short terms, showing that bank loans mainly meet liquidity requirements.

In 2010 , with the effectiveness of the two Laws on Credit Institutions and the Law on the State Bank of Vietnam and in accordance with the roadmap of WTO commitments, the State Bank of Vietnam issued Circular 07/2010/TT-NHNN dated February 26, 2010 allowing credit institutions to lend at agreed interest rates. This decision is considered to have opened up capital sources in the market, helping to reflect the relationship between supply and demand of capital in the market more accurately.

However, effective on October 1, 2010 of Circular 13/2010/TT-NHNN, starting from September 2010, the mobilization interest rate in the market continuously created waves. The goal of the State Bank is to reduce the interest rate level to about 10.5% -11%/year. In fact, commercial banks have to mobilize at higher interest rates to prepare sources to meet the capital needs of enterprises at the end of the year. Particularly at some times, interest rates were pushed up to 17% -18%/year, specifically, Techcombank mobilized 17%/year in 3 days of December 8-9-10, 2010. The process of increasing interest rates in many forms has increased the capital mobilization cost of commercial banks, leading to a rapid increase in lending interest rates, some commercial banks have lent at interest rates from 23% - 27%/year. Overnight lending rates in the interbank market have sometimes reached 30% per year. At the same time, the race to increase interest rates and fees in various forms has pushed price competition among commercial banks to become increasingly fierce. In the context of high inflation, the State Bank of Vietnam has implemented a tight monetary policy, restricting lending to real estate and securities trading. Lending interest rates in the market have fluctuated strongly.

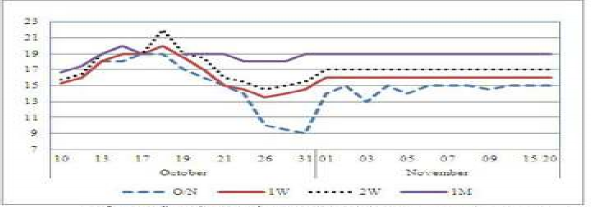

In November 2011, the common overnight VND interest rate was 13-15%; 1 week 15%-17%; 2 weeks 16%-18%; 1 month 18%-19%, which has decreased significantly compared to October 2011. Much higher than the mobilization from the population (14%), many people are concerned that the high interbank interest rate is a sign of the lack of liquidity of the banking system, especially small banks, which can easily lead to collapse. Economic experts say that the increase in interbank interest rate is not too worrying. Because interbank interest rate only reflects in the short-term cycle, if the increase occurs regularly and continuously by month, it is worth discussing, currently it is mainly happening by week. The high increase in interbank interest rate is also partly due to the adjustment of the State Bank to increase the refinancing interest rate from 14% per year to 15%, the overnight lending interest rate in electronic payment

The interbank interest rate from 14% to 16% per year, applied from October 2010, is also a factor pushing up interbank interest rates.

Since Circular 30/2011/TT-NHNN was issued, stipulating the maximum interest rate for non-term deposits and deposits with terms of less than 1 month at 6%/year, the mobilization interest rate has generally been within the framework of 14%/year. In the past, although the ceiling interest rate still has some issues that have not met the requirements, it has basically brought about positive effects, restoring order in the monetary market. Large commercial banks continue to assert their strength; small banks have more difficulty in mobilizing capital, which may lead to liquidity stress. Recently, BIDV's commitment to support liquidity of VND8,000 billion for BacAbank and GPBank is a sign of this.

Chart 2.3 - Interbank VND interest rate developments

Some small commercial banks, due to lending too much to non-production sectors, are at risk of insolvency. To ensure the safety of the system, the State Bank has provided these banks with re-lending loans and encouraged large commercial banks to continue to "pump" capital to support liquidity through the market to banks. To support capital for enterprises directly engaged in production and business, and to open up capital sources to serve the economy, the State Bank has adjusted Circular 13/2010/TT-NHNN by Circular 19/2010/TT-NHNN in the direction of loosening regulations on limits on credit sources for credit institutions. At the same time, to restore market discipline, the State Bank has regulated the ceiling interest rate for mobilization by Circular 02/2011/TT-NHNN and Directive 02/2011/CT-NHNN, Circular 30/2011/TT-NHNN. With a series of administrative measures, strict handling of violations has restored stability to the market.

