This provision plays a very important role in making information transparent for a large part of the free market (unlisted public companies), helping investors have honest information about businesses that are currently outside the scope of the law on securities and securities market. The application of information disclosure forms through electronic means is considered an effective solution to bring information to the maximum number of investors in the most synchronous and timely manner, shortening the delay in the information disclosure process.

The work of monitoring and handling violations of information disclosure has initially been focused on. In the early stages of operating the stock market: information disclosure violations of some listed companies appeared relatively commonly, such as the false disclosure of business results in 2002 of BIBICA Confectionery Joint Stock Company, the value added tax fraud of Canfoco in 2002. The case of fining CAVICO Company Limited when this company became a major shareholder of Cavico Vietnam Mining and Construction Joint Stock Company but did not report on the ownership of major shareholders to the State Securities Commission and Ho Chi Minh City Stock Exchange within the prescribed time with a fine of 20 million VND, fining Ba Ria - Vung Tau Housing Development Joint Stock Company 20 million VND when this company did not fully disclose information according to the legal deadline... Thus, the detection and handling of violations of information disclosure have initially been considered important to deter and ensure transparency in the market.

(6) State management of securities registration, depository, clearing and payment activities

Registration, depository, clearing and settlement of securities transactions are auxiliary services that ensure the settlement of transactions and transfer of securities ownership, contributing to ensuring the legitimate rights and interests of investors. This is also the final step, creating a closed circle for securities transactions on the market.

Maybe you are interested!

-

Basics of Securities and the Stock Market - 51

Basics of Securities and the Stock Market - 51 -

Total Registered Capital and Average Registered Capital of Enterprises

Total Registered Capital and Average Registered Capital of Enterprises -

Establishing Investment Funds to Attract Investors and Launching New Products, Derivative Securities Market Products to Prevent Risks

Establishing Investment Funds to Attract Investors and Launching New Products, Derivative Securities Market Products to Prevent Risks -

Total FDI Capital Registered and Implemented in Vietnam in the Period 1988-2006

Total FDI Capital Registered and Implemented in Vietnam in the Period 1988-2006 -

The Role of Securities Companies in the Development of Vietnam's Stock Market.

The Role of Securities Companies in the Development of Vietnam's Stock Market.

In the early stages of building the stock market, the functions of registration, depository, and clearing of securities transactions were performed independently by the Ho Chi Minh City Stock Exchange and the Hanoi Stock Exchange without any connection with each other. On July 27, 2005, the Ministry of Finance issued Decision No. 189/QD-BTC, establishing the Securities Depository Center and officially coming into operation at the time when the Vietnamese stock market witnessed a remarkable growth in the number of registered securities, securities companies and investors in the market. According to

Decision 3195/QD-BTC dated September 9, 2005 of the Ministry of Finance, the Securities Depository Center is responsible for registering, depositing, clearing and paying for securities; providing services to support securities trading and buying and selling. At the same time, it monitors, within its authority, compliance with regulations and operating procedures of depository members in registration, depository and clearing activities.

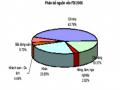

As of December 31, 2009, the total number of members of the VSD was 124, including 102 securities companies, 03 domestic commercial banks, 05 branches of large foreign commercial banks such as HSBC, Citygroup, Deutsche Bank... and 14 members opening direct accounts. Currently, the VSD has managed each investor in detail, including 797,068 domestic investor accounts and 14,195 foreign investor accounts. The total value of securities registered at par value at the VSD increased rapidly from 2006-2009 as follows:

Registered securities

million

20,000

252

5

2,103

788

Fund certificate

15,000

252

Bonds issued in foreign currency Bonds issued in domestic currency UPCOM stocks

10,000

1,948

Share

171

16,191

1,489

5,000

100

839

2,470

8,262

5,209

0

2006

2007

2008

2009

Chart 2.8: Total value of securities registered at par value at the Vietnam Securities Depository from 2006-2009

Source:State Securities Commission

The regulation of all securities registration, depository, clearing and settlement activities at a single TTLKCK has avoided dispersion and increased operational efficiency by taking advantage of the scale of TTLKCK. Along with that, the functional block supporting transaction activities is separated from the transaction function undertaken by the SGDCK and TTGDCK, so each organization has the conditions to specialize more deeply in each field of operation, while the scope and quality of services

also increased thanks to the improvement of organizational and operational aspects and management of each unit.

