2020. This is also Mizuho's first investment transaction in Vietnam and the largest in the Southeast Asian market.

Over 50 years of construction and development, Vietcombank has grown strongly according to the model of a multi-functional bank, becoming the leading provider of financial services in Vietnam in the field of international trade finance. By the end of 2012, in addition to the head office, Vietcombank currently has 01 transaction office and 78 branches with 311 transaction offices operating in 47/63 provinces and cities nationwide. The operating network is concentrated in 26% in the Southeast region, 20.5% in the Red River Delta region, 20.5% in the South Central region, 17.9% in the Mekong Delta region, 9.6% in the North Central region, 5.5% in the Northeast region. In addition, Vietcombank also has over 1,700 correspondent banks in more than 120 countries and territories worldwide. In addition to its solid position in the wholesale banking sector with many traditional customers being corporations, general companies and large enterprises, Vietcombank has successfully built a wide and diverse distribution platform, creating momentum for the expansion of retail banking activities, serving customers who are enterprises.

small and medium enterprises, individuals with many modern and high-quality banking products and services 3 has, is and will continue to attract a large number of customers with its convenience, speed, safety and efficiency. In addition, the bank also invests in many other fields such as securities, investment fund management, life insurance, real estate business, infrastructure development, capital contribution, share purchase, etc. through subsidiaries and joint ventures.

2.1.2. Organizational structure

Vietcombank is currently organized and operates according to a model in which commercial banking plays the role of the main business segment, acting as a parent company, and other financial and non-financial activities act as subsidiaries.

Vietcombank organizational structure model (details in attached Appendix 1)

3 Foreign currency trading, card services, Internet Banking, SMS Banking, Home Banking

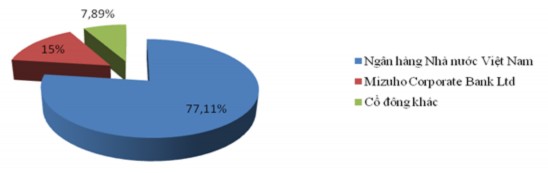

Table 2.1: List of major shareholders of Vietcombank

SHAREHOLDER NAME

TOTAL NUMBER OF SHARES | PROPORTION | |

State Bank of Vietnam (representative of state capital ownership) | 1,787,023,116 | 77.11% |

Mizuho Corporate Bank Ltd | 347,612,563 | 15% |

Other shareholders | 182,781,398 | 7.89% |

Maybe you are interested!

-

Current Status of Credit Risk Management for Individual Customers at Vietnam Technological and Commercial Joint Stock Bank - Thai Nguyen Branch

Current Status of Credit Risk Management for Individual Customers at Vietnam Technological and Commercial Joint Stock Bank - Thai Nguyen Branch -

Current Status of Lending Scale of Vietnam Technological and Commercial Joint Stock Bank

Current Status of Lending Scale of Vietnam Technological and Commercial Joint Stock Bank -

Current Status of Loan Quality for Small and Medium Enterprises at Joint Stock Commercial Bank for Foreign Trade of Vietnam, Hanoi Branch (Vietcombank Hanoi)

Current Status of Loan Quality for Small and Medium Enterprises at Joint Stock Commercial Bank for Foreign Trade of Vietnam, Hanoi Branch (Vietcombank Hanoi) -

Current Status of Liquidity at Vietnam Thuong Tin Commercial Joint Stock Bank

Current Status of Liquidity at Vietnam Thuong Tin Commercial Joint Stock Bank -

Current Status of Capital Mobilization Efficiency at Vietnam International Commercial Joint Stock Bank

Current Status of Capital Mobilization Efficiency at Vietnam International Commercial Joint Stock Bank

(Source: VCB Annual Report 2012)

Chart 2.1: Chart of ownership ratio of Vietcombank's shareholders

Table 2.2: List of related companies of Vietcombank

COMPANY NAME

INVESTMENT CAPITAL (billion VND) | PROPERTY RATIO PROPERTY (%) | |

Vietcombank Financial Leasing Company Limited | 500 | 100 |

Vietcombank Securities Company Limited | 700 | 100 |

Vietcombank Tower Company Limited | 197.65 | 70 |

Vietnamese Finance Company in Hong Kong | 116.9 | 100 |

Vietcombank money transfer company | 64.35 | 75 |

Vietcombank Bonday – Ben Thanh Company Limited | 351.61 | 52 |

Securities investment fund management joint venture company Vietcombank | 28.05 | 51 |

Vietcombank Life Insurance Company Limited | 270 | 45 |

Vietcombank Bonday Company Limited | 11.11 | 16 |

Vietcombank Member Fund 1 | 6.6 | 11 |

(Source: VCB Annual Report 2012)