Table 2.4 - Developments in capital mobilization, investment, deposits, and lending on the interbank market up to September 2012

Unit: Billion VND

CREDIT INSTITUTION

Capital mobilization and lending investment in the interbank market | ||||||||

Fundraising/Deposit Acceptance | Deposit/Lending Investment | |||||||

2010 | 2011 | September 2012 | % Increase, Decrease(-) 2011 vs 2010 | 2010 | 2011 | September 2012 | % Increase, Decrease(-) 2011 vs 2010 | |

VIETINBANK | 74,939 | 74,419 | 61,978 | -520 | 50,508 | 66,170 | 40,923 | 15,662 |

BIDV | 52,279 | 53,127 | 77,529 | 848 | 59,595 | 58,868 | 46,613 | -727 |

VCB | 69,766 | 70,246 | 82,031 | 480 | 78,124 | 78,124 | 103,473 | -467 |

AGRIBANK | 69,918 | 58,147 | 27,849 | -11.771 | 41,178 | 41,303 | 18,073 | 125 |

Block of TCTD N/water | 341,778 | 255,939 | 260,257 | -85.839 | 244,283 | 244,465 | 212,061 | 182 |

SACOMBANK | 20,372 | 25,145 | 7.304 | 4,773 | 16,452 | 19,752 | 13,268 | 3,300 |

ACB BANK | 37,626 | 43,567 | 25,699 | 5,941 | 34,160 | 44,739 | 35,205 | 10,579 |

TECHCOMBANK | 35,874 | 38,754 | 39,992 | 2,880 | 25,564 | 32,506 | 28,911 | 6,942 |

Joint Stock Commercial Bank Block | 458,768 | 332,851 | 425,849 | -125.917 | 361,245 | 458,781 | 392,258 | 97,536 |

Whole system | 1,079,441 | 795,669 | 686.106 | -283.772 | 857,000 | 1,015,970 | 604,319 | 158,970 |

Maybe you are interested!

-

Increasing capital mobilization from individual customers of commercial banks - Case study of Vietnam Joint Stock Commercial Bank for Investment and Development, Phu Tho Branch - 1

Increasing capital mobilization from individual customers of commercial banks - Case study of Vietnam Joint Stock Commercial Bank for Investment and Development, Phu Tho Branch - 1 -

Market Share of Capital Mobilization of Vietnamese Commercial Banks

Market Share of Capital Mobilization of Vietnamese Commercial Banks -

Solutions to enhance capital mobilization at Dong Trieu Branch of Investment and Development Bank - Quang Ninh - 4

Solutions to enhance capital mobilization at Dong Trieu Branch of Investment and Development Bank - Quang Ninh - 4 -

Management of capital mobilization at Vietnam Joint Stock Commercial Bank for Investment and Development - Son Tay Branch - 1

Management of capital mobilization at Vietnam Joint Stock Commercial Bank for Investment and Development - Son Tay Branch - 1 -

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Solutions for tourism development in Tien Lang - 10

zt2i3t4l5ee

zt2a3gstourism, tourism development

zt2a3ge

zc2o3n4t5e6n7ts

- District People's Committees and authorities of communes with tourist attractions should support, promote, and provide necessary information to people, helping them improve their knowledge about tourism. Raise tourism awareness for local people.

*

* *

Due to limited knowledge and research time, the thesis inevitably has shortcomings. Therefore, I look forward to receiving guidance from teachers, experts as well as your comments to make the thesis more complete.

Chapter III Conclusion

Through the issues presented in Chapter II, we can come to some conclusions:

Based on the strengths of available tourism resources, the types of tourism in Tien Lang that need to be promoted in the coming time are sightseeing and resort tourism, discovery tourism, weekend tourism. To improve the quality and diversify tourism products, Tien Lang district needs to combine with local cultural tourism resources, at the same time combine with surrounding areas, build rich tourism products. The strengths of Tien Lang tourism are eco-tourism and cultural tourism, so developing Tien Lang tourism must always go hand in hand with restoring and preserving types of cultural tourism resources. Some necessary measures to support and improve the efficiency of exploiting tourism resources in Tien Lang are: strengthening the construction of technical facilities and labor force serving tourism, actively promoting and advertising tourism, and expanding forms of capital mobilization for tourism development.

