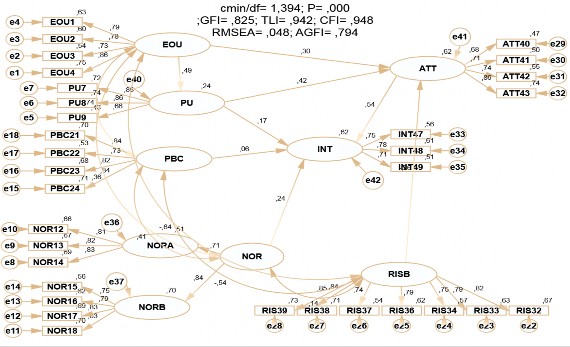

Figure 4.11 SEM structural model results

The detailed results of the structural model tests are shown in Table 4.25 below, in which the standard error coefficients are all smaller than [2.58], and there is no negative variance, indicating that the Heywood phenomenon does not appear, the model is considered appropriate. The Heywood phenomenon appears when one or more variances of the errors or correlations between latent variables have negative values. The estimates if this phenomenon occurs will be theoretically inappropriate and must be corrected.

Table 4.25 SEM structural model results

Relationship

Estimate standardize | SE | CR | P | |||

NT usefulness | <--- | NT is easy to use | 0.487 | 0.059 | 5,313 | *** |

Attitude | <--- | NT is easy to use | 0.295 | 0.059 | 3,005 | 0.003 |

Attitude | <--- | Useful NT | 0.425 | 0.085 | 4,696 | *** |

Attitude | <--- | Perception of risk | -0.259 | 0.053 | -2.99 | 0.003 |

Intent | <--- | NT behavioral control | 0.06 | 0.062 | 0.657 | 0.511 |

Intent | <--- | Attitude | 0.536 | 0.118 | 4,345 | *** |

Intent | <--- | Subjective standard | 0.236 | 0.082 | 2,561 | 0.01 |

Intent | <--- | Useful Perception | 0.174 | 0.091 | 1,729 | 0.084 |

Maybe you are interested!

-

Discussion of Quantitative Research Results on the Impact of Control Variables on Financial Performance

Discussion of Quantitative Research Results on the Impact of Control Variables on Financial Performance -

Building a Scale and Research Model of Factors Affecting Customers' Decision to Choose a Bank to Deposit Savings at

Building a Scale and Research Model of Factors Affecting Customers' Decision to Choose a Bank to Deposit Savings at -

Research Model and Research Methodology to Analyze the Impact of Bad Debt on Bank Efficiency

Research Model and Research Methodology to Analyze the Impact of Bad Debt on Bank Efficiency -

Research Results on the Relationship Between Exchange Rate Level and FDI Capital in Vietnam and Discussion

Research Results on the Relationship Between Exchange Rate Level and FDI Capital in Vietnam and Discussion -

Test Results and Discussion of Research Results

Test Results and Discussion of Research Results

The values of the standardized estimates are shown in Table 4.25 above. Of the eight hypotheses that the research model produced, six were accepted (p<0.05) and two were rejected. The coefficient of determination R2 of Attitude was 62.2% and of Intention was 62%, indicating that the above research model explained 62.2% of the attitude towards granting NNCNC credit and 62% of the intention to implement credit contracts for NNCNC production of credit officers of commercial banks.