2.2. Current status of competitiveness of Joint Stock Commercial Bank for Foreign Trade of Vietnam

2.2.1. Financial capacity

2.2.1.1. Equity size

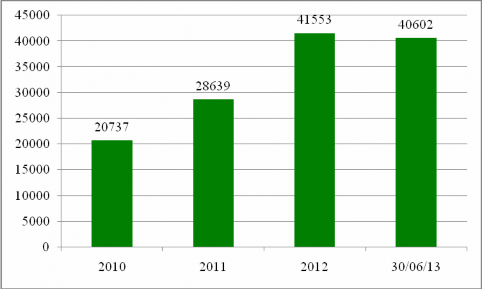

Vietcombank's equity increased continuously over the years from 2010 to June 30, 2013, specifically in 2010 it reached 20,737 billion VND, in 2011 it reached 28,639 billion VND, in 2012 it was 41,553 billion VND, and by June 30, 2013 it was 40,602 billion VND, a decrease compared to 2012 due to the impact of profits in the first 6 months of 2013.

Chart 2.2: Vietcombank's equity from 2010 to June 30, 2013

(Source: VCB Annual Reports of each year and audited report June 30, 2013)

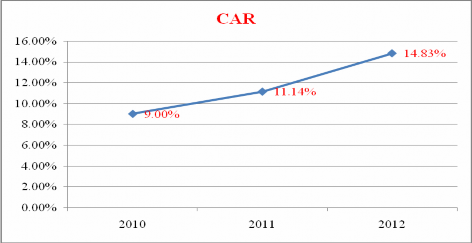

2.2.1.2. Capital adequacy ratio

Capital Adequacy Ratio (CAR) is a measure of a bank's capital safety, often used to protect depositors from bank risks and increase the stability and efficiency of the system.

Chart 2.3: Vietcombank's minimum capital adequacy ratio from 2010 to 2012

(Source: VCB Annual Reports of each year)

During the period from 2010 to 2012, Vietcombank maintained a minimum capital adequacy ratio of >9% in accordance with Basel regulations, which had a positive impact on Vietcombank's reputation and increased competitiveness, especially in international trade.

2.2.1.3. Asset quality

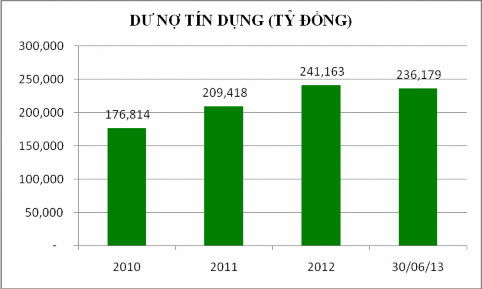

Table 2.3: Asset quality of Vietcombank

Target

Year 2010 | 2011 | 2012 | June 30, 2013 | |

Outstanding debt (billion VND) | 176,814 | 209,418 | 241,163 | 237,546 |

Bad debt (bad debt) | 5,022 | 4.251 | 5,788 | 6.651 |

Bad debt ratio/total outstanding debt | 2.83% | 2.03% | 2.4% | 2.8% |

(Source: VCB's consolidated financial statements of the years and consolidated financial statements June 30, 2013)

Vietcombank's asset quality increased continuously from 2010 to 2012. As of June 30, 2013, Vietcombank's asset quality decreased compared to 2012. Outstanding loans as of June 30, 2013 were VND 237,546 billion, an increase of 10.2% over the same period last year but a decrease of 1.5% compared to 2012. Since 2012, credit growth has been struggling due to the prolonged economic difficulties, limited demand and capital absorption capacity, the quality of business inventories has not improved, businesses do not have many new and effective business plans, so the demand for loans has decreased significantly, in which outstanding loans at Vietcombank of some customers have a large proportion of outstanding loans such as the group of customers of petroleum, seafood, etc.

In addition, fierce competition from rivals due to excess capital in most banks, the application of Circular 37/2012/TT-NHNN significantly reduced foreign currency debt.

Vietcombank's bad debt ratio increased from 2.4% in 2012 to 2.8% as of June 30, 2013, the industry's bad debt ratio was 4.65% as of June 30, 2013. The reason for the increase in bad debt is due to the negative impact of some industries on Vietcombank's customers such as frozen real estate, seafood industry facing many difficulties in export, cashew industry facing difficulties in domestic production and export market; on the other hand, Vietcombank has not closely followed the actual situation of customers to make appropriate assessments of customers' business situation and cash flow untimely proposals on borrowing and debt repayment plans.

2.2.1.4. Profitability

Chart 2.4: Vietcombank's pre-tax and after-tax profits from 2010 to June 30, 2013

(Source: VCB Annual Reports of each year and audited report June 30, 2013)

Vietcombank's pre-tax and after-tax profits from 2010 to 2012 increased year by year, except for 2011 when after-tax profits decreased slightly compared to 2010. As of June 30, 2013, following the general trend of the industry, pre-tax profits reached VND 2,603 billion, down 8% compared to the same period last year due to Vietcombank increasing its provisioning.

