between VND and USD deposits. In the long term, this shift is important for the monetary policy management solution of the State Bank, shifting from the mobilization-lending relationship to the foreign currency buying-selling relationship. However, in the short term, the decrease in foreign currency deposits while the foreign currency debt continuously increases will create pressure on the exchange rate.

Total means of payment as of August 30 increased by 9.16% compared to the target of 15-16% for the whole year, therefore, the total remaining means of payment in the last months of the year could reach about 300,000 billion VND, an average of 59,500 billion VND per month.

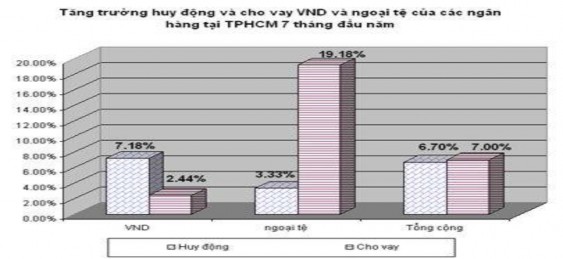

Chart 2.11: Chart showing the growth of mobilization and lending of commercial banks in Ho Chi Minh City in the first 7 months of the year.

Mobilizing at high interest rates will increase mobilization costs and reduce profits. On the other hand, to compensate for the difference in mobilization interest rates, commercial banks have increased lending interest rates. According to the State Bank of Vietnam, in October 2011, VND lending interest rates for the agricultural, rural and export sectors were about 17-19%/year, lending for other production and business sectors was about 18-21%/year, lending for non-production sectors was about 20-25%/year.

Manufacturing and trading enterprises are currently borrowing at interest rates of 18-21%. The difference between deposit and lending interest rates of commercial banks is up to 4-7%, so lending risks continue to increase when bad debts continue to rise and commercial banks

difficulties in capital sources to provide credit. In fact, up to this point, credit of the commercial banking system has only increased by 8.61% compared to the beginning of the year, less than half of the credit growth target that the State Bank of Vietnam set at the beginning of the year.

The climax of capital mobilization by all means is the increase in interest rates for gold and a series of foreign currencies "other than USD" by commercial banks. This action is considered quite clever because it avoids the interest rate ceiling of 14% for VND and the ceiling of 2% for USD. It also helps commercial banks diversify their sources of capital mobilization. However, because the main purpose is liquidity, commercial banks will find it difficult to avoid exchange rate risks, because most small commercial banks lack experience in managing foreign exchange rates other than USD.

According to the State Bank, medium and long-term loans account for a large proportion of about 77% of total loans , while the capital mobilized by banks is mainly short-term, so liquidity risks may arise. It is clear that commercial banks are lacking medium and long-term capital. This is not a new phenomenon because when inflation increases, the Vietnamese currency depreciates, people's lives become increasingly difficult, ... the mentality of depositing money for a short term is still the priority choice because when needed, it is easier to withdraw and you get a high interest rate.

Although the real estate market has improved, it is still heavily affected by the 2008 financial crisis . Many projects do not have capital to implement, some businesses sell off to recover capital, pay interest and principal to banks. This causes real estate prices to fall seriously, this is also the time

good for people to buy land and houses at cheap prices. That's why there is also a number of deposits withdrawn from banks.

In the first months of the year, the world gold price fluctuated strongly and abnormally, combined with people's gold buying habits, causing domestic gold prices to increase rapidly. Gold prices changed continuously, and Vietnamese people had the habit of storing cash and gold at home, so buying and selling gold to enjoy the difference occurred quite a lot, pushing domestic gold prices higher than world gold prices. The drastic implementation of the Government's solutions to stabilize gold prices and the domestic gold market has

contributing to bringing domestic gold prices closer to world gold prices; speculators are no longer able to manipulate the market; banks have begun to buy gold from the domestic market to compensate for the amount of gold sold, reducing pressure on gold imports, saving foreign currency, reducing pressure on exchange rates, helping to stabilize the capital mobilized by commercial banks.

The exchange rate also fluctuates a lot, especially the USD/VND exchange rate. When importing goods from abroad, businesses need to pay for the goods when due, but because the USD/VND exchange rate on the black market is much higher than the listed price at commercial banks, the amount of foreign currency in cash outside the bank is very high. Banks do not have foreign currency to sell, so businesses find it difficult to buy foreign currency for payment, and are forced to buy on the black market. This pushes the exchange rate even higher. However, the issuance of Resolution 11/NQ-CP dated February 24, 2011 by the Government has reduced speculation and hoarding, increasing the amount of foreign currency in cash at commercial banks. As of September 29, 2011, foreign currency deposits of credit institutions at the State Bank increased by 45.1% compared to the end of August 2011, equivalent to an increase of 586 million USD.