Regarding the scope of services provided, the operation of the Securities Depository Center will help overcome the limitations of the old system. The issuance of centralized transaction codes for foreign investors has simplified procedures, ensured the consistency of the system and shortened the implementation time. The shortened payment time creates more convenience for investors when participating in the market. In addition, thanks to the good performance of management and supervision functions, the Securities Depository Center has contributed to improving the quality of activities of depository members, ensuring the safe and stable operation of the market.

The State's strict management of the activities of the Securities Depository Center through the granting of depository licenses is completely consistent with international practice because securities depository activities are considered a conditional business activity, related to the management and holding of investors' accounts, helping investors exercise related rights during the depository period.

(7) Management of securities trading and investment activities:

- For securities trading activities:

According to the Law on Securities, securities business is the performance of securities brokerage, securities trading, securities underwriting, securities depository, securities investment fund management, and securities investment portfolio management.

The State regulates the legal capital for each type of business. The current capital level is higher than the previous capital level. Accordingly, for securities brokerage services, it is 25 billion VND, securities self-trading is 100 billion VND, securities guarantee is 165 billion VND, securities investment consulting is 10 billion VND. In case an organization requests a license for many business activities, the legal capital is the total legal capital corresponding to each business activity for which a license is requested. In addition to the requirements on legal capital, the State management agency also regulates the conditions on facilities and personnel (such as employees working in the securities field must have a practice license, regulations on professional ethics, etc.).

The licensing process for the above business organizations is also carried out according to a relatively strict 6-step process: ensuring transparency, fairness and objectivity.

In recent years, the State has provided many favorable financial incentives to encourage the formation and operation of securities trading organizations. Circular 100/2001/TT-BTC on taxes for the securities sector stipulates that the above types of securities trading are not subject to value added tax. Newly established securities companies and fund management companies are exempt from corporate income tax for 2 years from the time of taxable income, reduced by 50% of payable tax for the next 3 years, and are subject to a corporate income tax rate of 20% for 10 years from the date of commencement of operations, after which the general tax rate is 28%. Obviously, the above regulations clearly demonstrate the incentives for securities companies and fund management companies, demonstrating the goal of the State management agency in promoting the development of the securities market.

To manage and supervise the activities of these organizations, the State Securities Commission has issued and guided the implementation of documents such as Decision No. 92/2004/QD-BTC on the system of monitoring indicators for securities companies and securities management companies, Decision No. 401/2005/QD-UBCK dated September 19, 2005 on promulgating regulations on monitoring the registration, depository, clearing and settlement of securities of depository members and the Securities Trading Center and the Securities Depository Center. These are necessary and specific legal bases for the functional departments of the State Securities Commission, the Securities Trading Center and the Securities Depository Center to effectively implement securities market monitoring activities.

In the process of monitoring the activities of these organizations, the State Securities Commission has detected and handled many violations in business activities in the market, thereby contributing to ensuring fairness and transparency for all participants in the market, creating peace of mind for investors.

- Regarding management and supervision of securities investment activities:

Management and supervision of securities investment activities on the Vietnamese stock market include issuing policies to attract domestic and foreign investors to participate in investing in the stock market, carrying out necessary administrative procedures such as opening trading accounts, depositing deposits to place trading orders, etc., and supervising the legal compliance of investors.

investment as reporting obligations of major shareholders to ensure fairness in the stock market. According to current regulations, securities companies and fund management companies are responsible for managing and supervising securities investors who are their customers in accordance with the provisions of law. Securities trading centers and stock exchanges manage securities investors' transactions mainly through supervising customers in carrying out procedures for registering transaction codes (for foreign investors), opening trading accounts, depositing securities, making deposits and placing trading orders at securities companies that are members of the stock exchanges and stock exchanges.

