Advantage

Compact and simple organizational structure. Fast processing of documents, saving time for customers. Building and implementing a decentralized credit risk management model does not take much effort and time.

Disadvantages

Work is concentrated in one place, lacking in depth. There is no complete separation, independence of business functions, operations, credit risk management. Credit management is all remote based on reporting unit data or indirectly through credit policies, leading to many difficulties in credit risk management.

Maybe you are interested!

-

Credit risk management at Vietnam International Commercial Joint Stock Bank - Hanoi Branch - 12

Credit risk management at Vietnam International Commercial Joint Stock Bank - Hanoi Branch - 12 -

Credit risk management for personal loans at Nam A Commercial Joint Stock Bank - Quang Ninh Branch - 13

Credit risk management for personal loans at Nam A Commercial Joint Stock Bank - Quang Ninh Branch - 13 -

The Role of Risk Management in Credit Activities at Commercial Banks

The Role of Risk Management in Credit Activities at Commercial Banks -

Credit risk management at Military Commercial Joint Stock Bank, Hue Branch - 12

Credit risk management at Military Commercial Joint Stock Bank, Hue Branch - 12 -

Current Status of Credit Risk Management at Vietnam Bank for Agriculture and Rural Development

Current Status of Credit Risk Management at Vietnam Bank for Agriculture and Rural Development

3.2.3 Credit risk management methods

According to Basel II standards, there are two approaches to measuring and evaluating RRTD:

- First : The standard method used to measure credit risk is based on independent credit assessments of independent credit rating agencies. To determine the risk weight according to this method, banks are allowed to use the assessment of independent credit rating agencies (ECAI) approved by the State Bank of Vietnam. Basel II sets out 6 conditions that credit rating agencies must meet. In addition, Basel II allows banks to adjust the value of receivables and transactions according to credit risk mitigation measures (CRM) for capital calculation purposes more than Basel I.

- Second : The internal credit rating method to implement this method must have the approval of the Banking Supervisory Authority - will allow the bank to rely on its internal model estimates of risk factors, including estimated probability of default (PD), estimated loss at default (LGD), total outstanding customer debt at the time of customer default (EAD), and effective maturity (EM). In some cases, the bank is forced to apply the values given by the supervisory authority even though those values may be contrary to internal estimates.

According to the internal credit rating method, banks will divide into 5 different groups of assets in the bank book. Regarding this group of assets, Basel gives two methods: basic and advanced. According to the basic method, banks use

banks use their own estimates of PD and rely on the bank supervisor’s estimates of the other risk components. The enhanced approach, on the other hand, will have estimates of PD, LGD, EAD, and EM. However, this is subject to de minimis standards. For retail operations, there is no distinction between the enhanced and basic approaches. For both approaches, banks must always use the risk weighting function set out in the Capital Accord for capital requirements purposes. In addition to the collateral recognized in the standard approach, some other forms of collateral are also recognized in the internal credit rating approach.

3.3 Basel's view on credit risk

3.3.1 Introduction to the Basel Committee

The Basel Committee on Banking Supervision (BCBS) on banking supervision was established in 1974 by a group of central banks and supervisory agencies of 10 developed countries (G10) in Basel, Switzerland. Up to now, the members of the Basel Committee include representatives of central banks or banking supervisory agencies of the following countries: UK, Belgium, Canada, Germany, Netherlands, United States, Luxembourg, Japan, France, Spain, Sweden, Switzerland and Italy and meet four times a year. The establishment of the Basel Committee aimed to find ways to prevent a series of bank failures in the 1980s.

In addition, the Basel Committee Secretariat proposed by the Bank for International Settlements in Basel includes 15 members of the secretariat who are professional banking supervisors temporarily seconded from member financial credit institutions.

The Basel Committee does not have any supervisory authority and its conclusions have no legal force or compliance with banking supervision. Instead, the Basel Committee develops and publishes broad supervisory standards and guidelines. Another important objective of the Basel Committee is to close the international supervisory gap based on two basic principles: (1) No foreign bank may be established outside the

supervision; (2) Supervision of banking activities must be commensurate. To achieve the set objectives.

