Figure 2.3 has clarified the internal control system with three clear lines of defense associated with the functions of the internal control system according to Circular 13/2018/TT-NHNN.

2.2.1.2 Internal regulations of Vietnam Bank for Agriculture and Rural Development

Decision 600/QD-HDTV/2012 on promulgating the Charter on organization and operation of Agribank, which stipulates on internal control and internal audit. Accordingly: Internal control system is a set of mechanisms, policies, procedures, internal regulations, and organizational structure of Agribank built in accordance with the guidance of the State Bank and organized to ensure prevention, detection and timely handling of risks and to achieve the set requirements. Agribank needs to establish an internal control system to ensure the following requirements: (1) Ensuring efficiency and safety in operations; protecting, managing, and safely and effectively using assets and resources. (2) Ensuring the financial information system and management information are honest, reasonable, complete and timely. (3) Ensuring compliance with the law and internal regulations, procedures and rules. The activities of the internal control system must be periodically assessed by the internal audit department and an independent auditing organization in accordance with the provisions of law. This Decision also stipulates that the Board of Directors establishes a specialized internal audit unit under the Supervisory Board to conduct internal audit at Agribank with specific tasks of reviewing and independently and objectively assessing the internal control system; independently assessing the appropriateness and compliance with internal regulations, policies, procedures and processes established in Agribank; making recommendations to improve the effectiveness of the system, processes and regulations, contributing to ensuring that Agribank operates safely, effectively and in accordance with the law. This Decision also stipulates that the results of internal audit must be promptly reported to the Board of Directors, the Supervisory Board and sent to the General Director of Agribank. Thus, the Charter of organization and operation of Agribank has stipulated the establishment of an internal control system with control objectives and an internal audit department that is quite consistent with the practices and regulations in Circular 13/2018/TT-NHNN.

Accordingly, the Board of Directors issued Decision 102/QD-HDTV-KTNB/2014 on Agribank's Internal Audit Regulations and the Supervisory Board issued Decision 206/QD-BKS/2019 on the Regulations on the organization and operation of Agribank's Internal Audit. These are considered legal bases that create favorable conditions for establishing Internal Audit as well as Internal Audit activities at Agribank.

Maybe you are interested!

-

Current Status of Internal Control at Viet Duc Friendship Hospital

Current Status of Internal Control at Viet Duc Friendship Hospital -

Current Status of Internal Control System at Vdb

Current Status of Internal Control System at Vdb -

Current Status of Internal Control in Vietnamese Garment Enterprises

Current Status of Internal Control in Vietnamese Garment Enterprises -

Current Status of Internal Control for Corporate Income Tax Compliance of Small and Medium Enterprises at Bu Gia Map District Tax Department

Current Status of Internal Control for Corporate Income Tax Compliance of Small and Medium Enterprises at Bu Gia Map District Tax Department -

Car body electrical practice - 8

zt2i3t4l5ee

zt2a3gs

zt2a3ge

zc2o3n4t5e6n7ts

If the voltage is out of specification, replace the wire or connector.

If the voltage is within specification, install the front fog light relay and follow step 5.

Step 5 Check the front fog light switch

- Remove the D4 connector of the fog light switch

- Use a multimeter to measure the resistance of the front fog light switch.

Measurement location

Condition

Standard

D4-3 (BFG) -D4-4 (LFG)

Light switchFront Fog OFF

>10kΩ

D4-3 (BFG) -D4-4 (LFG)

Front fog light switchON

<1 Ω

- Standard resistor

D4 connector is located on the combination switch assembly.

If the resistance is out of specification, replace the combination switch (the fog light switch is located in the combination switch).

If the resistance is within specification, follow step 6.

Step 6 Check wiring and connectors (front fog light relay-light selector switch)

- Disconnect connector D4 of the combination switch assembly

- Use a voltmeter to measure the voltage value of jack D4 on the wire side.

Measurement location

Control modecontrol

Standard

D4-3 (BFG) - (-) AQ

TAIL

11 to 14 V

D4 connector for the wiring of the combination switch assembly

If the voltage does not meet the standard, replace the wire or connector.

If the voltage is within standard, there may have been an error in the previous measurements.

Step 7 Check the front fog lights

- Remove the front fog light electrical connector.