To attract foreign investment, the Vietnamese Government has implemented an open-door policy for foreign investors from the beginning with cautious steps following certain loosening roadmaps. The policy does not discriminate between domestic and foreign investors by allowing foreign investors to directly carry out transaction procedures at securities companies like domestic investors. The process of implementing the policy to attract foreign investors to the Vietnamese stock market is carried out with relatively cautious and flexible steps. Initially, according to Decision 139/1999/QD-TTg on the participation rate of foreign parties in the Vietnamese stock market, foreign organizations and individuals are only allowed to hold a maximum of 20% of the total outstanding shares of a joint stock company and a maximum of 20% of the total number of investment certificates of a securities investment fund, in which each foreign organization is allowed to hold a maximum of 7% and each foreign individual holds a maximum of 3%; The capital contribution of a foreign securities business organization participating in a joint venture securities company is maximum 30% of the charter capital.

After a period of time, the Vietnamese stock market has revealed certain weaknesses. In response to practical requirements, on July 17, 2003, the Prime Minister issued Decision 146/2003/QD-TTg replacing the above Decree, which stipulates that foreign organizations and individuals are allowed to buy and sell securities on the Vietnamese stock market to hold a maximum of 30% of the total number of listed shares of a public company, and the capital contribution ratio of securities trading organizations to securities companies and fund management companies is also adjusted to 49%. This policy has created a real boost for securities trading activities on the Vietnamese stock market. From October 2003 to April 2004, the Vietnamese stock market has clearly recovered thanks to the main impact of foreign investors, the VN-Index has increased from about 130 points to about 250 points, and the total transaction value has also increased from several billion to tens of billions of VND per trading session. The next stage is resistance.

The lack of excitement in the trading of the Vietnamese stock market, according to many experts, is due to the fact that the ownership ratio of foreign investors in most listed companies has been filled. On September 29, 2005, the Prime Minister signed Decision 238/2005/QD-TTg to expand the room for foreign investors. Accordingly, foreign organizations and individuals buying and selling securities on the Vietnamese stock market are allowed to hold a maximum of 49% of the total number of shares and investment certificates listed and registered for trading on the stock market. This regulation does not limit the holding ratio of outstanding bonds of an issuer. To strengthen the management and supervision of foreign investors and ensure safety during the integration process, the Government has used various management tools, such as regulations requiring foreign investors to register transaction codes, comply with the State Bank's regulations on foreign exchange management, foreign investors are only allowed to transact in Vietnamese Dong and comply with the securities ownership ratio according to the above regulations.

Implementing a policy of non-discrimination between domestic and foreign investors has contributed to creating attractiveness for foreign investors. In addition, opening up and attracting foreign investment from the beginning has helped domestic investors learn experience and investment skills in the stock market. Decision 55/2009/QD-TTg, dated April 15, 2009 of the Prime Minister on the participation rate of foreign investors in the Vietnamese stock market stipulates: Foreign investors buying and selling securities on the Vietnamese stock market are allowed to hold a maximum of 49% of the total number of shares of a public joint stock company. In cases where specialized laws have other provisions, the provisions of specialized laws shall apply. In cases where the foreign ownership ratio is classified according to the list of specific industries, the classification list shall apply. Holding a maximum of 49% of the total number of investment fund certificates of a public securities investment fund. Hold up to 49% of the charter capital of a public securities investment company. For bonds: the issuing organization may stipulate a limit on the holding ratio for the outstanding bonds of the issuing organization.