4.4.1.7. Estimating theoretical models using Bootstrap

Table 4.26 Bootstrap estimation results

Relationship

Estimate ML | SE | SE-SE | Mean | Bias | SE-Bias | |||

PU | <--- | EOU | 0.312 | 0.059 | 0.002 | 0.315 | 0.003 | 0.003 |

ATT | <--- | EOU | 0.179 | 0.059 | 0.003 | 0.177 | -0.001 | 0.005 |

ATT | <--- | PU | 0.401 | 0.085 | 0.003 | 0.401 | 0 | 0.005 |

ATT | <--- | RISB | -0.159 | 0.053 | 0.003 | -0.159 | 0 | 0.004 |

INT | <--- | PBC | 0.041 | 0.062 | 0.005 | 0.021 | -0.02 | 0.007 |

INT | <--- | ATT | 0.514 | 0.118 | 0.006 | 0.545 | 0.031 | 0.009 |

INT | <--- | NOR | 0.211 | 0.082 | 0.01 | 0.23 | 0.02 | 0.014 |

INT | <--- | PU | 0.158 | 0.091 | 0.003 | 0.148 | -0.01 | 0.005 |

Bootstrap is an alternative repeated sampling method used to assess the reliability of the estimates in the model. From the original sample (N=175), the number of repeated samplings in the study was chosen to be 500 times. In Table 4.26 above, the ML estimate column shows the standardized estimate value, the Mean column shows the average of the Bootstrap estimates, SE is the standard deviation, SE-SE is the standard deviation of the standard deviation, Bias is the bias, SE-Bias is the standard deviation of the bias. The estimation results show that the bias of the average of the Bootstrap estimates and the normal estimates is very small, insignificant and statistically insignificant. Therefore, it can be concluded that the estimates in the model can be reliable.

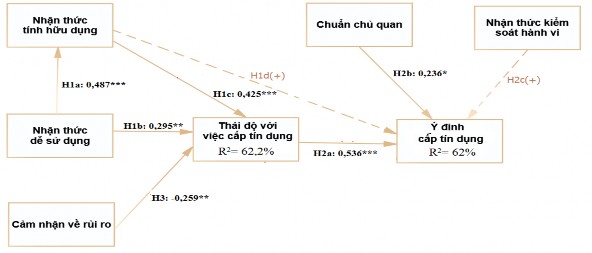

4.4.1.8. Discussion of research results of the first model

The research object of the first model is behavioral intention to grant credit to NNCNC production with the first survey object being credit officers who have never granted credit to NNCNC production. The model includes 7 theoretical concepts and 8 research hypotheses.

The results of testing the research hypotheses of the first model are shown in Figure

4.13 below.

The results of the first model can be expressed through the following regression equations: INT = α1 + 0.536ATT + 0.236NOR + Ð1

ATT = α2 + 0.425PU + 0.295EOU – 0.259RIS + Ɛ2

This is an equation using standardized regression coefficients so α = 0. Ð1 , Ð2 are errors (or noise). Looking up in the estimate table in Sem, we have: Ð1 = 0.119; Ð2 = 0.129.

INT = 0.536ATT + 0.236NOR + 0.119

ATT = 0.425PU + 0.295EOU – 0.259RIS + 0.129

Thus, under the condition that other factors remain constant, when the Attitude towards granting credit of employees increases by one measurement unit, their intention to grant credit will increase by 0.536 units. Similarly, when Subjective Norm increases by one measurement unit, the Intention to grant credit will increase by 0.236 units (note that the measurement unit here is the variance of the scale). In total, the two independent variables Attitude and Subjective Norm explained 62% of the variation in the Intention to grant credit of bank employees, the rest will be influenced by factors other than the research model.

Similarly, with the condition that other factors remain constant, an increase of 1 measurement unit of Perceived Usefulness, Perceived Ease of Use and Perceived Risk will respectively cause the attitude of employees towards granting NNCNC credit to increase by 0.425 or 0.295 or decrease by 0.259 measurement units respectively. In total, the three independent variables Perceived Usefulness, Perceived Ease of Use and Perceived Risk explained 62.2% of the variation in attitude towards granting NNCNC credit of commercial bank credit employees, the rest will be influenced by factors other than the research model.

The equation for the mediating effect of Perceived Ease of Use on Attitude through Perceived Usefulness:

ATT = α3 + 0.295*0.487EUO + Ɛ3 = α3 + 0.144EUO + Ɛ3

In the above mediation effect equation, when other factors remain constant, if Perceived ease of use increases by 1 measurement unit, it will indirectly cause employees' Attitude towards granting NNCNC credit to increase by 0.144 corresponding measurement units.

Figure 4.12 Results of the first research model

The model includes 6 unidirectional scales and one multidirectional scale, which is Subjective Norm with two components, Original Subjective Norm and Policy Subjective Norm . The measurement model results have met the appropriate indicators, the scales in the model have satisfied the reliability, discriminant validity and convergent validity, showing that the study has successfully identified the factors affecting the intention to grant NNCNC credit of credit officers of commercial banks.

The status (magnitude) of the factors in the model is calculated by the average value of the observed variables measuring that factor. With a scale ranging from 1 to 5, the average value of the observed variables also fluctuates within this level, with the average being from 2.6 to 3.4. Values from 3.4 to 4.2 are quite high and from 4.2 and above are high. The average value and standard deviation of the concepts in the model are calculated by the “Mean” function through SPSS software and are shown in Table 4.27 below.