- Supply battery voltage to the fog lamp terminals

Jack 8, B9 of front fog lamp on the electrical side

blind first.

Power supply location

Terms and Conditions

Battery positive terminal - Terminal 2Battery negative terminal - Terminal 1

Fog lightsbefore morning

- If the light does not come on, replace the bulb.

If the light is on, re-plug the jack and continue to step 8.

Step 8 Check wiring and connectors (relay and front fog lights)

- Disconnect the B8 and B9 connectors of the front fog lights.

- Use a voltmeter to measure voltage at the following locations:

Measurement location

Switch location

Terms and Conditions

B8-2 - (-) AQ

Electric lock ON TAIL size switchFog switch ON

11 to 14 V

B9-2 - (-) AQ

Electric lock ONTAIL size switch Fog switch ON

11 to 14 V

B8 and B9 connectors on the front fog lamp wiring side

Voltage is not up to standard, repair or replace the jack. If up to standard, there may have been an error in the measurement process.

2.2.4. Procedure for removing, installing and adjusting fog lights 1. Procedure for removing

- Remove the front inner ear pads

Use a screwdriver to remove the 3 screws and remove the front part of the front inner ear liner

-Remove the fog light assembly

+ Disconnect the connector.

+ Use a screwdriver to remove 3 screws to remove the fog light cover

2. Installation sequence

-Rotate the fog lamp bulb in the direction indicated by the arrow as shown in the figure and remove the fog lamp from the fog lamp assembly.

-Rotate the fog light bulb in the direction indicated by the arrow as shown in the figure and install the light into the fog light assembly.

- Use a screwdriver to install the fog light cover

-Install the electrical connector

Attention: Be careful not to damage the plastic thread on the lamp assembly.

- Install the front inner ear pads

Use a screwdriver to install the front inner bumper with 3 screws.

3. Prepare the vehicle to adjust the fog light convergence. Prepare the vehicle:

- Make sure there is no damage or deformation to the vehicle body around the fog lights.

- Add fuel to the fuel tank

- Add oil to standard level.

- Add engine coolant to standard level.

- Inflate the tire to standard pressure.

- Place spare tire, tools and jack in original design position

- Do not leave any load in the luggage compartment.

- Let a person weighing about 75 kg sit in the driver's seat.

4. Prepare to check the fog light convergence

a/ Prepare the vehicle status as follows:

- Place the car in a dark enough place to see the lines. The lines are the dividing line, below which the light from the fog lights can be seen but above which it cannot.

- Place the car perpendicular to the wall.

- Keep a distance of 7.62 m between the center of the fog lamp and the wall.

- Park the car on level ground.

- Press the car down a few times to stabilize the suspension.

Note: A distance of approximately 7.62 m is required between the vehicle (fog lamp center) and the wall to adjust the convergence correctly. If the distance of 7.62 m cannot be achieved, set the correct distance of 3 m to check and adjust the fog lamp convergence. (Since the target area varies with the distance, please follow the instructions as shown in the figure.)

b/ Prepare a piece of thick white paper about 2 m high and 4 m wide to use as a screen.

c/ Draw a vertical line through the center of the screen (line V).

d/ Set the screen as shown in the picture. Note:

- Keep the screen perpendicular to the ground.

- Align the V line on the screen with the center of the vehicle.

e/Draw the reference lines (H, V LH and V RH lines) on the screen as shown in the figure.HINT:

Mark the center of the fog lamp on the screen. If the center mark cannot be seen on the fog lamp, use the center of the fog lamp or the manufacturer's name mark on the fog lamp as the center mark.

H line (fog light height):

Draw a line across the screen so that it passes through the center mark. Line H should be at the same height as the center mark of the fog light bulb.

Line V LH, V RH (center mark position of left fog lamp LH and right fog lamp RH):

Draw two lines so that they intersect line H at the center marks.

5. Check the fog light convergence

a/ Cover the fog lamp or remove the connector of the other side fog lamp to prevent light from the unchecked fog lamp from affecting the fog lamp convergence test.

b/ Start the engine.

c/ Turn on the fog lights and make sure that the dividing line is outside the standard area as shown in the drawing.

6. Adjust the fog light convergence

Use a screwdriver to adjust the fog light to the standard area by turning the toe adjustment screw.

