There are still many debates, criticisms, and questions about this scale, especially its generality and validity in measuring quality. The SERVQUAL measurement procedure is quite lengthy, so a variant of SERVQUAL, SERVPERF, has appeared.

The SERVPERF scale is used to measure customer perceptions to determine service quality instead of measuring both perceived and expected quality like the SERVQUAL scale. This scale was proposed by Cronin & Taylor (1992) based on overcoming the difficulties when using the SERVQUAL scale. They believe that service quality is best reflected by perceived quality without expected quality.

Service quality = Perception level

Maybe you are interested!

-

Introduction to Saigon Thuong Tin Commercial Joint Stock Bank (Sacombank)

Introduction to Saigon Thuong Tin Commercial Joint Stock Bank (Sacombank) -

General Introduction About Bim Food Joint Stock Company

General Introduction About Bim Food Joint Stock Company -

Introduction to Vietnam Joint Stock Commercial Bank for Industry and Trade - Thang Long Branch

Introduction to Vietnam Joint Stock Commercial Bank for Industry and Trade - Thang Long Branch -

General Assessment of the Business Performance of Vietnamese Joint Stock Commercial Banks

General Assessment of the Business Performance of Vietnamese Joint Stock Commercial Banks -

Introduction of Vietnam Joint Stock Commercial Bank for Industry and Trade - Phu Yen Branch and Deposit Mobilization Activities

Introduction of Vietnam Joint Stock Commercial Bank for Industry and Trade - Phu Yen Branch and Deposit Mobilization Activities

Due to its origin from the SERVQUAL scale, the components and observed variables of this SERVPERF scale remain the same as SERVQUAL.

1.2.3 Factors affecting CVTD quality

Objective factors

Income and psychology of people: the ability to shop and the purchasing power of consumers are determined by their income. A developed economy creates a stable mentality for people, along with a good income, creating a potential market for banks to exploit and provide CVTD services and vice versa. The source of repayment for consumer loans is the income of customers, so customers' income greatly affects the bank's decision to lend or not.

Competition from other credit institutions : facing fierce competition from other credit institutions in the market, CVTD activities become more difficult. It is both a factor that hinders the process of shaping the scale of CVTD activities and a factor that encourages banks to focus resources on their CVTD products. Currently, competitors in CVTD activities can be divided into 3 main groups. Group 1 includes state-owned commercial banks, group 2 includes foreign banks, joint venture banks and group 3 includes joint stock banks.

Society: unemployment rate, labor structure from training mechanism are the main issues affecting CVTD. Currently, our country has policies and programs to implement reasonable labor structure transformation.

Party and State policies and guidelines: In order to create a driving force to promote the country's economy to overcome difficulties and challenges, continue the industrialization and modernization process and create a favorable environment for production and business activities, financial and monetary activities, Party and State leaders have introduced many new policies and guidelines, suitable to the needs and aspirations of the people, including policies that directly or indirectly affect CVTD.

Subjective factors

Credit policy: specific orientation and credit policy towards satisfying consumer needs are decisive factors for the effectiveness of CVTD activities in particular and other activities in general. Therefore, only with specific planning policies can resources for its development be focused to complete well. Policies suitable to market practices will create competitive advantages for banks.

Customer appraisal: effective appraisal techniques and procedures, without cumbersome or complicated procedures in a short time, are one of the important methods to attract customers. Credit appraisal aims to make correct assessments of customers and loans, thereby making appropriate lending decisions. A reasonable, scientific and unified appraisal technique system is the decisive factor in appraisal quality and therefore determines loan quality, because the most important thing in CVTD is the "credibility" of the customer.

Ability to mobilize capital: directly affects the term, interest rate and CVTD limit. If the capital source is large and abundant, the bank can easily expand the scale and diversify its CVTD products.

Credit officers: the qualifications of bank officers have a great influence on the activities of the bank in general and the activities of credit officers in particular. Especially for the activities of credit officers with high risks, it requires both professional qualifications and professional ethics from credit officers.

