- Then, send it to the company director for signature and stamp. The payment order is sent to the bank during working hours.

- This transaction is recorded as follows: Debit account 635: 28,350,598

Credit account 1121: 28,350,598

At the end of the month, the accountant transfers the financial expenses of the month to account 911 to determine the business results:

Debit account 911: 28,350,598

Credit account 635: 28,350,598

Account 112

General accounting diagram

Account 635 Account 911

28,350,598 (635) | 28,350,598 (635) |

| 28,350,598 (635) | ||

28,350,598 | 28,350,598 |

Maybe you are interested!

-

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1 -

Completing revenue accounting and determining business results at Ha Lam Coal Joint Stock Company - Vinacomin - 16

Completing revenue accounting and determining business results at Ha Lam Coal Joint Stock Company - Vinacomin - 16 -

Completing revenue and cost accounting and determining business results at Nakashima Vietnam Co., Ltd. - 14

Completing revenue and cost accounting and determining business results at Nakashima Vietnam Co., Ltd. - 14 -

Accounting for revenue, expenses and determining business results at Saigon Real Estate Joint Stock Company - 1

Accounting for revenue, expenses and determining business results at Saigon Real Estate Joint Stock Company - 1 -

Completing the accounting of revenue, expenses and determining business results at Huong Duong Tourism Development and Service Company - 10

Completing the accounting of revenue, expenses and determining business results at Huong Duong Tourism Development and Service Company - 10

Diagram 3.4. Diagram of accounting for financial costs

ACCOUNT LEADERS

December 2012

Account: 635 - Financial expenses

CT number

Accounting date | CT Type | Interpretation | Account | Corresponding account | In debt | Have | |

A | B | C | D | E | F | 1 | 2 |

- Beginning balance | |||||||

Document | |||||||

CTK83 | December 31, 2012 | profession | Interest expense | 635 | 1121 | 28,350,598 | |

other | |||||||

KCT12 | December 31, 2012 | Carry forward profit and loss | Carry forward financial expenses | 635 | 911 | 28,350,598 | |

Add | 28,350,598 | 28,350,598 | |||||

Closing balance | |||||||

(Source: According to data from the accounting department of Nam Gia Lai Trading Company)

3.7. Accounting for other income and other expenses

Accounting for other income and other expenses in the company includes:

+ Other income is unusual income that rarely occurs, mainly from the liquidation of fixed assets such as: gasoline selling tools, transport vehicles... or money earned from renting premises. This income accounts for a small proportion of the Company's total income.

- Normally, when receiving money from renting premises, accountants rely on the short-term rental contract, compare and record it in Misa software. Then, issue 2 payment vouchers, have the chief accountant sign and confirm and give copy 2 to the customer, copy 1 is kept internally.

- If it is a case of liquidation of fixed assets, accounting is based on the fixed asset liquidation contract.

+ Other expenses are expenses not related to the business or financial activities of the Company. They are expenses related to liquidation of fixed assets, fines for breach of contract, etc.

However, in December 2012, at Nam Gia Lai Trading Company, there were no transactions related to other income or other expenses.

3.8. Accounting determines business performance

At the end of the month, the accountant will determine the business performance results on Misa software (Summary / Profit and Loss Transfer Subsystem). Based on the data that the accountant has entered during the month, the software will automatically calculate and give the results of the company's business performance during the month. After that, the accountant will export the results to an excel file and submit it to the Board of Directors for confirmation.