To date, the Basel Committee has issued three standards requiring minimum capital adequacy, specifically:

1998: Basel I standards issued

1999: In order to overcome the limitations of Basel I, the committee proposed a new measurement framework with 3 main pillars as well as set out 25 basic principles in banking supervision.

2004: Approval of Basel II standards

2007: Basel II standards come into effect

2010: End of transition

3.3.2 Summary of the Basel Accords

Basel I Accord

In 1988, the Basel Committee decided to introduce a capital measurement system which is referred to as Basel I or Basel Capital Standards.

The purpose of this standard is to strengthen the stability of the entire international banking system, establish a unified and equal international banking system to create fair competition among international banks.

The Basel I standards include:

Risk-based capital ratio or “Cook's Ratio”

This ratio was developed by BCBS with the aim of strengthening the international banking system in general and the initial target was internationally active banks in particular. This ratio has been implemented in more than 100 countries.

Capital Ratio (CAR) = Required Capital / Risk Weighted Assets (RWA)

According to this standard, the minimum amount of capital that a bank must retain is at least 8% of its risk-weighted assets. Determining whether a bank is well capitalized or not is based on the CAR ratio as follows:

- CAR> 10%: bank with the best capital level

- CAR > 8%: bank has appropriate capital level

- CAR < 8%: bank lacks capital

- CaR < 6%: bank has obvious capital shortage

- CAR < 2%: bank is in a state of severe capital shortage

Tier 1, Tier 2 and Tier 3 capital

The major achievement of Basel I was to provide the most common international definition of bank capital, or what is known as the bank's capital adequacy ratio. This standard stipulates:

Tier 1 Capital ≥ Tier 2 Capital + Tier 3 Capital

Tier 1 capital (mainly equity) comprises available reserves and disclosed reserves, which are considered as reserves for borrowings such as (i) permanent equity, (ii) disclosed reserves - retained earnings,

(iii) minority interests in subsidiaries on consolidated financial statements, (iv) business advantages.

Tier 2 capital (Supplementary capital of lower reliability) includes undisclosed retained earnings, asset revaluation reserves, general provisions, hybrid capital instruments, loans with concessional terms, investments in financial subsidiaries and other financial institutions.

RWA = ∑ (Assets x Risk factor of each asset in the balance sheet) + ∑ (Equivalent debt x Off-balance sheet risk level)

Tier 3 capital (For market risk) includes short-term loans

Risk-weighted capital:

Regarding the risk coefficient of assets, Basel 1 provides 4 risk levels for equivalent asset types: 0% - 20% - 50% - 100%.

After the system of indicators for credit risk management was established in 1988, the Basel Committee turned its attention to market risk in response to the increasingly specialized business activities of banks.

commercial and by 1996, Basel I was amended to include the cost of capital for market risk and was to be implemented by 1 January 1998 at the latest.

In general, the regulations in Basel I on measurement are equal because the risk level of assets is only based on the collateral and customer group, not on the size of the loan, term or creditworthiness of each customer.

Basel II Accord

In 2004, the Basel Committee introduced a new version called Basel II to overcome the limitations of Basel I and took effect from 2007, ending the transition period in 2010.

With Basel II, the standards have provided general principles for banking supervision. Therefore, Basel II is presented as a set of proposed regulations and brings a series of compliance challenges for banks around the world. The complexity of Basel II comes with international financial reporting standards and strict regulations from each place in the world. All of the above has made the implementation in banking operations very challenging.

To apply Basel II standards, commercial banks will have to redefine their business strategies and appropriate risk appetite. Applying Basel II standards in business operations will help commercial banks gain more competitive advantages through the correlation between risk and capital allocation efficiency.