CONCLUDE

I Conclusion

1. Based on the results achieved within the framework of the thesis's needs, some basic conclusions can be drawn as follows:

Tien Lang is a locality with great potential for tourism development. The relatively abundant cultural tourism resources and ecological tourism resources have great appeal to tourists. Based on this potential, Tien Lang can build a unique tourism industry that is competitive enough with other localities within Hai Phong city and neighboring areas.

In recent years, the exploitation of the advantages of resources to develop tourism and build tourist routes in Tien Lang has not been commensurate with the available potential. In terms of quantity, many resource objects have not been brought into the purpose of tourism development. In terms of time, the regular service time has not been extended to attract more visitors. Infrastructure and technical facilities are still weak. The labor force is still thin and weak in terms of expertise. Tourism programs and routes have not been organized properly, the exploitation content is still monotonous, so it has not attracted many visitors. Although resources have not been mobilized much for tourism development, they are facing the risk of destruction and degradation.

2. Based on the results of investigation, analysis, synthesis, evaluation and selective absorption of research results of related topics, the thesis has proposed a number of necessary solutions to improve the efficiency of exploiting tourism resources in Tien Lang such as: promoting the restoration and conservation of tourism resources, focusing on investment and key exploitation of ecotourism resources, strengthening the construction of infrastructure and tourism workforce. Expanding forms of capital mobilization. In addition, the thesis has built a number of tourist routes of Hai Phong in which Tien Lang tourism resources play an important role.

Exploiting Tien Lang tourism resources for tourism development is currently facing many difficulties. The above measures, if applied synchronously, will likely bring new prospects for the local tourism industry, contributing to making Tien Lang tourism an important economic sector in the district's economic structure.

REFERENCES

1. Nhuan Ha, Trinh Minh Hien, Tran Phuong, Hai Phong - Historical and cultural relics, Hai Phong Publishing House, 1993

2. Hai Phong City History Council, Hai Phong Gazetteer, Hai Phong Publishing House, 1990.

3. Hai Phong City History Council, History of Tien Lang District Party Committee, Hai Phong Publishing House, 1990.

4. Hai Phong City History Council, University of Social Sciences and Humanities, VNU, Hai Phong Place Names Encyclopedia, Hai Phong Publishing House. 2001.

5. Law on Cultural Heritage and documents guiding its implementation, National Political Publishing House, Hanoi, 2003.

6. Tran Duc Thanh, Lecture on Tourism Geography, Faculty of Tourism, University of Social Sciences and Humanities, VNU, 2006

7. Hai Phong Center for Social Sciences and Humanities, Some typical cultural heritages of Hai Phong, Hai Phong Publishing House, 2001

8. Nguyen Ngoc Thao (editor-in-chief, Tourism Geography, Hai Phong Publishing House, two volumes (2001-2002)

9. Nguyen Minh Tue and group of authors, Hai Phong Tourism Geography, Ho Chi Minh City Publishing House, 1997.

10. Nguyen Thanh Son, Hai Phong Tourism Territory Organization, Associate Doctoral Thesis in Geological Geography, Hanoi, 1996.

11. Decision No. 2033/QD – UB on detailed planning of Tien Lang town, Hai Phong city until 2020.

12. Department of Culture, Information, Hai Phong Museum, Hai Phong relics

- National ranked scenic spot, Hai Phong Publishing House, 2005. 13. Tien Lang District People's Committee, Economic Development Planning -

Culture - Society of Tien Lang district to 2010.

