0.9%). Realizing that many cash receipts from businesses and social organizations will be paid within a specified period, due to convenient payment deposits but low interest rates, NCB - Hai An Hai Phong has offered flexible monthly term interest rates such as 5.9%/year for 3 months; 6.5%/year for 6 months; 7.1%/year for 9 months to encourage organizations and businesses to deposit money at NCB - Hai An Hai Phong. This is a creative factor that NCB - Hai An Hai Phong has attracted many idle savings sources of enterprises and economic organizations to increase more diverse business capital.

2.2.4 Analysis of capital mobilization activities from issuing valuable papers

Looking at Table 2.5, although the issuance of valuable papers is a form of capital mobilization that has existed for a long time, the amount mobilized from this source is lower than other capital mobilization components of the Branch. In 2018, capital mobilization from the issuance of valuable papers was VND 3,012 million, an increase of VND 498 million compared to 2017 (equivalent to 19.8%). In 2019, the mobilization reached VND 3,651 million, an increase of VND 639 million, corresponding to

with an increase of 21.2% compared to 2018. Issuing valuable papers is a fairly easy and convenient capital mobilization solution for National Citizen Commercial Joint Stock Bank - Hai An Hai Phong Branch. However, from an academic perspective, because the issuance of valuable papers is a new type of transaction that has recently appeared in our country, there are still very few legal studies on this issue. This makes it very difficult to correctly perceive the legal nature of the transaction of issuing valuable papers at NCB - Hai An Hai Phong.

2.2.5 Analysis of capital mobilization activities from other sources

In addition to the above forms of mobilization, NCB - Hai An Hai Phong also mobilizes deposits from other credit institutions such as Vietinbank, Vietcombank, Agribank... to increase its missing capital to ensure liquidity, reserves, and urgency. This is the third largest mobilization of NCB - Hai An Hai Phong after deposits from economic organizations and residents. On average, each year, deposits from credit institutions increase by 10.2% to 17.9%. In 2018, the amount mobilized from credit institutions was 47,510 million VND; an increase of 4,837 million VND, corresponding to an increase of 10.2% compared to 2017; by 2019, the amount mobilized was 61,696 million VND, an increase of 9,349 million VND compared to 2018, corresponding to 17.9%.

2.3 Analysis of indicators reflecting the efficiency of capital mobilization at National Citizen Commercial Joint Stock Bank - Hai An Hai Phong Branch

To have an accurate and comprehensive assessment of a commercial bank’s capital mobilization, it is indispensable to provide criteria for evaluating this activity. When considering the effectiveness of capital mobilization, we can evaluate based on the following main indicators:

- Capital scale and growth rate of mobilized capital

- Cost of capital mobilization

- Ability to meet capital needs

2.3.1 Capital scale and growth rate of mobilized capital

To analyze the capital mobilization efficiency of NCB - Hai An Hai Phong, we will first base on the scale of capital mobilization, shown through the indicator: Capital mobilization plan completion rate (TLHTKHHĐV).

Actual amount of capital mobilized | ||

TLHTKHHĐV | = | Mobilization plan |

We will consider the capital mobilization ratio of NCB - Hai An Hai Phong through the following data table:

Table 2.6: Mobilized capital of NCB - Hai An Hai Phong

Unit: Million VND

Target

2017 | 2018 | 2019 | |

Plan | 1,550,000 | 1,950,000 | 2,000,000 |

Perform | 1,610,568 | 2,050,822 | 2,265,041 |

Plan completion rate (%) | 104% | 105% | 113% |

( Source: NCB Summary Report - Hai An Hai Phong)

The completion rate of the capital mobilization plan is always over 100%, which means that the Bank Branch has completed the capital mobilization plan according to the plan at the beginning of the year. According to the data from Table 2.6 above, we can see that the completion rate of the capital mobilization plan is always greater than 100%. This shows that the Branch has tried to carry out capital mobilization work, expanding its capital sources by diversifying forms, measures, and capital mobilization channels from all sources in all economic sectors. Despite market fluctuations and high plans, the result of capital mobilization always exceeds the set plan.

Specifically, in 2017 it reached 104%, in 2018 it reached 105%, in 2019 it reached 113% compared to the set plan. With such a plan completion rate, it shows that the source planning work did not accurately forecast the amount of capital that could be mobilized by NCB - Hai An Hai Phong and the amount of capital mobilized to meet the bank's capital needs in the years.

As a financial intermediary providing capital to the economy in the form of loans and investments, banks understand the importance of finding capital sources for themselves. NCB - Hai An Hai Phong has attached great importance to capital mobilization and considered capital as the first element of business activities and also the decisive factor for the existence and development of the bank. When the mobilized capital has a reasonable structure, low mobilization costs will contribute to improving the operational efficiency of the bank.