Table 4.27 Status of factors in the first model

Concepts in model 1

Average value | Standard deviation | |

Perceived ease of use | 3.0829 | ,94245 |

Perceived usefulness | 3.5886 | ,89607 |

Original subjective standard | 3,1105 | ,96780 |

Subjective policy standards | 3,6686 | ,90862 |

Subjective standard | 3.3895 | ,81923 |

Perceived behavioral control | 3,1529 | ,89048 |

Perception of risk | 3,4678 | ,90057 |

Attitudes towards funding for NNCNC | 3,6700 | ,73989 |

Intention to provide NNCNC credit capital | 3,9448 | ,68004 |

In the group of four hypotheses H1 on the group effects of factors in the TAM theoretical framework including Perceived Ease of Use and Perceived Usefulness , three hypotheses were supported and one hypothesis was rejected. Accordingly, Perceived Ease of Use has both a direct impact on Attitude towards NNCNC credit granting behavior of credit officers and an indirect impact through Perceived Usefulness . Thus, Perceived Usefulness is the most important factor affecting Attitude , it shows a direct impact with a fairly large intensity (β=0.425). The Perceived Usefulness factor in this model is measured by three observed variables PU7, PU8 and PU9, representing employees' perceptions of the benefits that granting credit to NNCNC can bring to their work, and to the bank they are working for (for example, achieving targets on outstanding loans, credit revenue). Thus, for credit officers who have never proposed credit to NNCNC before, the factor that most affects their Attitude is the perception of the benefits that NNCNC credit contracts bring. The results of the influence branch of the two-factor group in the TAM theory above are similar to the results of the model that Lee (2009) has tested. However, there is a small difference compared to the results of the author above: Perceived Usefulness in this study does not have a direct impact on the Intention to provide NNCNC credit, but only affects the intention indirectly through Attitude . Thus, although the Attitude of the officers is greatly affected by Perceived Usefulness , this factor is not the direct cause leading to their Behavioral Intention . This may be due to the low perceived usefulness of providing credit for NNCNC production among commercial bank credit officers, with an average value of 3.58 for the scale with the largest value range of 5. Therefore, when officers do not have a high perceived usefulness of providing NNCNC credit, this factor only has a positive impact on their attitudes, but is not strong enough to directly affect behavioral intentions.

Similar to the above interpretation, the factor Perceived behavioral control with an average value of 3.15 also shows that employees in subject 1 have no experience working with customers borrowing NNCNC credit, so they are still quite vague about the issue of ability, experience and perception of resources supporting the implementation of NNCNC credit contracts. Therefore, the employees' Perceived behavioral control does not directly affect their Intention to perform that action. In Lee's study (2009), this factor also only has a very small impact on Intention (β=0.12). Factor Perceived control

Behavioral intention in other studies also has a relatively small impact on Intention , for example, in Lee's study (2009) β=0.12 or Jeon et al.'s study (2011) β=0.19. In both studies, the impact of Subjective Norm on Behavioral Intention is always stronger than Perceived Behavioral Control.

The Subjective Norm factor in this model is a second-order concept consisting of two components: Original Subjective Norm (mean=3.11) and Policy Subjective Norm (mean=3.67). The appearance of the new component Policy Subjective Norm is the result of qualitative research, stemming from the unique characteristics of the research environment, which is commercial bank credit. For normal behaviors, an individual's intention to perform them will be influenced by the views of important people around them. In the working environment of the banking industry, and the specific behavior is granting NNCNC credit, employees are also influenced by policies and regulations from the state, locality and the bank where they are working. The appearance of a new factor shows that credit officers of commercial banks are very receptive to and implement the regulations, policies and guidelines set forth by the state, locality and bank. Therefore, the promotion and support of relevant management agencies on a certain development policy can affect the decisions and behaviors of credit officers, in the case of this model, the behavior of granting NNCNC credit. In addition to the psychological impact from colleagues and friends, the impact from local policies and organizational support is also an important cause to promote the behavior of bank credit officers. However, the average value of the above two factors is still quite low, proving that commercial banks have not yet focused on the field of NNCNC credit, and the policies of the state and the support of related parties are still not large.