Note: If the screw is adjusted too far, loosen it and then tighten it again, so that the last rotation of the light adjustment screw is clockwise.

3. Self-study questions

1. Describe the operating principle of the lighting system with automatic headlight function

2. Describe the operating principle of the lighting system with the function of rotating headlights when turning

3. Draw diagram and connect lighting system on Hyundai Porter car

4. Draw diagram and connect lighting system on Honda Accord 1992

5. Draw the lighting circuit on a 1993 Toyota Lexus

LESSON 3 MAINTENANCE AND REPAIR OF SIGNAL SYSTEM

I. IMPLEMENTATION GOAL

After completing this lesson, students will be able to:

- Distinguish between types of signals on cars

- Correctly describe common symptoms and suspected areas causing damage.

- Connecting signal circuits ensures technical requirements

- Disassemble, install, check, maintain and repair the signal system to ensure technical requirements.

- Ensure safety in work and industrial hygiene

II. LESSON CONTENT

1. General description

The signal system equipped on cars aims to create signals to notify other vehicles participating in traffic about the vehicle's operating status such as: stopping, parking, braking, reversing, turning...

Signals are used either by light such as headlamps, brake lights, turn signals….. or by sound such as horns, reverse music….

Just like the lighting system. A signal system circuit usually consists of: battery, fuse, wire, relay, electrical load and control switch. Only some switches of the signal system are on the combination switch. The switches of other signals are usually located in different locations such as in the gearbox or brake pedal……

2. Maintenance and repair

2.1. Turn signals and hazard lights

The installation location of the turn signal is shown in Figure 3.1. The turn signal control switch is located in the combination switch under the steering wheel. Turning this switch to the right or left will make the turn signal turn right or left.

The hazard light switch is used when the vehicle has a problem while participating in traffic. When the hazard light switch is turned on, all the turn signals on the vehicle will light up at a certain frequency. The hazard light switch is usually placed separately from the turn signal switch (some old cars integrate the hazard and turn signal switches on the same combination switch cluster).

Figure 3.1 Turn signal switch Figure 3.2 Hazard switch

The part that generates the flashing frequency for the lights is called a turn signal relay. The turn signal relay usually has 3 terminals: B (positive power supply); E (negative power supply); L (providing the turn signal switch to distribute to the

lamp)

2.1.1. Circuit diagram

To generate the frequency for the turn signal, a turn signal relay is used in the turn signal circuit. The current from the turn signal relay will be sent to the turn signal switch assembly to distribute the current to the turn signal lights for the driver's purpose.

Figure 3.3. Schematic diagram of a turn signal circuit without a hazard switch

1. Battery; 2. Electric lock; 3. Turn signal relay; 4. Turn signal switch; 5. Turn signal lamp; 6. Turn signal lamp; 7. Hazard switch

Figure 3.4 Schematic diagram of turn signal circuit with hazard switch

1. Battery; 2. Combination switch cluster; 3. Turn signal;

4. Turn signal light; 5. Turn signal relay

Today's cars no longer use three-pin turn signal relays (B, L, E) but use eight-pin turn signal relays (figure 3.5) (pin number 8 is used for hazard lights).

For this type, the current supplying the turn signal lights is supplied directly from the turn signal relay to the lights.

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; vertical-align: 1pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -9pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s9 { color: #008000; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s10 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; te

Car body electrical practice - 8

zt2i3t4l5ee

zt2a3gs

zt2a3ge

zc2o3n4t5e6n7ts

If the voltage is out of specification, replace the wire or connector.

If the voltage is within specification, install the front fog light relay and follow step 5.

Step 5 Check the front fog light switch

- Remove the D4 connector of the fog light switch

- Use a multimeter to measure the resistance of the front fog light switch.

Measurement location

Condition

Standard

D4-3 (BFG) -D4-4 (LFG)

Light switchFront Fog OFF

>10kΩ

D4-3 (BFG) -D4-4 (LFG)

Front fog light switchON

<1 Ω

- Standard resistor

D4 connector is located on the combination switch assembly.

If the resistance is out of specification, replace the combination switch (the fog light switch is located in the combination switch).

If the resistance is within specification, follow step 6.