14.Website www.HaiPhong.gov.vn

APPENDIX 1

List of national ranked monuments

STT

Name of the monument

Number, year of decisiondetermine

Location

1

Gam Temple

938 VH/QĐ04/08/1992

Cam Khe Village- Toan Thang commune

2

Doc Hau Temple

9381 VH/QĐ04/08/1992

Doc Hau Village –Toan Thang commune

3

Cuu Doi Communal House

3207 VH/QĐDecember 30, 1991

Zone II of townTien Lang

4

Ha Dai Temple

938 VH/QĐ04/08/1992

Ha Dai Village –Tien Thanh commune

APPENDIX II

STT

Name of the monument

Number, year of decision

Location

1

Phu Ke Pagoda Temple

178/QD-UBJanuary 28, 2005

Zone 1 - townTien Lang

2

Trung Lang Temple

178/QD-UBJanuary 28, 2005

Zone 4 – townTien Lang

3

Bao Khanh Pagoda

1900/QD-UBAugust 24, 2006

Nam Tu Village -Kien Thiet commune

4

Bach Da Pagoda

1792/QD-UB11/11/2002

Hung Thang Commune

5

Ngoc Dong Temple

177/QD-UBNovember 27, 2005

Tien Thanh Commune

6

Tomb of Minister TSNhu Van Lan

2848/QD-UBSeptember 19, 2003

Nam Tu Village -Kien Thiet commune

7

Canh Son Stone Temple

2160/QD-UBSeptember 19, 2003

Van Doi Commune –Doan Lap

8

Meiji Temple

2259/QD-UBSeptember 19, 2002

Toan Thang Commune

9

Tien Doi Noi Temple

477/QD-UBSeptember 19, 2005

Doan Lap Commune

10

Tu Doi Temple

177/QD-UBJanuary 28, 2005

Doan Lap Commune

11

Duyen Lao Temple

177/QD-UBJanuary 28, 2005

Tien Minh Commune

12

Dinh Xuan Uc Pagoda

177/QD-UBJanuary 28, 2005

Bac Hung Commune

13

Chu Khe Pagoda

177/QD-UBJanuary 28, 2005

Hung Thang Commune

14

Dong Dinh

2848/QD-UBNovember 21, 2002

Vinh Quang Commune

15

President's Memorial HouseTon Duc Thang

177/QD-UBJanuary 28, 2005

NT Quy Cao

Ha Dai Temple

Ben Vua Temple

Tien Lang hot spring

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 16pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 6pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 12pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Source: Report on lending and deposit activities of credit institutions of the State Bank. In particular, in the first months of 2012 , interest rates in the interbank market (Market 2) continuously decreased to a low level while interest rates mobilized from enterprises and individuals (Market 1) remained at a fairly high level. This phenomenon has not occurred in the same period in many years. The main transactions (April 2012) only fluctuated within the range of 5.5 - 6.5%/year; one week from -7.5%/year; two weeks from 7.5 - 8%/year and one month from 10.5 - 11%/year. There is a paradox in the market, which is that interest rates for loans to enterprises are still very high (18%/year - 22%/year) while interbank interest rates are very low. In fact, before that, interbank interest rates were also quite low. Specifically, in the week from April 2 to April 6, before the State Bank lowered the ceiling on deposit interest rates to 12% per year, the interbank interest rate announced by the State Bank was lower than other interest rates in the money market and continued to decrease. The average overnight VND interest rate was 10.34% per year; 1 week was 8.9% per year; 2 weeks was 9.17% per year and 1 month was 11.98% per year. These interest rates decreased by 0.1 - 1.5% compared to the week.

before

In the last months of the year, the interbank market interest rate continued to decrease. Some commercial banks had surplus available capital in VND. In fact, the current interest rate in the interbank market does not reflect the true nature of the market, because large banks currently have excess liquidity but only invest in state treasury bills, lend to each other or even do not lend.

interbank lending. Small banks are almost unable to "squeeze" into this market, and if they do, they are required to have collateral when transacting. However, not all small banks have collateral to borrow from interbank, there are two factors that make the interest rate in the interbank market low. (i) - First, this market is currently "concentrated" in banks in the G14 group ( 14 largest commercial banks ) and foreign banks. The cause of this phenomenon is mainly due to historical factors: since the fourth quarter of 2011, the number of small banks with poor liquidity and difficulties in debt repayment has appeared. Obviously, a part of the members have not been able to re-enter the market, which also makes the market not operate perfectly. (ii) - Second and also the most important reason is that commercial banks are limited in credit growth due to the decrease in the number of customers meeting the loan conditions. Therefore, when the amount of money mobilized from the population still increases slightly, banks in the G14 group will have a relatively surplus of deposits. High supply means lower prices, that is the rule. Members of the banking system still fully participate in the interbank market but at different levels. Low interest rates show good liquidity in the market, while lending does not grow as planned. Therefore, banks are having to rebalance their operating plans, adjusting both inputs and outputs. But anyway, interest rates in the interbank market, even if they are low, will only be low in the short term and will certainly have to self-adjust to the correct rule of being higher than interest rates mobilized from the population. Low interbank interest rates show that the capital supply of the State Bank through large banks will shape interest rates in the market, this is the regulation of the State Bank and also a manifestation of excess money in the system.