In addition, another indispensable characteristic factor when researching in the banking credit industry is Risk Perception . Through the qualitative research step, the model has listed 15 observed variables to measure the Risk Perception of credit officers for granting NNCNC credit. During the analysis process, 7 observed variables were retained to measure the risk perception of credit officers. With the first group of credit officers who have never implemented NNCNC credit contracts, their concerns focus on the feasibility of agricultural projects, production management capabilities, quality management and market output; because credit officers have never had experience implementing NNCNC credit contracts, there are concerns about the legality or reliability of the project.

information, records. In summary, when credit officers have never granted NNCNC credit, they are more worried about the feasibility of the project, and this reduces the positive attitude towards accepting NNCNC credit. This negative impact, although not very large (β=0.259), and the average value of Risk Perception at 3.46, shows that officers have a clear and quite careful view in considering and considering the objects needing funding.

Finally, similar to the results of previous studies such as Venkatesh and Bala (2008), Lee (2009) or Jeon et al. (2011) or Ali et al. (2017), Attitude is always the main cause that has the strongest impact on the Intention of credit officers. Thus, with 6/8 research hypotheses supported, the first research model successfully explained the Intention to provide credit for NNCNC production of credit officers at commercial banks. The coefficient of determination R 2 = 62% shows that the level of explanation of the model is above average and the above model can be used to explain and predict the intention to provide credit. In addition, from the results of the model, it is possible to study policies and orientations for the organization and operation of commercial banks to enhance the efficiency of credit activities in the future.

4.4.2. Results of the second model study

4.4.2.1. Results of Cronbach's Alpha reliability analysis

Table 4.28 Cronbach's Alpha test results for scales

Concept (Cronbach's coefficient

Alpha)

Observation variable | Variable-total correlation coefficient | Cronbach's Alpha coefficient if variable is excluded | |

Perceived EOU Ease of Use (0.833) | EOU1 | ,634 | ,800 |

EOU2 | ,711 | ,784 | |

EOU3 | ,687 | ,789 | |

EOU4 | ,769 | ,771 | |

EOU5 | ,476 | ,832 | |

EOU6 | ,387 | ,850 | |

Perceived usefulness PU (0.800) | PU7 | ,560 | ,769 |

PU8 | ,647 | ,740 | |

PU9 | ,607 | ,755 | |

PU10 | ,608 | ,753 | |

PU11 | ,493 | ,787 | |

Subjective norm NOR (0.829) | NOR12 | ,558 | ,809 |

NOR13 | ,582 | ,805 | |

NOR14 | ,555 | ,809 | |

NOR15 | ,589 | ,804 |

NOR16 | ,656 | ,792 | |

NOR17 | ,545 | ,811 | |

NOR18 | ,542 | ,811 | |

Perceived behavioral control PBC (0.798) | PBC19 | ,369 | ,805 |

PBC20 | ,350 | ,818 | |

PBC21 | ,647 | ,744 | |

PBC22 | ,647 | ,743 | |

PBC23 | ,672 | ,739 | |

PBC24 | ,671 | ,739 | |

PBC19 | ,369 | ,805 |

Table 4.28 Cronbach's Alpha test results for scales (cont.)

Concept (Cronbach's coefficient

Alpha)

Observation variable | Variable-total correlation coefficient | Cronbach's Alpha coefficient if variable is excluded | |

Financing Intention INT (0.806) | INT47 | ,638 | ,753 |

INT48 | ,667 | ,730 | |

INT49 | ,671 | ,719 | |

CONF Confirmation (0.795) | CONF44 | ,558 | ,815 |

CONF45 | ,697 | ,655 | |

CONF46 | ,680 | ,691 | |

Attitude towards NNCNC credit funding ATT (0.873) | ATT40 | ,704 | ,783 |

ATT41 | ,717 | ,771 | |

ATT42 | ,552 | ,850 | |

ATT43 | ,726 | ,768 | |

RIS Risk Perception (0.893) | RIS25 | ,321 | ,898 |

RIS26 | ,635 | ,883 | |

RIS27 | ,676 | ,882 | |

RIS28 | ,572 | ,886 | |

RIS29 | ,445 | ,891 | |

RIS30 | ,435 | ,892 | |

RIS31 | ,508 | ,889 | |

RIS32 | ,596 | ,885 | |

RIS33 | ,562 | ,887 | |

RIS34 | ,638 | ,884 | |

RIS35 | ,300 | ,896 | |

RIS36 | ,701 | ,881 | |

RIS37 | ,669 | ,882 | |

RIS38 | ,730 | ,879 | |

RIS39 | ,681 | ,882 |