Step 6 Check wiring and connectors (front fog light relay-light selector switch)

- Disconnect connector D4 of the combination switch assembly

- Use a voltmeter to measure the voltage value of jack D4 on the wire side.

Measurement location

Control modecontrol

Standard

D4-3 (BFG) - (-) AQ

TAIL

11 to 14 V

D4 connector for the wiring of the combination switch assembly

If the voltage does not meet the standard, replace the wire or connector.

If the voltage is within standard, there may have been an error in the previous measurements.

Step 7 Check the front fog lights

- Remove the front fog light electrical connector.

- Supply battery voltage to the fog lamp terminals

Jack 8, B9 of front fog lamp on the electrical side

blind first.

Power supply location

Terms and Conditions

Battery positive terminal - Terminal 2Battery negative terminal - Terminal 1

Fog lightsbefore morning

- If the light does not come on, replace the bulb.

If the light is on, re-plug the jack and continue to step 8.

Step 8 Check wiring and connectors (relay and front fog lights)

- Disconnect the B8 and B9 connectors of the front fog lights.

- Use a voltmeter to measure voltage at the following locations:

Measurement location

Switch location

Terms and Conditions

B8-2 - (-) AQ

Electric lock ON TAIL size switchFog switch ON

11 to 14 V

B9-2 - (-) AQ

Electric lock ONTAIL size switch Fog switch ON

11 to 14 V

B8 and B9 connectors on the front fog lamp wiring side

Voltage is not up to standard, repair or replace the jack. If up to standard, there may have been an error in the measurement process.

2.2.4. Procedure for removing, installing and adjusting fog lights 1. Procedure for removing

- Remove the front inner ear pads

Use a screwdriver to remove the 3 screws and remove the front part of the front inner ear liner

-Remove the fog light assembly

+ Disconnect the connector.

+ Use a screwdriver to remove 3 screws to remove the fog light cover

2. Installation sequence

-Rotate the fog lamp bulb in the direction indicated by the arrow as shown in the figure and remove the fog lamp from the fog lamp assembly.

-Rotate the fog light bulb in the direction indicated by the arrow as shown in the figure and install the light into the fog light assembly.

- Use a screwdriver to install the fog light cover

-Install the electrical connector

Attention: Be careful not to damage the plastic thread on the lamp assembly.

- Install the front inner ear pads

Use a screwdriver to install the front inner bumper with 3 screws.

3. Prepare the vehicle to adjust the fog light convergence. Prepare the vehicle:

- Make sure there is no damage or deformation to the vehicle body around the fog lights.

- Add fuel to the fuel tank

- Add oil to standard level.

- Add engine coolant to standard level.

- Inflate the tire to standard pressure.

- Place spare tire, tools and jack in original design position

- Do not leave any load in the luggage compartment.

- Let a person weighing about 75 kg sit in the driver's seat.

4. Prepare to check the fog light convergence

a/ Prepare the vehicle status as follows:

- Place the car in a dark enough place to see the lines. The lines are the dividing line, below which the light from the fog lights can be seen but above which it cannot.

- Place the car perpendicular to the wall.

- Keep a distance of 7.62 m between the center of the fog lamp and the wall.

- Park the car on level ground.

- Press the car down a few times to stabilize the suspension.

Note: A distance of approximately 7.62 m is required between the vehicle (fog lamp center) and the wall to adjust the convergence correctly. If the distance of 7.62 m cannot be achieved, set the correct distance of 3 m to check and adjust the fog lamp convergence. (Since the target area varies with the distance, please follow the instructions as shown in the figure.)

b/ Prepare a piece of thick white paper about 2 m high and 4 m wide to use as a screen.

c/ Draw a vertical line through the center of the screen (line V).

d/ Set the screen as shown in the picture. Note:

- Keep the screen perpendicular to the ground.

- Align the V line on the screen with the center of the vehicle.

e/Draw the reference lines (H, V LH and V RH lines) on the screen as shown in the figure.HINT:

Mark the center of the fog lamp on the screen. If the center mark cannot be seen on the fog lamp, use the center of the fog lamp or the manufacturer's name mark on the fog lamp as the center mark.

H line (fog light height):

Draw a line across the screen so that it passes through the center mark. Line H should be at the same height as the center mark of the fog light bulb.