Growth rate of mobilized capital

As analyzed, the bank's capital mobilization activities still maintain an annual growth rate. Thereby, it can be assessed that the capital mobilization efficiency is quite good. However, the efficiency of capital mobilization activities is not only reflected in the increase or decrease of mobilized capital but also in many other factors that we need to consider such as capital structure and the ability to meet capital needs.

2.3.2 Cost of capital mobilization

Effectively mobilized capital not only meets the business needs of the bank but also has to be a source of capital with low mobilization costs. Mobilization costs include: deposit interest costs, loan interest costs, securities issuance costs, management costs, of which the main ones are deposit interest costs and securities issuance costs. In which, interest rates directly affect the fluctuations of mobilized capital as well as the speed of borrowing, thereby affecting the business results of the bank. Because mobilization costs are so important, in business activities, banks need to find solutions to reduce costs.

Table 2.7: Capital mobilization costs of NCB - Hai Phong

Unit: Million VND

Target

Year 2017 | Year 2018 | Year 2019 | 2018/2017 | 2019/2018 | |||

+ (-) | % | + (-) | % | ||||

Total cost of capital mobilize | 54,214 | 62,014 | 78,142 | 7,800 | 5.1% | 6.128 | 10.0% |

In which: Interest expense mobilize | 45,124 | 57,146 | 64,774 | 2,022 | 8.3% | 7,628 | 4.9% |

( Source: NCB Summary Report – Hai An Hai Phong)

In general, capital costs increased over the years, in 2018 they increased by 5.1% compared to 2017. In 2019, due to the large increase in mobilized capital compared to 2018, the total cost of mobilized capital also increased by about 10%. In the total cost, the main cost is interest payment, usually accounting for more than 90%. In 2018, interest costs increased by 12,022 million VND, equivalent to an increase of 8.3% compared to 2017. In 2019, interest costs continued to increase by 7,628 million VND, equivalent to a rate of 4.9%. The increase in costs shows the increase in mobilized capital in the 3 years 2017 - 2019 due to the need to increase capital for economic development, so capital mobilization activities also increased. In addition, the increase in costs in recent years is also due to the increase in interest rates in the market. Therefore, banks must have an interest rate policy that is consistent with the development of the market, compensating for the level of inflation and attracting capital mobilized in the economy.

In addition to bank interest expenses, there are other expenses such as management expenses, advertising expenses, risk provisions, etc. Although it only accounts for a small part of the total expenses, it also affects the revenue results. Especially in the current competitive period, banks compete to implement promotional programs, compete to mobilize capital, causing costs to increase. In fact, the cost growth rate of NCB - Hai An Hai Phong is very low, so the bank needs to promote and control costs so that they are at such a low level every year, then the bank can ensure its operational capacity.

To attract deposits, the Bank offers quality products and services and constantly innovates products to create convenience for customers. The Bank also offers many forms of interest payment such as: post-interest payment, pre-interest payment, periodic interest payment... In which, post-interest payment is the most popular form. Interest rates are constantly fluctuating over different periods, mainly for foreign currencies. And the Bank needs to choose the right form of mobilization with low cost to ensure the goal of maximizing the owner's profit.

2.3.3 Ability to meet capital needs

In fact, not only the growth in scale, the structure of capital sources in general and mobilized capital sources in particular can fully assess the effectiveness of capital mobilization at the bank. If the bank mobilizes a lot of capital but uses little, it will lead to capital stagnation. On the contrary, if the capital mobilization is small but the capital use is high, the risk for the bank will be very high. At that time, the bank will find measures to limit risks such as borrowing from other credit institutions or the State Bank, the State Treasury...

This shows that even when the Bank mobilizes a lot of capital, the business efficiency is still not high and to achieve efficiency, the Bank must harmoniously combine the mobilized capital with the lending capacity. In the Bank's operations, lending is the most and the interest income from lending is the largest. Besides, there are also investment activities but they account for a very small proportion.

Graduation thesis

Table 2.8: Situation of using mobilized capital

Unit: Million VND

Target

2017 | 2018 | 2019 | 2018/2017 | 2019/2018 | |||

+ (-) | % | + (-) | % | ||||

Total capital mobilized | 1,610,568 | 2,050,822 | 2,265,041 | 440,254 | 27.3% | 214,219 | 10.4% |

1. Non-term deposits | 354.145 | 364,714 | 399,147 | 10,569 | 3.0% | 34,433 | 9.4% |

Ratio to total mobilized capital | 22.0% | 17.8% | 17.6% | -4.2% | -0.2% | ||

2. Term deposits | 1,256,423 | 1,686,108 | 1,865,894 | 429,685 | 34.2% | 179,786 | 10.7% |

Ratio to total mobilized capital | 78.0% | 82.2% | 82.4% | 4.2% | 0.2% | ||

- Term deposits under 12 months | 459,099 | 664,855 | 879,897 | 205,756 | 44.8% | 215,042 | 32.3% |