Credit officers will conduct analysis and evaluation to select quality loans that bring profits to the bank. The qualifications of credit officers, in addition to being good at professional skills, also include ethical qualities. Officers who come into contact and work in a money environment are easily bribed, and can harm both the bank and the customer for personal gain. In an increasingly fierce competitive environment between banks, customers have many choices of service providers to satisfy their needs. Therefore, in order to gain trust from customers to create effective CVTD operations, banks always pay attention to building the image of a team of credit officers with good professional expertise, professional style, enthusiasm, providing quick services, saving time for customers.

Facilities: affect the psychology of customers depositing and borrowing money; the more modern banking technology is, the more quickly and effectively banks can perform banking operations.

1.2.4 Policy mechanism to support CVTD at commercial banks

In recent times, implementing the government's stimulus policy, the State Bank and ministries have issued many documents to create conditions for commercial banks to expand credit to the economy, creating conditions for economic sectors to increase consumption to stimulate economic growth.

1.2.4.1 Credit mechanism

In the period before the Banking Ordinance (from August 1988 to October 1990), the State Bank issued a credit mechanism according to economic sectors, and began to expand lending to the non-state economy. Before the Law on Credit Institutions was issued (from 1990 to September 1998), the State Bank issued a credit mechanism in the direction of expanding lending, gradually improving the business autonomy of credit institutions.

The regulations have generally demonstrated the motto that the State Bank does not deeply intervene in the business process of credit institutions but creates conditions for credit institutions to be proactive in business, reducing unnecessary procedures for customers to borrow capital conveniently, but at the same time strengthening the State management role of the State Bank. When the Banking Law

The State and the Law on Credit Institutions came into effect, the State Bank issued the Regulations on lending by credit institutions to customers attached to Decision No. 324/1998/QD-NHNN1 replacing previous directives on lending regulations. Basically, the provisions of the Lending Regulation 324 have regulated the lending relationship between credit institutions and customers in the process of borrowing and repaying debts, replacing the previous cumbersome and patchwork lending document system, ensuring more transparency in the lending process, emphasizing the rights and obligations of the parties in credit activities. The lending mechanism is expanded and made more transparent by the Lending Regulation attached to Decision No. 1627/2001/QD-NHNN. Accordingly, credit institutions are allowed to lend to subjects that are not prohibited by the Regulation. Lending Regulation 1627 has created a clear but safe legal corridor for lending activities, facilitating credit institutions to fully exercise their rights, obligations and responsibilities in lending, applying international practices in accordance with the actual conditions and legal environment of Vietnam. Mechanism 1627 continues to be supplemented and amended according to Decisions No. 127/QD/2005/QD-NHNN, No. 87/QD/2005/QD-NHNN to be more suitable with the actual operations of credit institutions, as well as with other management regulations of the State Bank, contributing to proactive credit activities, improving credit quality of credit institutions, and at the same time improving the management capacity of the State Bank in credit work.

1.2.4.2 Loan guarantee mechanism

During the period of the centrally planned economy, the banking sector had the responsibility to fully meet the capital needs of state-owned enterprises and cooperatives in all economic sectors according to the principle of having equivalent materials as collateral. The guarantee of loans by means of pledging or mortgaging the borrower's assets or guaranteeing the borrower's assets by third parties has not been regulated.

Due to practical conditions requiring the State Bank to have new regulations on loan security, on August 17, 1996, the Governor of the State Bank issued the Regulations on mortgages, pledges and guarantees for bank loans of credit institutions, attached to Decision No. 217/QD-NH1 (Regulation 217). According to Regulation 217, all customers of all economic sectors borrowing from credit institutions must implement measures to secure assets. This regulation

Invisibly, the loan security by means of pledging, mortgaging the borrower's assets, and guaranteeing with assets of a third party is considered the most important loan condition. The regulation on loan security by assets formed from loan capital only applies to loans or projects for national and people's welfare decided and taken responsibility by the General Director (Director) of the credit institution.

Pursuant to the provisions of the Law on Credit Institutions, the Civil Code, the Land Law and other relevant legal documents, on December 29, 1999, the Government issued Decree No. 178/1999/ND-CP on loan guarantees of credit institutions (Decree 178). Decree 178 and documents on loan guarantees are a fundamental innovation compared to the past, consistent with relevant legal documents, creating a legal corridor for banking credit activities in recovering debts that credit institutions have lent to customers, in order to limit and prevent risks.