Line V LH, V RH (center mark position of left fog lamp LH and right fog lamp RH):

Draw two lines so that they intersect line H at the center marks.

5. Check the fog light convergence

a/ Cover the fog lamp or remove the connector of the other side fog lamp to prevent light from the unchecked fog lamp from affecting the fog lamp convergence test.

b/ Start the engine.

c/ Turn on the fog lights and make sure that the dividing line is outside the standard area as shown in the drawing.

6. Adjust the fog light convergence

Use a screwdriver to adjust the fog light to the standard area by turning the toe adjustment screw.

Note: If the screw is adjusted too far, loosen it and then tighten it again, so that the last rotation of the light adjustment screw is clockwise.

3. Self-study questions

1. Describe the operating principle of the lighting system with automatic headlight function

2. Describe the operating principle of the lighting system with the function of rotating headlights when turning

3. Draw diagram and connect lighting system on Hyundai Porter car

4. Draw diagram and connect lighting system on Honda Accord 1992

5. Draw the lighting circuit on a 1993 Toyota Lexus

LESSON 3 MAINTENANCE AND REPAIR OF SIGNAL SYSTEM

I. IMPLEMENTATION GOAL

After completing this lesson, students will be able to:

- Distinguish between types of signals on cars

- Correctly describe common symptoms and suspected areas causing damage.

- Connecting signal circuits ensures technical requirements

- Disassemble, install, check, maintain and repair the signal system to ensure technical requirements.

- Ensure safety in work and industrial hygiene

II. LESSON CONTENT

1. General description

The signal system equipped on cars aims to create signals to notify other vehicles participating in traffic about the vehicle's operating status such as: stopping, parking, braking, reversing, turning...

Signals are used either by light such as headlamps, brake lights, turn signals….. or by sound such as horns, reverse music….

Just like the lighting system. A signal system circuit usually consists of: battery, fuse, wire, relay, electrical load and control switch. Only some switches of the signal system are on the combination switch. The switches of other signals are usually located in different locations such as in the gearbox or brake pedal……

2. Maintenance and repair

2.1. Turn signals and hazard lights

The installation location of the turn signal is shown in Figure 3.1. The turn signal control switch is located in the combination switch under the steering wheel. Turning this switch to the right or left will make the turn signal turn right or left.

The hazard light switch is used when the vehicle has a problem while participating in traffic. When the hazard light switch is turned on, all the turn signals on the vehicle will light up at a certain frequency. The hazard light switch is usually placed separately from the turn signal switch (some old cars integrate the hazard and turn signal switches on the same combination switch cluster).

Figure 3.1 Turn signal switch Figure 3.2 Hazard switch

The part that generates the flashing frequency for the lights is called a turn signal relay. The turn signal relay usually has 3 terminals: B (positive power supply); E (negative power supply); L (providing the turn signal switch to distribute to the

lamp)

2.1.1. Circuit diagram

To generate the frequency for the turn signal, a turn signal relay is used in the turn signal circuit. The current from the turn signal relay will be sent to the turn signal switch assembly to distribute the current to the turn signal lights for the driver's purpose.

Figure 3.3. Schematic diagram of a turn signal circuit without a hazard switch

1. Battery; 2. Electric lock; 3. Turn signal relay; 4. Turn signal switch; 5. Turn signal lamp; 6. Turn signal lamp; 7. Hazard switch

Figure 3.4 Schematic diagram of turn signal circuit with hazard switch

1. Battery; 2. Combination switch cluster; 3. Turn signal;

4. Turn signal light; 5. Turn signal relay

Today's cars no longer use three-pin turn signal relays (B, L, E) but use eight-pin turn signal relays (figure 3.5) (pin number 8 is used for hazard lights).

For this type, the current supplying the turn signal lights is supplied directly from the turn signal relay to the lights.