- Term deposits over 12 months | 797,324 | 1,021,253 | 985,997 | 223,929 | 28.1% | (35,256) | -3.5% |

Total outstanding loans | 1,626,206 | 1,918,562 | 1,815,391 | 292,356 | 18.0% | (103,171) | -5.4% |

1. Short-term loans | 1,392,481 | 1,640,879 | 1,544,173 | 248,398 | 17.8% | (96,706) | -5.9% |

2. Medium and long term loans | 233,725 | 277,683 | 271,218 | 43,958 | 18.8% | (6,465) | -2.3% |

Debt to Equity Ratio | 1,010 | 0.936 | 0.801 | -0.074 | -0.134 | ||

1. Short term (times) | 1,712 | 1,594 | 1,207 | -0.119 | -0.386 | ||

2. Medium and long term (times) | 0.293 | 0.272 | 0.275 | -0.021 | 0.003 | ||

( Source: NCB Summary Report - Hai An Hai Phong)

The table shows that the term structure of the Bank's deposit sources has been gradually increasing over the years (in 2018, it increased by 34.2% compared to 2017, in 2019, it increased by 10.7% compared to 2018) and non-term capital has also increased but at a slower rate than term deposits (in 2018, it increased by 3% compared to 2017, in 2019, it increased by 9.4% compared to 2018). Term deposits account for 78% to 82.4% of the total mobilized capital of the Branch. In terms of finance, this is favorable for the Bank.

Because term deposits are a source with high interest rates when there is a need for medium and long-term capital, term deposits meet all the needs and help the Bank plan to lend to customers and also plan to pay deposits of depositors. This proves that the reputation of NCB - Hai An Hai Phong is high, so the number of term deposits accounts for a large part of the total capital mobilized by the transaction office. However, the bank should also have measures to attract more non-term deposits to reduce interest costs and increase profits for the transaction office.

The effectiveness of capital mobilization activities is also reflected in the rationality and balance between capital mobilization and capital use. The main activity of the bank, lending from mobilized capital accounts for the largest proportion.

Table 2.9: Relationship between capital use (lending) and capital mobilization

Target

2017 | 2018 | 2019 | 2018/2017 | 2019/2018 | |||

+ (-) | % | + (-) | % | ||||

Outstanding debt | 1,626,206 | 1,918,562 | 1,724,704 | 292,356 | 18% | (193,858) | -10.1% |

Total capital mobilized | 1,610,568 | 2,050,822 | 2,265,041 | 440,254 | 27.3% | 214,219 | 10.4% |

Outstanding/Total Capital mobilized (%) | 100.97% | 93.55% | 76.14% | -7.42% | -17.41% | ||

( Source: NCB Summary Report – Hai An Hai Phong)

The total outstanding debt of NCB - Hai Phong from 2017 - 2019 tended to fluctuate and be unstable. In 2018, outstanding loans increased sharply due to the investment needs and expansion of business operations, causing the Branch's credit growth to increase dramatically from the outstanding debt of 2017 of VND 1,626,206 million to VND 1,918,562 million in 2018 with an increase of VND 292,356 million (or an increase of 18%) compared to 2017. In 2019, the total outstanding debt decreased by 10.1% compared to 2018, corresponding to a decrease of VND 193,858 million. The Branch has proactively sought, exploited, and selected customers with healthy financial status in terms of capital, while regularly monitoring the production and business situation and analyzing the financial situation of borrowing enterprises. Outstanding loans tended to increase in 2018 but decreased in 2019. The ratio of outstanding loans/mobilized capital over three years tended to decrease from 100.97% to 76.14%. This shows that although outstanding loans increased and decreased unsteadily, the level of capital mobilization tended to grow steadily and was continuously expanded much larger than credit activities. Therefore, the ratio of outstanding loans/mobilized capital, on average from 2017 to 2019, decreased quite sharply. In 2017, mobilized capital was not enough for credit activities, due to the very hot growth of credit in 2017. To meet the capital for credit, the Branch had to call for internally transferred capital to support credit disbursement. However, in 2018 and 2019, capital mobilization activities increased rapidly, enough to meet the capital needs of Hai An Hai Phong Branch and achieve the mobilization target set by the Head Office.

The general assessment shows that the branch's capital mobilization activities are relatively effective. All indicators have a fairly good growth rate, each year is higher than the previous year. Besides the achieved results, the transaction office also has many limitations.

2.4 Evaluation of capital mobilization efficiency of National Citizen Commercial Joint Stock Bank - Hai An Hai Phong Branch

2.4.1. Results achieved

On the basis of making the most of resources and opportunities, National Citizen Bank in general has operated quite effectively in all aspects, finance, business operations,