Specifically, these entries are recorded as follows:

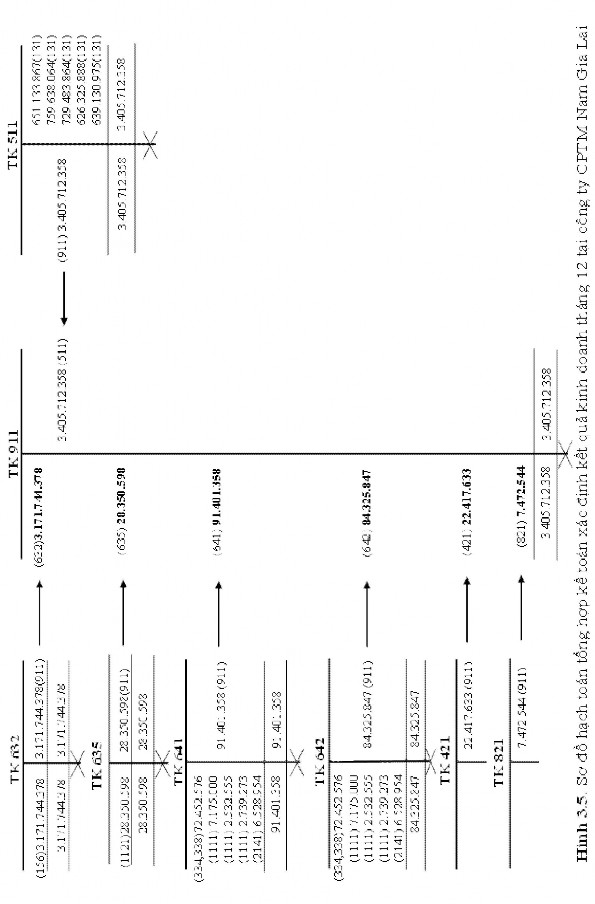

a. Revenue transfer

Debit account 511: 3,405,712,358

Credit account 911: 3,405,712,358

Debit account 911: | 3,375,822,181 |

There is account 632: | 3,171,744,378 |

There is account 635: | 28,350,598 |

There is account 641: | 91,401,358 |

There is account 642: | 84,325,847 |

- Determine the business results of Unilever industry in December 2012 3,405,712,358 - 3,375,822,181 = 29,890,177 VND

- Corporate income tax payable in December 2012 29,890,177 * 25% = 7,472,544 VND

- Profit after corporate income tax of Unilever industry in December 2012

29,890,177 - 7,472,544 = 22,417,633 VND

Thus, in December 2012, Unilever's business activities brought the company a profit of 22,417,633 VND.

a. Debit account 911: | 29,890,177 |

There is account 4211: | 22,417,633 |

There is account 8211: | 7,472,544 |

b. Debit account 8211: 7,472,544

Credit account 3334: 7,472,544

ACCOUNT LEADERS

December 2012

Account: 911 – Determining business results

CT number

Accounting date | CT Type | Interpretation | Account | Corresponding account | In debt | Have | |

A | B | C | D | E | F | 1 | 2 |

- Beginning balance | |||||||

KCT12 | December 31, 2012 | Carry forward profit and loss | Transfer of sales revenue and service provision | 911 | 511 | 3,405,712,358 | |

KCT12 | December 31, 2012 | Carry forward profit and loss | Carry over cost of goods sold | 911 | 632 | 3,171,744,378 | |

KCT12 | December 31, 2012 | Carry forward profit and loss | Carry forward financial expenses | 911 | 635 | 28,350,598 | |

KCT12 | December 31, 2012 | Carry forward profit and loss | Carry forward cost of sales | 911 | 641 | 91,401,358 | |

KCT12 | December 31, 2012 | Carry forward profit and loss | Carry over business management expenses | 911 | 642 | 84,325,847 | |

KCT12 | December 31, 2012 | Carry forward profit and loss | Current corporate income tax expense | 911 | 8211 | 7,472,544 | |

KCT12 | December 31, 2012 | Carry forward profit and loss | Profit after corporate income tax career | 911 | 4211 | 22,417,633 | |

Add | 3,405,712,358 | 3,405,712,358 | |||||

Closing balance | |||||||

(Source: According to data from the accounting department of Nam Gia Lai Trading Company)