The State Bank of Vietnam affirmed that the foreign currency flow of the economy and the banking system has many positive changes. The surplus of the international balance of payments, the consolidation of the state foreign exchange reserves and the foreign currency liquidity of the banking system in recent months are important bases for stabilizing the USD/VND exchange rate and foreign currency interest rates in the domestic market in the remaining months of 2011.

According to Directive No. 01/CT-NHNN dated March 1, 2011 of the State Bank, as of December 31, 2011: the maximum outstanding loan ratio for non-production of commercial banks is 16% of total outstanding loans, thus creating pressure forcing commercial banks to make efforts to recover loans related to non-production sectors.

2.5. Evaluation of capital mobilization results at some commercial banks in Ho Chi Minh City.

2.5.1. Advantages and achievements:

Currently, the banking and finance sector of the country in general and Ho Chi Minh City in particular is facing many difficulties and challenges. However, there are also some advantages that must be mentioned such as:

Ho Chi Minh City is the largest financial and banking center in Vietnam , the city leads the country in the number of banks and financial and credit relations turnover. The revenue of the city's banking system accounts for about 1/3 of the total revenue nationwide.

Ho Chi Minh City is the largest economic center of the country , many foreign capital flows in, many foreign companies are established in Ho Chi Minh City. This is a dynamic economic development area, people's income is quite high compared to other regions, so a large amount of money is deposited in banks.

Ho Chi Minh City has an interbank electronic payment center implemented through the State Bank, with high data processing speed, safety, speed, and accuracy. The operating time and clearing payment of the State Bank of Vietnam, Ho Chi Minh City Branch is extended to 4:30 p.m.

The number of banks is quite large today , on one street there are sometimes 5-6 different banks. In addition, the number of ATMs is about 1,800, very convenient for transactions via ATM cards such as: withdrawing money, paying phone bills, saving money on ATMs without having to go to the bank to deposit money, ...

Political and social stability has a great impact on the psychology and confidence of depositors. In a country with stable politics, people will feel secure in living and working, and will trust and feel secure in depositing their money in banks. From there, it helps banks to perform their functions well, providing capital to serve the development of the economy.

Changes in fiscal and monetary policies and government regulations also affect the ability to attract capital. During the financial crisis in 2008, the government used financial tools proactively and flexibly.

Active and effective, Vietnam has overcome the crisis, our economy is gradually recovering.

The current technical facilities are invested in very satisfactorily by commercial banks , with modern machinery, equipment, technology and a wide and impressive branch network... creating peace of mind and trust for customers.

An intangible asset that needs to be mentioned is the brand of the bank that has been built over many years; a bank with a team of enthusiastic, open, dynamic employees who are knowledgeable about products and services will attract more customers. Currently, there are many reputable banks that have created trust with people as well as businesses and economic organizations such as: Vietinbank, Vietcombank, Agribank, BIDV, ACB, DongAbank, Sacombank...

Achievements:

Capital mobilized by commercial banks has increased in recent times.

After a period of operation, the scale of mobilized capital of commercial banks has increased significantly compared to before. The mobilized capital in 2008 was 585,339.4 billion VND, and by 2010 it had reached 1,014,900 billion VND.

Faced with the pressure of increasing mobilized capital, commercial banks have proactively sought outlets with many effective lending products that attract customers. Previously, unsecured lending products were only developed in foreign banks and some large joint stock commercial banks. Now, most banks are promoting unsecured lending in many forms such as: overdraft via ATM cards, loans for car purchases, home purchases, etc., showing the positivity in the business activities of banks. Despite difficulties and challenges, the commercial banking system in Ho Chi Minh City has had good growth, achieved encouraging results, and promoted the development of the country.

Table 2.7: Capital mobilization data at some commercial banks from 2008 to 2010.

Unit: billion VND

2008 | 2009 | 2010 | |

Vietcombank | 196,507 | 225,983 | 264,290 |

Vietinbank | 174,905 | 220,591 | 339,699 |

BIDV | 184,542 | 212,223 | 251,924 |

Asia | 75,113 | 98,355 | 198,000 |

Sacombank | 58,635 | 86,335 | 126,203 |

Techcombank | 51,661 | 67,383 | 95,574 |

East Asia | 29,797 | 36,714 | 47,756 |

VIBank | 23,958 | 34,210 | 59,564 |

SCB | 34,606 | 48,902 | 54,439 |

Habubank | 19,961 | 25,470 | 33,272 |

Trustbank | 2.016 | 4,631 | 10,254 |

Dai A Bank | - | 5,266 | 6,080 |

Maybe you are interested!