It is easy to imagine the general goal that the State Bank aims for when implementing 7 groups of solutions in restructuring the banking system: to quickly reduce weak banks and build a small number of banks with enough strength to compete with the region as well as to be the pillars of the entire domestic banking system. These groups of restructuring solutions will be implemented by the State Bank in the period from now to 2015 with many different specific stages. Among the above solutions, the orientation to quickly reduce weak banks that have been in decline for a long time has received special attention from the public. Especially after the recent merger of three joint stock commercial banks Ficombank, TinNghiaBank and SCB. The restructuring process of these banks can be carried out according to the motto of using organizations with strong capacity.

larger scale and greater financial position to participate in the restructuring of smaller credit institutions.

Normally, at the end of the year, the interbank market will be active. However, currently, capital flow in the interbank market shows signs of congestion when many large commercial banks have capital but do not dare to pump it into this market. That is because credit institutions only decide to lend no more than 50% of collateral. Currently, there is no shortage of capital in the interbank market, but when lending, large commercial banks require small commercial banks to have highly liquid collateral such as gold, foreign currency ( not accepting collateral in bonds even if they are bonds issued by the lending bank itself ) and when mortgaging, banks only lend no more than 50% of collateral. The lending limit on collateral is even lower than in the short-term lending market. It can be seen that the mortgage requirement comes from the fact that some commercial banks have deferred debts in the interbank market. In fact, there are currently large commercial banks lending in the interbank market 7,000-

10,000 billion VND, half of which is mortgaged and half is unsecured, but has not yet been recovered. Therefore, the caution of large commercial banks is necessary. However, the strictness in lending by large commercial banks has made it even more difficult for small commercial banks. In this situation, many opinions say that the State Bank needs to take the lead in requiring large banks to support small banks and small commercial banks must commit to the State Bank to comply with the agreement. Only then can the interbank market be cleared. In addition, the State Bank also needs to continue to inject capital through the open market. In response to concerns that the State Bank's injection of money could cause inflation, a banking expert said that increasing the total means of payment depends on the money multiplier. Once the State Bank has controlled credit growth, even if the base currency increases, the money creation coefficient is controlled, the total means of payment will not increase, and will not affect inflation.

Putting borrowing and lending activities in the interbank market into order will help the credit flow of banks to be used more effectively. Tightly controlling the source of borrowing capital on the interbank market will also avoid the situation where commercial banks "live on each other's backs", ending the situation where some large state-owned banks are given preferential loans from the State Bank with low interest rates, and lend to other commercial banks at high interest rates. The State Bank issued Circular 21/2012/TT-NHNN dated June 18, 2012 regulating lending, borrowing; term buying and selling of valuable papers between credit institutions and bank branches.

foreign countries and Circular 01/2013/TT-NHNN dated January 7, 2013 on amending and supplementing a number of provisions in Circular 21/2012/TT-NHNN dated June 18, 2013.

However, there are also opinions that currently many small commercial banks are still hesitant to access capital directly from the State Bank for fear of "exposing" their shady business practices. Therefore, it is hoped that from 2012, when the State Bank has determined and announced the health of commercial banks, the State Bank will have an appropriate management mechanism to put the banking system into operation and business in a transparent, clear and safe manner.

Although there have been no major disputes related to interbank lending and deposit transactions, in 2011, the market saw cases of credit institutions borrowing and receiving deposits from other credit institutions but failing to repay the money on time. In addition, there were also cases of some small commercial banks using capital mobilized through the interbank money market mainly for the purpose of expanding credit, lending for real estate, and trading securities beyond the permitted limit. This has the potential to pose liquidity risks when there are market fluctuations. Currently, the State Bank of Vietnam is researching to restructure the banking system in the direction of arranging and improving the management and operation capacity of commercial banks to ensure system safety. It is possible to merge some weakly operating commercial banks, ensuring that the interbank domestic currency market becomes transparent and develops stably.