On October 25, 2002, the Government issued Decree No. 85/2002/ND-CP amending and supplementing Decree No. 178/1999/ND-CP dated December 29, 1999 on loan guarantees of credit institutions (Decree 85). This Decree has ensured consistency and compliance with current provisions of relevant laws, in accordance with international practice. Decree 85 has allowed credit institutions to self-regulate and agree with borrowers on loan guarantees. The provisions of Decree 85 are clear, specific, easy to apply, simplifying loan guarantee procedures to comply with relevant provisions of law and the current legal environment.

CHAPTER 2

ASSESSMENT OF CONSUMER LOAN QUALITY AT JOINT STOCK COMMERCIAL BANK FOR FOREIGN TRADE OF VIETNAM, HUE BRANCH

2.1 GENERAL INTRODUCTION OF THE JOINT STOCK COMMERCIAL BANK FOR FOREIGN TRADE OF VIETNAM HUE BRANCH

2.1.1 Introduction to Joint Stock Commercial Bank for Foreign Trade of Vietnam Hue Branch

2.1.1.1 Formation and development process

Before 1993, when there was no Joint Stock Commercial Bank for Foreign Trade of Vietnam - Hue Branch, enterprises in Thua Thien Hue province had to open a foreign currency account and open L/C in Da Nang, Hanoi, ... to carry out business operations. Unfavorable traffic conditions along with long distances had a significant impact on business results due to delays in time and travel expenses. On the other hand, it also affected the psychology of the recipient as well as the depositor through the bank. For that reason, the establishment of Joint Stock Commercial Bank for Foreign Trade of Vietnam - Hue Branch (Vietcombank Hue) was considered an inevitable requirement.

According to the directive of Vietcombank's board of directors and based on the actual needs of Thua Thien Hue province regarding banking operations. According to Decision 68-QDNH dated August 10, 1993 of the General Director of the Joint Stock Commercial Bank for Foreign Trade of Vietnam in Thua Thien Hue was established and officially put into operation on November 2, 1993. Currently, the head office is located at 78 Hung Vuong - Hue City. The bank's Vietnamese transaction name is Joint Stock Commercial Bank for Foreign Trade of Vietnam - Hue Branch.

2.1.1.2 Basic situation of Joint Stock Commercial Bank for Foreign Trade of Vietnam Hue Branch in the period 2009 - 2013

2.1.1.2.1 Labor situation

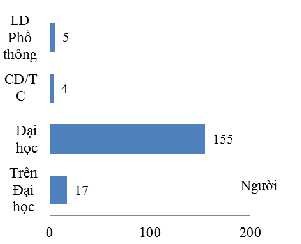

Chart 2.1 Labor situation of VCB Hue in 2013

(Source: Branch General Department)

As of 2013, Hue branch staff had 181 people including 62 men and 119 women.

The branch has constantly innovated the work of building and operating the unit, improving the qualifications of the workforce, reforming working methods, and arranging and assigning staff reasonably to meet the actual situation and requirements of economic innovation.

2.1.1.2.2 Asset and capital situation

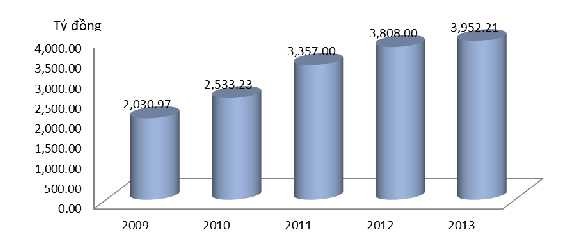

Chart 2.2 Asset and capital situation of VCB-Hue Bank in the period of 2009-2013

(Source: Branch General Department)

The bank's assets and capital tended to increase in the period 2009-2013. It increased from more than 2 trillion VND in 2009 to nearly 4 trillion VND in 2013.