-

Developments in Capital Mobilization, Investment, Deposits, and Lending on the Interbank Market Up to September 2012

Developments in Capital Mobilization, Investment, Deposits, and Lending on the Interbank Market Up to September 2012 -

Capital Mobilization and Lending Situation of Acb Can Tho

Capital Mobilization and Lending Situation of Acb Can Tho -

Solutions to enhance capital mobilization at Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch - 9

Solutions to enhance capital mobilization at Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch - 9 -

Solutions to Improve Capital Mobilization Efficiency at Vietnam Foreign Trade Bank

Solutions to Improve Capital Mobilization Efficiency at Vietnam Foreign Trade Bank -

Solutions to enhance capital mobilization at Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch - 8

Solutions to enhance capital mobilization at Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch - 8

“Source: Compiled from annual reports of commercial banks over the years”

The profits of commercial banks have increased dramatically in the past few years, always at the highest level in the economy. Although the national and world economies are facing many difficulties and fluctuations after the financial and monetary crisis, the banking sector still has high profits, typically in 2010, VCB's pre-tax profit was 5,400 billion, Vietinbank was 4,598 billion, BIDV was 4,600 billion, Sacombank was 2,400 billion,... Even some small-scale banks such as Military Bank, Maritime Bank, ... also made hundreds of billions of dong in profit.

The competitiveness of commercial banks is increasing.

Since Vietnam joined the WTO, the competition between banks has become increasingly fierce, not only domestic commercial banks compete with each other but also with foreign banks. Although the competition is still weak, domestic banks

still has certain advantages such as a widespread network, not only in big cities but also to districts and communes.

Currently, commercial banks have branches or transaction offices in all provinces, cities, industrial parks, and export processing zones. Most commercial banks operate in the direction of modernization, applying modern technology, promoting service activities, and the number of ATM and POS locations is increasing. By the end of 2010, the number of cards in the entire system nationwide reached 28.5 million with more than 11,000 ATMs and 50,000 POS.

The payment system through banks and non-cash payments has also attracted a large amount of capital : people have more and more conditions to access banking products and services, the opening of payment deposit accounts by individuals and economic organizations has brought a temporary amount of idle capital with low costs for commercial banks to operate. The legal framework for payment activities of banks is constantly being improved as a basis for commercial banks to invest in technological innovation, improve processes, especially the application of information technology in banking activities has helped commercial banks expand the types and methods of service provision; technical facilities are increasingly improved.

Flexible interest rate policy, in line with market developments . Based on the basic interest rate of the State Bank, credit institutions proactively adjust deposit interest rates and lending interest rates within the permitted fluctuation range, ensuring safety and efficiency regulations in banking business, contributing to the good implementation of the State Bank's monetary and financial policies.

Foreign exchange management policy has been gradually liberalized , in line with international practices, initially meeting the requirements of administrative reform and enterprise law in clearly defining the rights and obligations of enterprises; creating more openness for foreign economic activities, helping the State Bank have conditions to research and formulate policies and mechanisms according to the model of a modern central bank.

The exchange rate policy was initially adjusted relatively flexibly according to the supply and demand relationship of foreign currency , reflecting relatively accurately the purchasing power of VND, and the correlation.

between VND and foreign currencies of countries having trade and investment relations with Vietnam. Flexible exchange rate adjustment creates favorable conditions for commercial banks and the State Bank to increase foreign currency purchases from the market, meeting most of customers' foreign currency needs, ensuring the goal of increasing the state's foreign exchange reserves.

2.5.2. Difficulties and problems affecting capital mobilization:

Besides the achievements, commercial banks also face the following difficulties and problems:

People's habit of storing gold and foreign currency : cultural environment is a decisive factor in living habits and customs. In developed countries, non-cash payments and the use of banking services are popular, but in developing countries like Vietnam, people have long had the habit of keeping money, gold, foreign currency, etc., which limits the amount of capital attracted to banks.

Due to the large number of banks operating in Ho Chi Minh City, there is a shortage of human resources , especially after joining the WTO, many foreign banks have been established in Ho Chi Minh City, causing a brain drain. Many talented and capable workers have jumped to work in foreign banks. Newly established commercial banks that want to attract talented workers must offer high and attractive salaries, while banks that want to retain their employees must increase salaries to be equal to or higher than the salaries offered by newly established commercial banks, which pushes up labor costs.

The instability of the socio-economic situation : high inflation, gloomy economic situation, businesses have difficulty accessing bank capital. In this situation, the Government is forced to implement a tight monetary policy, resulting in negative real interest rates and controlled deposit interest rate ceilings.

The narrowing of the outstanding non-production credit ratio to 16% as of December 31, 2011 has caused commercial banks to urgently collect debts and stop lending medium and long term, especially lending related to the real estate sector. This has made businesses even more miserable because although the real estate market has shown signs of recovery, its development is not sustainable, and projects under construction do not have capital to implement.