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s3 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; vertical-align: 1pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -9pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s9 { color: #008000; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s10 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; te

2.2.2 Current status of completing the internal control system at Vietnam Bank for Agriculture and Rural Development according to COSO international standards

Through Agribank's reports as well as discussions with experts, the thesis synthesizes the current status of Agribank's internal control system according to the five components that make up the internal control system to see the level of completion of this system at Agribank according to the COSO internal control model, including: Control environment - Risk assessment - Control activities - Information & communication - Monitoring. Specifically:

2.2.2.1 Current status of control environment at Vietnam Bank for Agriculture and Rural Development

The thesis analyzes the current status of the control environment at Agribank according to the elements of the control environment (integrity and ethical values, commitment to capacity, Board of Directors & Supervisory Board, organizational structure, division of authority and responsibility, human resource policy) associated with five principles according to the COSO internal control model, specifically:

a. Commitment to honesty and adherence to ethical values

According to Circular 13/2018/TT-NHNN, Control culture is the corporate cultural value of a commercial bank that demonstrates a unified awareness of the importance of control and risk management activities of the Board of Directors, Board of Members, Supervisory Board, General Director (Director) and individuals and departments. Control culture is formed through professional ethics standards, internal regulations, reward and discipline regimes to encourage and ensure that individuals and departments proactively identify and control risks in their operations and the operations of the commercial bank. A strong enough control culture is believed to help commercial banks minimize or avoid losses due to failures of internal control.

Agribank has issued the Agribank Cultural Handbook, which specifically stipulates the Agribank cultural identity, ethical standards, behavior, communication, ethics, and responsibilities of Agribank officers and employees; regulations on standards, conduct, and transaction styles of tellers in the Agribank system; labor regulations... in written form and widely disseminated in the system via the Website, Eoffice internal network... to encourage and ensure that individuals and departments grasp the control messages, thereby proactively identifying and controlling risks in their own operations in particular and Agribank's operations in general. In 2019, Agribank continued to complete the draft Regulations on Professional Ethics Standards.

for employees (except internal auditors and BSK members) to submit to the Board of Directors for approval to create a healthy control culture in the system. However, Agribank's control culture has not been uniformly recognized; some officers have not yet realized the importance of control culture and risk management, leading to serious violations in the process of performing operations due to non-compliance with regulations, business processes and lax inspection and supervision at the unit. The Board of Directors and General Director of Agribank have also taken preventive measures and promptly handled violations and violations of the law and internal regulations of Agribank according to Decision 600/QD-HDTV-TCTL/2015 on promulgating the Charter of organization and operation of Agribank. Specifically, in 2019, Agribank was determined in handling violations of the law, internal regulations and professional ethics standards: Handling units and individuals related to existing problems and violations through internal inspection and examination work, internal fraud cases at units (Cho Lon Branch, Khanh Hoa); Disciplining the heads of branches with low credit quality, many problems, serious violations but slow to overcome (Nam Ha Noi Branch, Branch 10). Thus, Agribank has basically complied with the first principle of COSO standards when establishing a control culture with standards of conduct in the bank and assessing compliance as well as handling violations quite promptly.

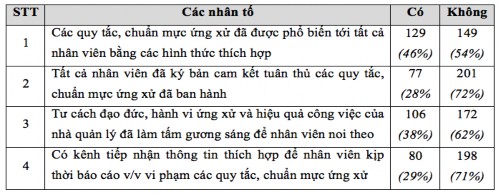

In addition to the achieved results, the survey also found that the Board of Directors and the Executive Board of Agribank have not yet established a strong enough control culture.

Table 2.2 Survey results of some factors belonging to Control Environment

of Agribank

Source: Compiled from survey results at Agribank

Firstly, some managers have not been good role models in complying with ethical standards through words and actions. Secondly, control messages are still communicated to employees in traditional forms such as sending documents and not implementing commitments to ensure compliance. Agribank has not done a good job of promoting and raising employees' awareness of internal control so that they understand and clearly define the functions, tasks, powers and responsibilities in internal control. As a result, employees do not have a control culture and are not really proactive in effectively participating in the implementation of control policies and procedures. Thirdly, the capture and handling of violations of rules and standards has been done but sometimes delayed at Agribank, leading to the consequences of incidents being often large and difficult to overcome. The main reason identified through the above survey results is that Agribank has not established appropriate information channels for employees to promptly report violations. All of the above may lead to a decline in the control culture at Agribank, creating a message throughout the system that internal control only plays a secondary role after other goals of the bank; individuals and departments only focus on performing their own work and forget about control responsibilities.