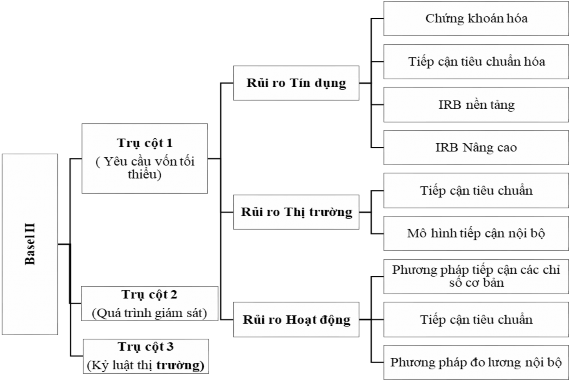

In general, Basel II has eliminated the “one size fits all” methodology in Basel I in calculating minimum regulatory capital requirements. Instead, Basel II has introduced the concept of 3 pillars including (1) Minimum capital requirements,

(2) Guidelines for principles in reviewing and supervising banking activities, (3) Transparency requirements based on minimum market information requirements.

Figure 3.2 Basel II Model

Source: Moody's Analytics Risk

Pillar 1 – Minimum Capital Requirement (8%)

Pillar 1 focuses on measuring the capital required by banks to maintain for three types of risks: credit, operational and market. For each type of risk, Basel II provides different methods for calculating the minimum capital reserve. Specifically:

- Credit risk is calculated by 3 methods:

(1) Standardized Approach (SA): uses the rating results of external independent credit rating organizations to determine the risk coefficient for different asset groups.

(2) Internal Rating based - Foundation (FIRB): uses internal data to build a probability of default model (PD model) and the parameters LGD (loss ratio), EAD (value at risk at the time of default) provided by the State Bank to calculate capital.

(3) Internal Rating based - Advanced (FIRB): banks build their own PD, LGD, EAD models to calculate minimum capital.

- Operational risk is calculated by 3 methods:

(1) The Basic Indicator Approach (BIA) calculates capital based on the average net income over 3 years, regardless of business segment.

(2) The Standardized Approach (STA) calculates capital based on dividing the bank's activities into 8 segments with different risk coefficients.

(3) The Advanced Measurement Approach (AMA) requires the use of internal loss data to build a capital calculation model.

- Market risk is calculated by 2 methods:

(1) The Standardized Measurement Approach calculates capital based on assigning certain risk factors to different business segments.

(2) Internal Model Approach uses historical data to calculate VaR (value at risk) as a basis for capital calculation.

Pillar II – Monitoring and supervision

Pillar II defines the process of overseeing the institution’s risk management framework and capital adequacy. It places specific review responsibilities on the board of directors and senior management, and strengthens internal controls and other corporate governance by regulators in different countries around the world. In Pillar II, in addition to credit, operational and market risks, Basel requires banks to identify, assess and manage other risks that banks face such as: systemic risk, strategic risk, reputational risk, liquidity risk, interest rate risk in the banking book, concentration risk, etc. To meet this requirement, banks need to have an Internal Capital Adequacy Assessment Process (ICAAP).

Basel II emphasizes the importance of bank risk management activities to develop internal capital assessment processes and set capital targets that are commensurate with the bank's risk asset profile and control environment.

Supervisors will be responsible for assessing how banks determine their capital adequacy needs relative to appropriate risks. Internal processes will then be reviewed, monitored and, where necessary, intervened. In the current environment, Pillar II requires supervisors to be more careful in their decisions regarding banks’ capital adequacy.

Pillar III – Market Principles

Pillar III enables market participants, including customers, investors, analysts, credit rating agencies, and other banks, to: assess a bank’s ability to withstand potential risks and meet its financial obligations to depositors and investors. Requires disclosure of information in a number of economic areas, including how banks calculate capital adequacy and how they assess their risk. Enhances transparency and comparability between banks.

Banks are required to disclose information focusing on key business parameters, risk management. Both qualitative and quantitative information must be disclosed. Information on capital structure and adequacy, and disclosure must include details of capital base. For credit risk, it is credit risk management and securities that must be provided.

Minimum capital requirements

Minimum capital is the risk management standard in the business activities of commercial banks. In which the minimum capital safety ratio that commercial banks must maintain is a large enough amount of capital to ensure their risky activities.

Basel II still stipulates a minimum capital adequacy ratio (CAR) of ≥ 8%. The equation for calculating the minimum capital adequacy ratio under Basel II is as follows:

≥8