In terms of assets

Cash at the bank has increased steadily over the years, but deposits at the State Bank over the past 5 years have increased and decreased unevenly. On the contrary, credit relations with customers have

The trend has fluctuated steadily over the past 5 years. Banking operations have been smooth and fast thanks to the presence of specialized machinery and equipment, but the proportion of fixed assets of banks is still quite low and has increased dramatically over the years.

In terms of capital

Deposits at the branch tend to fluctuate unevenly over the past 5 years. Capital mobilized from customers is the indicator with the largest value in the branch's capital. This indicator tends to increase steadily over the years. The reason is that in the period of 2009

– In 2013, the branch always tried to offer suitable interest rates along with promotional programs to increase the scale of capital mobilization. The equity ratio tends to increase and decrease unevenly every year.

Always create trust from the people. In addition, the policies to attract capital with attractive interest rates, the effective implementation of deposit promotion programs have attracted an increasing number of people to the branch. This further proves that the position of the branch is increasingly affirmed in the province.

2.1.1.2.3 Business performance results Business performance results are

The issue is of primary concern in the business activities of any organization or individual. It will fully reflect the business situation of the branch. Therefore, during the time of operation under the leadership of the Board of Directors and the enthusiastic efforts of all officers and employees of the Joint Stock Commercial Bank for Foreign Trade of Vietnam, Hue Branch

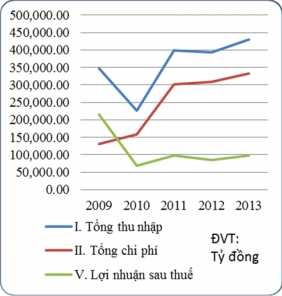

achieved the following results: Chart 2.3 Business performance results

VCB-Hue Bank, period 2009-2013

(Source: Branch General Department)

Profit is the difference between total income and total expenses, the ultimate goal that every bank needs to achieve, this is the indicator to evaluate the economic efficiency of the bank's activities, striving to increase profits is a regular task.

Based on the chart above, we can see the total income of Joint Stock Commercial Bank for Foreign Trade of Vietnam - Hue branch:

The total income of the bank in 2010 tended to decrease compared to 2009, reaching more than 227 trillion VND. By 2011, it was more than 367 trillion VND, an increase of 140 trillion VND, equivalent to 61.67%. In 2012, income from interest returned to its inherent growth rate, reaching nearly 375 trillion VND, and in 2013, non-interest income increased and reached more than 49 trillion VND. In 2012, the total income of the entire bank was more than 393 trillion VND and by 2013, this figure was 430 trillion VND.

Participating in many production and business cycles, to expand the scale of operations, the bank also increases costs over the years but still ensures profits for the bank to operate firmly during difficult economic times.

(For detailed data, see Appendix 1)

2.1.2 CVTD business process at Joint Stock Commercial Bank for Foreign Trade of Vietnam Hue Branch

Step 1: Guide customers to prepare loan application

For first-time credit customers: Credit officers guide customers to provide information about the customer; bank regulations that customers must meet regarding loan conditions and advise on setting up the necessary documents to receive a loan from the bank.

For customers who already have a credit relationship: Credit officers guide customers to complete loan applications.

-Loan application includes:

- Loan application form.

- Documents on legal capacity, civil conduct capacity, civil liability include:

+ Present ID card/passport; residence permit (household registration, KT3); residence permit for foreign individuals.

+ Documents and reports on production, business, services, life and financial capacity of customers.

+ Investment project or business production, service, life plan and other related documents.

+ Documents proving the legality and value of assets securing the loan: Land use rights certificate, property ownership certificate... and other related documents.

Step 2: Credit officer conducts review and appraisal

-Credit Officer:

- Collect information about loan customers.

- Appraisal of loan customers (non-financial); financial appraisal: checking the validity and legality of documents provided by customers; analyzing the feasibility and effectiveness of plans and projects; customers' ability to repay debts; checking and analyzing loan security measures (legality, value and ability to handle loan collateral, etc.)

- Prepare appraisal report, be responsible for the analysis and appraisal results on the report and the proposed opinion on whether to grant or not to grant the loan. Then transfer all documents and report to the credit department leader.

