- BSC helps businesses grow (learn and adapt), encourage improvement

continuous progress

- BSC helps quantify non-financial indicators into objective and transparent measurements, creating motivation in management.

- BSC helps businesses achieve consistency between goals and create a self-regulating system as well as timely corrective measures, helping businesses control effectively.

1.3 Key Performance Indicators (KPI)

KPI - Key Performance Indicator was born to create a link between the BSC model and the reality of applying performance measurement of a business (David Paramenter, 2009).

1.3.1 Concept of KPI

Key performance indicators (also known as Key Performance Indicators - KPIs) are indicators used in management to measure, report and improve work performance (David Paramenter, 2009).

KPIs should be quantifiable. They should be agreed upon by the members of the organization and should reflect the critical success factors of the organization. Regardless of the KPI used, they should reflect the organization’s goals and should be quantifiable (measurable).

1.3.2 Classification of KPIs:

According to David Paramenter (2009), there are three essential types of performance indicators as follows:

- Key Results Indicator (KRI) shows what the business has done with an indicator (KRI – Key Results Indicator)

- Performance Index (PI) tells you what you need to do (PI - Peformance Indecator)

- Key performance indicators (KPIs) tell us what to do to increase performance.

significantly (KPI- Key Performance Indicator).

1.3.2.1 Key result indicators (KRI)

KPIs are the results of many activities and show whether the company is on track or not. Key result indicators provide information on results at a point in time and are usually monitored periodically on a monthly or quarterly basis. These indicators have in common that they are the results of many activities and need a long time to monitor, showing the organization whether it is on track or not. However, these indicators do not show the organization what needs to be done to improve the results achieved. (David Paramenter, 2009)

Some key performance indicators include: Profits from customers; Net profits from key products; Increase in sales; Number of employees participating in the plan …

1.3.2.2 Performance Index (PI)

A key performance indicator is a management tool used to measure, report, and improve performance. A key performance indicator tells you what to do, and is a set of metrics that focus on aspects of an organization's operations. (David Paramenter, 2009)

In the process of combining with the BSC model, performance indicators are also divided into four main aspects: Performance indicators on the financial aspect; performance indicators on the customer aspect; performance indicators on the internal aspect; and Performance indicators on the training and development aspect.

1.3.2.3 Key Performance Indicators - KPI:

According to David Paramenter (2009), performance indicators have the following seven characteristics: they are non-financial indicators; They are regularly evaluated; They are influenced by the board of directors and senior management; They require employees to understand the indicators and take corrective action; They attach responsibility to individuals and groups; They have a significant impact on the aspects of the scorecard; They can have a positive impact.

Key performance indicators should be current and future indicators that generate

Differences attract people's attention and impact most aspects of

BSC.

1.4 Applying KPI and BSC to analyzing production and business activities

Basically, when applying the BSC model, KPI indicators are also established and revolve around the four aspects of the balanced scorecard. Therefore, the author temporarily divides them into four main KPI groups:

1.4.1 Group of indicators measuring financial aspects

KPIs in this perspective will tell us whether the implementation of strategies and goals leads to improvements in key results. The financial perspective typically focuses on:

- Revenue growth

- Reduce costs and improve productivity

- Asset utilization and investment strategy

Figure 1.2: Strategies in financial aspects (R.Kaplan & D.Norton, 2011)

In order to implement financial strategies, some key indicators in the field

These are collected and illustrated in Table 1.1.

Table 1.1: Some key measurement indicators in the financial aspect (R.Kaplan & D.Norton, 2011)

Strategic Theme | |||

Revenue growth and product mix | Reduce costs and improve productivity | Asset utilization and investment strategies | |

- Sales growth rate | - Profit margin % | ||

Sales by segment | - Revenue/Employee | with investment; (RO A, | |

U | song | ROE, ROI, ROCE ...) | |

business - SB | - Percentage of revenue from new customers' products and services | - Scrap rate by revenue | - R&D cost % to sales |

of unit k | - Target customer market share | - Cost reduction ratio | - Payback period (cash cycle) |

strategy c | - Revenue ratio from the new application | - Indirect cost ratio vs. revenue | - Quantity of initial material enter |

C | - Customer and product line profitability | - Unit cost per output product | |

Maybe you are interested!

-

Solutions to improve the business performance of Opera restaurant at Park Hyatt Saigon hotel - 2

Solutions to improve the business performance of Opera restaurant at Park Hyatt Saigon hotel - 2 -

Some solutions to improve business performance at JABIL Vietnam Co., Ltd. by 2017 - 1

Some solutions to improve business performance at JABIL Vietnam Co., Ltd. by 2017 - 1 -

Solutions to Improve Business Efficiency of Vietnam Technological and Commercial Joint Stock Bank

Solutions to Improve Business Efficiency of Vietnam Technological and Commercial Joint Stock Bank -

Evaluate the performance of some distributed hash table algorithms DHT and propose solutions to improve the performance of the CHORD algorithm - 1

Evaluate the performance of some distributed hash table algorithms DHT and propose solutions to improve the performance of the CHORD algorithm - 1 -

Some Online Content Marketing Solutions To Improve Business Efficiency Of Ani International Training Academy

Some Online Content Marketing Solutions To Improve Business Efficiency Of Ani International Training Academy

In general, businesses can implement each strategy individually or in combination, and depending on the characteristics of each company, they can apply just enough of the above measurement indicators.

1.4.2 Customer perspective measurement index

When selecting metrics for the customer perspective of the BSC, organizations need to answer key questions:

- Who are our target customers?