Foreign securities trading organizations are allowed to participate in the establishment of securities companies and fund management companies in Vietnam as follows: Only foreign securities trading organizations are allowed to contribute capital and purchase shares to establish securities companies. The maximum foreign capital contribution ratio is 49% of the charter capital of the securities company. Only foreign securities trading organizations are allowed to

Foreign insurance business organizations and securities investment fund management businesses are allowed to contribute capital and purchase shares to establish fund management companies. The maximum foreign capital contribution ratio is 49% of the charter capital of the fund management company.

Since the beginning of 2006, the development of the stock market has increased the demand for loans for investment and trading in securities, and the risk of credit risks has also increased due to the downward trend in securities prices. In the management activities of the State Bank of Vietnam for this activity, at the end of May 2007, two documents considered to be most directly related to the business activities of credit institutions and affecting securities investment activities on the stock market were issued. These are Directive 03/2007/CT-NHNN, dated May 28, 2007 on controlling the scale and quality of credit and lending for investment and trading in securities to control inflation and economic growth, and Decision No. 1141/QD-NHNN dated May 28, 2007 on adjusting the increase in the required reserve level for credit institutions. Accordingly, the Governor of the State Bank requires credit institutions from July 1, 2007 (the effective date of Directive 03) to control the ratio of outstanding loans and discounting of valuable papers for investment and trading in securities to the total outstanding credit balance of the credit institution at below 3%. For credit institutions with the ratio of outstanding loans and discounting of valuable papers for investment and trading in securities to the total outstanding credit balance of the credit institution at 3% or more, debt collection and debt reduction must be carried out, no later than December 31, 2007, in accordance with the prescribed ratio... In reality, after Directive 03 was issued, it had a negative psychological impact on the operation of the stock market and according to many experts, this was one of the reasons for the decline in the stock market from May to September 2007.

Thus, the State has given certain incentives to securities investors in the Vietnamese stock market in the form of tax incentives to encourage investors to participate in the stock market. According to Circular No. 100/2004/TT-BTC, the State does not impose value added tax on investment activities of securities investment funds, does not impose income tax on income such as dividends, bond interest, difference in buying and selling securities and other income from securities investment of individual investors. This contributes significantly to creating the attractiveness of the stock market and stimulating demand in the market.

The government's open policies on stock investment activities have had a positive impact on investor participation in the Vietnamese stock market.

2.2.2.5. Evaluation of the role of state management in the stock market in recent times

(1) Results achieved

After nearly 10 years of operation, although there have been many ups and downs and there are still many issues that need to be improved, the Vietnamese stock market has had a great impact on the improvement of the market economy and the overall development of the country's economy. To achieve the above achievements, the State has played a very important role, shown in the following main aspects:

Firstly, the work of perfecting the legal framework and market development policies is highly focused.

In order to meet the need to create a safe legal corridor for the operation of the stock market, since the establishment of the market, state management agencies have issued a series of documents, Decrees, Circulars, etc., as well as contributed comments to many legal documents drafted by ministries and branches such as: Criminal Procedure Code, Civil Procedure Code, Enterprise Law, Investment Law, Tax Laws, Law on amending and supplementing a number of articles of the Law on Credit Institutions, Competition Law, Auditing Law, etc. thereby gradually unifying and perfecting legal regulations related to the stock market.

Regarding the completion of the legal framework in the field of securities and securities market. Since the Government issued Decree No. 48/1998/ND-CP, dated July 11, 1998, on securities and securities market, creating the first official legal basis to regulate activities on the securities market, the issuance of legal documents related to securities and securities market has been relatively specific and strict, closely following the implementation situation and being implemented relatively fully. In particular, the issuance of the Securities Law and sub-law documents has created the necessary legal basis to deploy the management and supervision of activities and participants on the securities market. The continuous issuance of legal documents amending and supplementing shortcomings to suit the practical situation of the volatile securities market has gradually better met the requirements of transparency, protection and trust for investors, creating a healthy competitive environment, ensuring the smooth operation of the market.