b. Supervision of the Board of Members and the Board of Supervisors

The supervisory organization structure of the Board of Directors and General Director of Agribank has complied with the regulations of the State Bank (Circular 40/TT-NHNN/2011 on regulations on licensing and organization and operation of commercial banks and Circular 13/TT-NHNN/2018), accordingly: The Board of Directors has established four Committees, including: Risk Management Committee (Decision No. 853/QD-HDTV-TCCB/2009); Personnel Committee (Decision 125/QD-HDTV-TCTL/2014); Policy Committee (Decision 34/QD-HDTV-TCTL/2015); Investment Committee (Decision 781/QD-HDTV-UBNS/2017). Not only improving the organizational structure, in 2019, the Board of Directors issued the Regulations on organization and operation of the Committees to replace the previously issued Regulations on organization and operation to supplement the advisory tasks for the Board of Directors to carry out supervision of senior management according to assigned fields and sectors. The CEO also established three Councils (Risk Council, ALCO Council,

(capital management board) and promulgate the Regulations on organization and operation of the Councils to perform the task of advising the General Director to supervise individuals and departments involved in risk management and asset/liability management. Particularly for the internal control system, the Board of Directors of Agribank has established the function of supervising the internal control system through the internal audit department under the Supervisory Board, which has ensured the second principle of the COSO standard on establishing the responsibility to supervise the development and operation of internal control independently. In addition, the Chairman of the Board of Directors and members of Agribank are all people with appropriate expertise and are mostly aware of risk management. Currently, the Board of Directors and the Supervisory Board of Agribank are also quite independent from the Board of Management (Decision 600/QD-HDTV/2012 and Decision 116/QD-HDTV regulating the Regulations on the operation of the Board of Members of Agribank); has closely directed, fully supported and comprehensively assisted the activities of the Board of Directors. This has created the basis for establishing and operating an effective internal control system as well as a healthy control environment at Agribank.

However, the management and operation at Agribank still show limitations, so it does not ensure complete independence between the Board of Directors and the Board of Management. The General Director decides on issues under the authority of the Board of Directors or the Board of Directors also performs the management work of the General Director . In addition, the decentralization and authorization between management and operation are not specific and clear at Agribank; reflected in the fact that the Board of Directors still has to handle administrative tasks, reducing the role of supervision, strategic planning, and building mechanisms and regulations, which are the main functions of the Board of Directors. If this situation continues, Agribank will not fully meet the principles of COSO standards on ensuring the independence of the Board of Directors from the Board of Management as well as the new regulations in Circular 13/2018/TT-NHNN in separating the two functions of "management" and "operation" to promote a healthy corporate governance, minimizing conflicts of interest. To do so, Agribank needs to enhance the supervisory role of the Board of Directors, completely independent from the operations of the Executive Board.

c. Organizational model and division of authority and responsibility.

Agribank has also basically met the third principle of COSO standards on establishing the bank's organizational structure associated with reporting channels. Time

The organizational structure at the Head Office (TSC) and branches of Agribank has been gradually rearranged to better suit the business model and conditions of this bank. Accordingly, Agribank has continued to consolidate the management model, both centralized and decentralized, restructured and developed the network in accordance with its management capacity. The organizational model has gradually been completed in the direction of independence between the advisory and decision-making departments in business activities and the department that monitors and supervises processes and policies. By December 31, 2019, the organizational structure at the Head Office (TSC) was completed, including: Board of Directors (Chairman and 11 members), Board of Management (General Director, 09 Deputy General Directors, 01 Chief Accountant), Board of Supervisors (Head of the Board and 03 members); 04 Committees have the task of directly advising and assisting the Board of Directors (Policy Committee, Personnel Committee, Risk Management Committee, Investment Committee; ALCO Committee under the Board of Directors has been abolished); 27 Departments/Centers and equivalent units; 03 public service units; 03 regional representative offices; established Councils under the General Director since January 2019, including the Risk Management Council, the Agribank Asset/Liability Management Council (ALCO Council - converted from the ALCO Committee under the Board of Directors), and the Capital Management Council. At the same time, to meet the requirements of governance and management in accordance with the scale of operations, Agribank's senior personnel apparatus has continued to be supplemented and improved over the past time.