(2) Interbank foreign exchange market (foreign exchange)

The interbank foreign exchange market conducts spot transactions, forward transactions, and swap transactions, but the level and scope of each type of transaction is different, mostly spot transactions and very few forward transactions and swap transactions. All are subject to the transaction process: the State Bank announces the exchange rate and regulates the limit of the allowed increase, market members must offer both the buying and selling exchange rates along with the amount of foreign currency bought and sold. After a period of implementation, the transaction turnover in the market has increased: in 2003 it was only 254 million USD, but now it has reached billions of USD.

40000

35000

30000

25000

Transaction turnover

20000

15000

10000

5000

0

2005 2006 2007 2008 2009 2010 2011 2012

Chart 2.4- Average monthly foreign exchange transaction turnover from 2005 to 2012

Source: Annual foreign exchange transaction report of the State Bank of Vietnam. Characteristics of market operations: spot transactions account for a large proportion of the day.

larger, futures trading accounts for only a quarter of total trading. Swaps have

used mainly to solve the need for additional capital in VND for some commercial banks, the proportion of swap transactions is only 8% of the total transactions, mainly exchanging USD for VND for state-owned commercial banks. Official transactions on the interbank market only account for about 15%, while transactions mainly carried out at commercial banks account for 85%.

Exchange rate mechanism : Exchange rate is one of the important macroeconomic policies of each country. The exchange rate between USD and VND in the Vietnamese market is satisfied on the basis of foreign currency supply and demand within the scope of the State Bank's regulations with a limit of a trading band, not exceeding a certain percentage (%).

Since 2007 - the period after joining the WTO - the exchange rate has fluctuated quite complicatedly, the exchange rate between USD and Euro, between USD/JPY as well as the exchange rate between USD/VND. During this period, it was shown that the exchange rate was always a topical and very sensitive issue. The exchange rate not only affects import and export, trade balance, national debt, attracting direct and indirect investment, but also significantly affects people's confidence.

In 2008 , the USD/VND exchange rate increased dramatically. This was a special year for the exchange rate management mechanism as well as for the extremely complicated fluctuations in reality. Compared to the end of 2007, the USD/VND buying and selling rates of commercial banks increased by about 9%, a sudden increase compared to the familiar change of around 1% in previous years. 2008 was also the year that the exchange rate band was widened 3 times in a row, and 2 times the average interbank exchange rate was increased sharply directly. The special nature of the exchange rate in 2008 was also reflected in the opposite fluctuations. At the beginning of the year, a rare development in the history of the Vietnamese currency market was that the exchange rates of commercial banks were lower than the average interbank exchange rate, due to the abundant supply of foreign currency.

2009 is considered a year of many fluctuations in the financial market. It can be said that Vietnam has overcome the bottom of the economic recession, but the financial market is still unstable due to narrow elasticity and high risk level. Although the basic interest rate has been kept at 7% for quite a long time to stimulate demand, this has not reduced the fluctuations in the financial market. Interest rates and exchange rates have continuously fluctuated with many unusual signs.

At times, the exchange rate on the free market has a large difference compared to the official market, causing the dollarization of the economy to increase, creating conditions for hoarding, speculation, market manipulation, and negatively affecting the foreign exchange market. Therefore, the State Bank had to cooperate with a number of Ministries/Agencies, the People's Committees of Hanoi and Ho Chi Minh City to strengthen control over foreign currency and gold trading activities on the free market. In addition, the State Bank also had to adjust the exchange rate for the second time by raising the average interbank exchange rate from 17,034 to 17,961 VND/USD, along with narrowing the margin from +/-5% to +/-3% on November 25, 2009. The goal of this adjustment is to stabilize the USD price on the market, making the exchange rate announced by the State Bank more closely reflect market signals. The adjustment of the exchange rate has had a significant impact on the production and business of enterprises. While export enterprises benefit from the increase in exchange rate, most other enterprises, especially import enterprises, along with organizations and individuals... are under pressure mainly from the increase in the value of USD.

Faced with a serious imbalance in supply and demand due to a large amount of foreign currency being absorbed into the gold trading floor, as well as enterprises having foreign currency earned from business activities hoarding in their accounts, not selling to banks. Therefore, the Government had to use administrative measures to require 06 State-owned corporations and groups to sell foreign currency to banks to increase supply to the market, commercial banks