General accounting diagram

Chapter4 : COMMENTS AND RECOMMENDATIONS

4.1. Comments

4.1.1. General comments

Our country's economy is gradually changing to match the general development of the regional and world economy. Therefore, the important issue is how businesses should affirm their existence and develop in a market that is increasingly competitive and fierce. And Nam Gia Lai Trading Joint Stock Company is also among them. Although it is a joint stock company developing in the difficult Central Highlands mountainous region, but with the position of providing the main supply of essential goods for the people, it has the task of production and business with the goal of operating effectively as well as bringing high profits. Over 13 years of operation, the company has experienced many difficulties due to market fluctuations, crises... However, the company has always operated sustainably, brought high profits, and always fulfilled its duties to the State budget. The development of Nam Gia Lai Trading Joint Stock Company along with the company's increasingly sustainable position, deserves to be the leading company in the circulation of essential goods in the Southern and Southeast regions of Gia Lai province.

- In terms of accounting, the company applies accounting standards and methods in accordance with the principles and regulations of the State. Compared with the theoretical basis learned, it is found that when applied in practice, specifically the accounting work at Nam Gia Lai Trading Company, there are differences. Therefore, when going out into practice, in addition to having to master professional knowledge, accountants must also have a great understanding of the actual situation.

- In the company, the accountant is not only passive, only facing data and books, but also an advisor to the chief accountant, helping the chief accountant as well as managers grasp the current situation of the unit to make the most correct investment plan and decision.

4.1.2. Advantages

- The company is one of the pioneering enterprises in the South and Southeast of Gia Lai province to apply accounting software in accounting work as well as daily data processing of the unit. With the characteristics of diverse goods and large economic transactions, this is a solution to help reduce the workload for accounting staff, saving time and costs for the company. Specifically, the data entry process is fast, accurate and timely; the verification and inspection process is convenient, easy to detect errors and correct.

- Also with the characteristics of diverse goods, the volume of goods imported into the warehouse, exported from the warehouse is very large and continuous, so the management and control of the Unilever industry is very strict, tight and thorough. Therefore, the goods are always guaranteed quality, creating high trust with customers. From there, ensuring that revenue is always stable and the market is increasingly expanded.

- Expenses incurred during the period are always approved and signed by the chief accountant and the company's board of directors to ensure the reasonableness and accuracy of the data. Avoid fraud and duplicate expenses that cause losses to the company.

- The company's facilities are quite modern. In addition, along with the policies to encourage the spirit of employees of Nam Gia Lai Trading Company, this is a factor that helps accountants and employees work enthusiastically and devote themselves to the overall development of the unit.

4.1.3. Disadvantages

- The consumer market is still limited, focusing only on key and long-standing markets.

- The company mainly sells goods by retail method, mainly through agents. Therefore, it is difficult for the company to control actual sales but only relies on sales reports sent by agents and sales staff.

- The company does not apply provisions for inventory price reduction or provisions for bad debts. If established, these funds will help the company minimize risks.

- The company does not offer trade discounts to customers who purchase in large quantities.

- Unilever's products are too diverse. This is also a problem that causes difficulties for managers and accountants in warehousing, exporting, preserving goods and taking inventory at the end of the period; causing a lot of costs for the company.

- The company's headquarters and warehouse are in two different locations, so the delivery of goods is often slow when there is a request for goods. On the other hand, when handing over the warehouse to the warehouse keeper, you have to trust the warehouse keeper completely, so even with strict management, it is inevitable that goods will be lost.

- The company's general level is still a bit low. This is also a limitation that the company needs to overcome.

4.2. Recommendations

4.2.1. Consumer market

Currently, the company is still focusing on consuming goods in the center of towns, districts as well as in wards in the region. These are key and long-standing markets, bringing a stable number of customers and consumption. However, in the long term, with the goal of sustainable development and continuous expansion, the company should exploit the potential in remote markets such as in villages, communes, hamlets, and hamlets... Therefore, the work of the manager is very important, needing to grasp the situation in the areas to have the right and appropriate development strategy.

4.2.2. Sales method

The manager regularly coordinates with the Sales Supervisor to conduct surprise inspections of authorized agents and sales staff, and sets out reward policies for authorized agents and sales staff who perform their duties well and exceed the set sales target.