Agribank also regularly reviews and evaluates the performance of branches and transaction offices; merges ineffective branches and transaction offices with low development potential; develops networks in agricultural and rural areas - where there are favorable conditions for business expansion. Specifically, Agribank has adjusted the scope of management of Type I branches under TSC in the direction of reducing the scale, in accordance with the requirements of the Restructuring Plan associated with bad debt settlement for the period 2016-2020 (Issued under Decision 01/QD-NHNN/2018 of the State Bank). Accordingly, in 2019, Agribank completed the procedures for adjusting the scope of management of 09 branches in the provinces. In addition, Agribank reorganized the Type I and Type II Branches in Hanoi and Ho Chi Minh City in the direction that TSC does not manage the Type I and Type 3 Branches, ending the Type II Branch model in Ho Chi Minh City.

The basis for dissolving branches and establishing transaction offices after reorganization, typically the merger of Nam Hoa Branch and District 5 Branch into Branch 5, An Suong Branch and Hung Vuong Branch in Ho Chi Minh City into Bac Ho Chi Minh City Branch (in the transitional period before terminating type II branches and establishing transaction offices). This adjustment will help to improve the system, thereby creating more favorable conditions for control activities as well as internal audit.

Agribank has also changed the organizational model of credit granting activities - the main activity of this bank. The Board of Directors of Agribank issued Decision 225/QD-HDTV-TD/2019 on the Regulations on lending to customers in the Agribank system; the General Director issued Decision No. 1225/QD-NHNo-TD/2019 on guidelines for the Regulations on lending to customers in the Agribank system. Accordingly, the department with the function of credit appraisal is independent of individuals and other departments (a) Customer relations; (b) Re-appraisal (if any); (c) Approval of credit granting decisions; (d) Control of credit risk limits, management of problem credit grants, risk provisioning and use of provisions to handle credit risks. Thus, this regulation has met the requirements of Circular 13/2018/TT-NHNN (Clause 2, Article 11 of the Law on Credit Risk Management).

16) and regulations on the authority to restructure the debt repayment period to meet the requirements of Circular 36/TT-NHNN/2014 stipulating the limits and safety ratios in the operations of credit institutions (Point d, Clause 1, Article 4). The decision to restructure the debt repayment period must be made on the principle that the person deciding to restructure the debt repayment period is not the person deciding/approving that loan" while ensuring the principles according to the COSO internal control model on separating the functions of implementing steps in the credit process to minimize risks and fraud.

In addition, the survey results show that Agribank is currently developing a draft Job Description - a document that is essential for defining job positions with specific duties and powers and has been successfully implemented at many other banks. Therefore, Agribank has not fully ensured the third principle of the COSO framework in ensuring the identification, assignment and limitation of powers and responsibilities of individuals and departments in the bank. Specifically,

It is possible that some Departments/Centers at TSC, according to current regulations, have both the function of advising and assisting the Board of Directors and the function of advising and assisting the General Director, so it is inevitable that they will face difficulties in performing their duties . Internal relations between Departments/Centers and units are still administrative in nature; functional departments have not clearly defined the linkages according to work areas, product groups, and customer types . Furthermore, Agribank has not yet developed a set of performance measurement indicators (KPIs) to be able to objectively evaluate the work results of employees.

d. Commitment to capacity

In recent times, the quality of human resources has been increasingly improved at Agribank, and average labor productivity has been increased. Compared to 2014, the scale of operations (assets, capital, outstanding loans, profits) of Agribank has more than doubled with an insignificant increase in the actual number of employees. This shows that labor productivity and the quality of human resources of Agribank have been significantly improved; specifically, average labor productivity continued to increase compared to 2018 and increased 1.5 times compared to the first year of implementing the Restructuring Plan for the period 2016 - 2020.

However, Agribank's human resources are still uneven and labor productivity is still low compared to other large commercial banks, specifically:

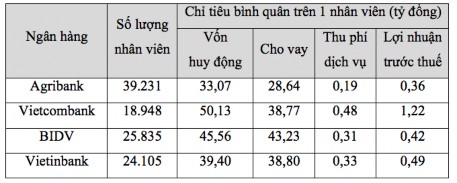

Table 2.3 Number of employees as of December 31, 2019 of some banks

Source: 2019 financial reports of banks

Thus, although Agribank is the bank with the largest number of employees in the system, compared to other large banks such as Vietcombank with only half the number of employees, it is clear that the labor productivity of Vietcombank employees is higher.