- What is our motto?

- What do customers expect or demand from us?

Customer metrics - metrics that show the relationship between customer satisfaction and business performance: Customer satisfaction, customer loyalty, market share, lost customers, response rate, value delivered to customers, quality, efficiency, service, cost…

Key metrics in the customer perspective: Market share; Customer retention; New customer acquisition; Customer profitability.

Some key metrics: Service failure index; Request completion time; Customer satisfaction survey; Product market share; Winning new customers; Customer retention

1.4.3 Internal process aspect measurement index (R.Kaplan & D.Norton, 2011)

In this perspective, managers focus on identifying and building the most important processes to achieve customer and shareholder goals. Typically, businesses will focus on the following four important processes:

- Process of developing and maintaining supplier relationships

- The process of producing goods and services

- Sales process and after-sales service

- Risk management

Process for developing and maintaining supplier relationships:

Process for developing and maintaining supplier relationships:

Developing relationships with suppliers is very important for the existence and development of a company. Input quality, delivery time, purchasing costs, etc. are the factors that make up the quality, high or low price of the goods provided by the company. Therefore, the goal of today's companies is to develop effective relationships with suppliers to reduce overall costs. In addition to the purchase price of goods, there are other costs that the company must pay to obtain goods such as purchasing costs, import costs, raw material inspection, obsolete goods costs or production stoppage costs due to lack of goods, etc.

Some of the key metrics used in this process include: Transaction Rate

On-time delivery; Defective goods rate; Return rate to suppliers; Ratio of purchasing costs to total purchase price; Number of days of inventory …

The process of producing goods and services

Manufacturing operations begin with production planning when an order is received from a customer and end with delivery to the customer. These operations tend to be repetitive and monitoring and control of these operations typically focuses on financial measures, standard costs, budgets or variances. In conjunction with total quality management, performance measures used today include quality and cost measures:

Quality measures:

With the particularly important role of quality in today's company operations in maintaining and developing business, companies have built a quality measurement system including: Defect rate (DPM); Good product rate; Quality cost (scrap, returned goods, repaired goods...); Product rate that meets quality standards from the beginning.

Cost measures:

In general, cost accounting systems have focused on the costs of each department or individual customer. The main cost measures that businesses can use are: Cost structure by revenue; Unit cost of each output product; Ratio of indirect costs to sales; Cost of defective goods in the production process; Quality costs...

Sales process and after-sales service

Typically, the sales process begins when a company begins to take inventory and process deliveries to customers. Similar to the process of developing and maintaining supplier relationships, the goals of this process also include performance metrics for cost, quality, and lead time.

Key metrics for this process include: Cost of inventory held

products and delivery to customers; On-time delivery rate; Delivery rate

No errors; Number and frequency of customer complaints.

Risk Management Process

Risk Management Process

The company's operations always contain many potential risks in production and business. Risks that may occur include cash flow shortages, interest rate increases, natural disasters, fires, etc. Managing risks in operations as well as in production helps the company develop safely and sustainably, helping the company avoid fluctuations in income and cash flow.

The key metrics for this process are: Inventory deterioration; % of uncollectible debts; Debt to capital ratio; Interest coverage ratio; …

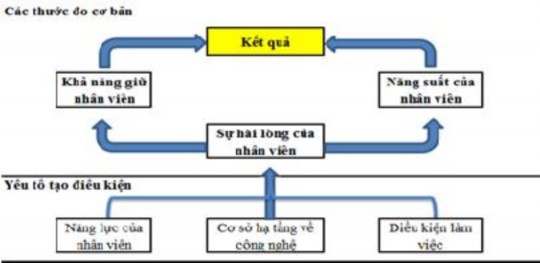

1.4.4 Learning and growth metrics

The learning and growth aspect is of utmost importance for adapting to changes in the present and preparing for the future. According to R. Kaplan & D. Norton, the learning and growth aspect consists of three main components: Employee competencies; Information system competencies; Motivation, accountability, and networking.

Figure 1.3: Learning and growth assessment framework (R.Kaplan & D .N orton, 2011)

Overall, employee satisfaction is the foundation for improving employee productivity and retaining employees towards delivering greater output.

for the company. To improve employee satisfaction, the company should target the following factors:

Enabling factors are employee capabilities, technological infrastructure, and employee working conditions.

Some of the main indicators in evaluating the training and development aspect are: Employee satisfaction index; Employee turnover rate; Revenue per employee; Value added per employee; Staff development; Availability of strategic information…

1.5 Contents of indicators in analyzing production and business activities according to the BSC model:

1.5.1 Financial aspect

KPIs for revenue growth and product mix:

KPIs for revenue growth and product mix:

Return on investment (RO I) indicator (Ngo Quang Huan, 2011):

ROI =

Net profit Weekly assets =

Corporate Profit

Companyℎ Tℎu x Investment capital

RO I is an indicator that shows how much profit has been generated compared to the value

investment resources. The higher the ROI value, the more effective the investment capital is.

Return on total assets (ROA (Ngo Quang Huan, 2011)):

ROA = Net profit after tax (NI)

Total assets (A)

This is an index reflecting the performance and efficiency of assets.

invested

The higher this ratio, the more effectively the company's assets are used and the higher the profit. This indicator is determined on the basis of net profit over total assets. This is an indicator to evaluate the efficiency of asset use, or the efficiency of turning investment into profit.

This is also an indicator to measure the company's performance without