- Notify customers of the decision to lend or not to lend by the Director or authorized person.

-Credit department manager:

Re-evaluate all loan applications, credit officer's submission or appraisal submission transferred by the appraisal department and clearly state your opinion on the appraisal form regarding whether to grant or not to grant the loan to submit to the Director or legally authorized person for consideration and decision and be responsible for the content of the above tasks.

-Director of legal representative:

Review the credit department's appraisal report and proposal, along with the appraisal department's appraisal report, to decide whether to grant or not to grant a loan and be responsible for his/her decision.

Step 3: Complete legal procedures for loan security

After the loan application has been assessed and approved, the customer will sign a loan guarantee contract with a credit officer.

Step 4: Establish a credit contract

After signing the loan guarantee contract, the customer will sign the credit contract.

Step 5: Disbursement

Customers will be disbursed based on the credit limit signed in the contract.

Step 6: Check and monitor loan capital

Credit officers are responsible for checking and monitoring the customer's borrowing process, loan use and debt repayment.

Step 7: Collect debt and interest according to plan

Customers can repay the debt (pay principal and interest periodically, in multiple installments or pay principal and interest at once upon maturity) according to the signed contract.

Step 8: Liquidate credit contract

- Loan settlement: When the customer has paid off the debt, the credit officer will coordinate with the accounting department to check and reconcile the principal, interest and fee payments to settle the loan.

- Liquidation of credit contract: the effective period of the credit contract and loan guarantee contract is as agreed in the signed credit contract and loan guarantee contract. When the borrower has paid off the principal, interest and fees, the credit contract and loan guarantee contract will automatically expire and the parties need to make a contract liquidation record.

Step 9: Release of collateral

Credit officers draft documents requesting release of collateral and loan documents to submit to the Head of Credit Department and Director for approval.

2.2 ASSESSMENT OF CONSUMER LOAN QUALITY AT JOINT STOCK COMMERCIAL BANK FOR FOREIGN TRADE OF VIETNAM, HUE BRANCH IN THE PERIOD 2009-2013

2.2.1 Credit situation at Joint Stock Commercial Bank for Foreign Trade of Vietnam Hue Branch over 5 years 2009-2013

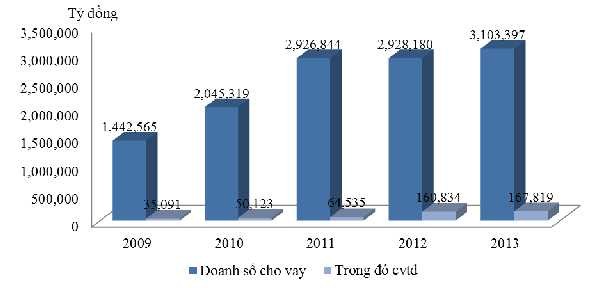

CVTD sales account for a small portion of the bank's total lending.

Chart 2.4: Credit turnover & CVTD of VCB-Hue over 5 years 2009 - 2013

(Source: Branch credit report)

The bank's total lending turnover in 2010 was over 2 trillion VND, an increase of 602 billion VND compared to 2009. The total lending turnover in 2011 and 2012 was nearly 3 trillion VND, an increase of more than 43% compared to 2010. In 2013, it continued to increase by 175 billion VND compared to 2009, a growth rate of 5.98%, reaching 3,103 billion VND.

Meanwhile, CVTD turnover only accounts for a small number, in 2009 it was 35,091 billion VND, accounting for 2.43%, in 2010 and 2011 it was 50,123 billion VND and 64,535 billion VND respectively. By 2012 CVTD had only reached 160 billion VND, and in 2013 CVTD turnover only increased by 4.34% compared to 2012, reaching nearly 168 billion VND. Although the number has increased, it still accounts for a low proportion.

Similarly, debt collection turnover and outstanding debt both account for a low proportion compared to the total debt collection turnover and outstanding debt of the Bank.

Through this, we can see that CVTD is increasing but still accounts for a small proportion in the bank's overall credit activities, which proves that the bank is expanding CVTD activities in a cautious direction. That is what the Bank needs to promote in the next business periods.