2.2.2 . Products and services

2.2.2.1. Capital mobilization activities

The business environment from 2010 to June 30, 2013 faced many difficulties due to the impact of the global economic crisis and the public debt crisis in the European region. The unhealthy competitive environment of credit institutions and some policy changes of the State Bank such as tightening monetary policy, anti-dollarization policy and applying interest rate ceilings, etc. have shifted the cash flow of some organizations and individuals, significantly affecting the growth rate of Vietcombank's mobilized capital. However, with the "flexible and drastic" direction of Vietcombank's Board of Directors, Vietcombank's mobilized capital has had positive changes.

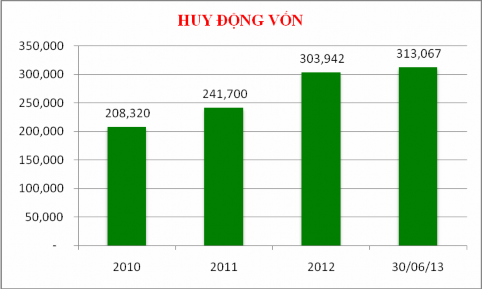

Chart 2.5: Capital mobilization data of Vietcombank from 2010 to June 30, 2013

(Source: VCB Annual Reports of each year and audited report June 30, 2013)

Vietcombank's mobilized capital in 2011 increased by 16.02% compared to 2010, in 2012 it increased quite high by 25.75% compared to 2011, as of June 30, 2013 it increased by about 3% compared to the end of 2012. Capital mobilization from the economy is still increasing, however, Vietcombank's capital mobilization in the second quarter of 2013 tends to increase more slowly because Vietcombank cuts the mobilization interest rate. As of June 30, 2013, capital mobilization from the economy reached 313,067 billion VND, an increase of 3% compared to the end of 2012 (lower than the general increase of 8.18% of the whole industry).

2.2.2.2. Credit activities

Regarding credit growth as of December 31, 2010, outstanding credit reached VND 175,814 billion, an increase of VND 35,053 billion ~ 24.9%, completing the plan set by the Board of Directors, accounting for 7.8% market share, ranking 4th in the Vietnamese commercial banking system. Short-term outstanding loans had a strong breakthrough, increasing by 30.7% while medium and long-term outstanding loans only increased by 18.8%, so Vietcombank has controlled the medium and long-term growth rate in the right direction to ensure the ratio of short-term capital use for medium and long-term loans. Outstanding foreign currency loans also increased sharply by 25.4% while outstanding VND loans only increased by 21.3%. Regarding lending to small and medium enterprises (SMEs), the proportion of outstanding loans to SMEs according to the criteria of Decree 90/CP and Decree 56/CP both met the set plan - reaching 29.6% and 17.2% respectively. Personal credit reached VND19,158 billion, up 38.9% over the previous year, accounting for 10.9% of outstanding personal loans; not yet reaching the assigned plan - the reason is that in the last months of the year, implementing the general direction on credit control, VCB had to limit consumer loans. The guarantee balance grew 38.5% and reached the target assigned by the General Director. The total outstanding interest rate support loans as of December 31, 2010 was VND8,117 billion.

By December 31, 2011, outstanding credit reached VND 208,086 billion, up 18.5%, fulfilling the planned target, maintaining a market share of nearly 8.1% of the entire banking industry. Vietcombank has controlled the foreign currency growth rate and medium and long-term growth rate to ensure liquidity and safety ratios. By currency, outstanding foreign currency in USD increased by only 7.4%; outstanding VND increased by 18.7%. By term, outstanding medium and long-term debt increased by only 4.8%, outstanding short-term debt increased by 30.2%.

Chart 2.6: Vietcombank's credit balance data from 2010 to June 30, 2013

(Source: VCB Annual Reports of each year and audited report June 30, 2013)

By December 31, 2012, outstanding credit reached VND 239,804 billion, up 15.2% (equivalent to an increase of VND 31,718 billion) compared to December 31, 2011, completing the adjusted plan and higher than the growth rate of the whole industry (reaching about 7%). VCB's credit growth in 2012 was divided into 2 stages: Stage 3 of the first year: outstanding loan growth was low. By the end of the first quarter of 2012, outstanding credit decreased by 0.6% compared to the end of 2011. The reasons were (i) Tight monetary policy, interest rates at the beginning of the year were still high; (ii) Difficult business environment so demand for imports/investment in new projects decreased. In the last 9 months of the year: outstanding loans increased rapidly, mainly focusing on short-term VND loans, mainly due to the continuous implementation of short-term loan packages with preferential interest rates for customers with good credit quality. Outstanding loans grew fastest in the fourth quarter of 2012. VND/foreign currency loan structure 68.8/31.2 consistent with the orientation of controlling foreign currency growth and encouraging VND loans. Short-term/medium-long term loan structure 62.4/37.6 consistent with Vietcombank's orientation of controlling medium-long term loan growth .

As of June 30, 2013, outstanding credit reached 236,179 billion VND, up 10.2%.