transfer products, goods and services to buyers, orderers and receive from them a corresponding amount of money.

The sales process is divided into 2 stages:

- Stage 1: Delivering products, goods or providing services to buyers. At this stage, the goods are still owned by the business and have not been identified as consumed.

- Phase 2: The buyer pays or accepts payment at this point, the goods are determined to be consumed and at the same time the sales process ends.

Maybe you are interested!

-

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1 -

Completing revenue accounting and determining business results at Ha Lam Coal Joint Stock Company - Vinacomin - 16

Completing revenue accounting and determining business results at Ha Lam Coal Joint Stock Company - Vinacomin - 16 -

Completing revenue and cost accounting and determining business results at Nakashima Vietnam Co., Ltd. - 14

Completing revenue and cost accounting and determining business results at Nakashima Vietnam Co., Ltd. - 14 -

Accounting for revenue, expenses and determining business results at Saigon Real Estate Joint Stock Company - 1

Accounting for revenue, expenses and determining business results at Saigon Real Estate Joint Stock Company - 1 -

Completing the accounting of revenue, expenses and determining business results at Huong Duong Tourism Development and Service Company - 10

Completing the accounting of revenue, expenses and determining business results at Huong Duong Tourism Development and Service Company - 10

In reality, these two stages rarely occur at the same time but are largely separated in space and time.

* Methods of sales and payment for goods.

a) Sales methods:

The sales method has a direct impact on the use of accounting accounts reflecting the situation of finished products and goods being exported. At the same time, it is decisive in determining the time of sale and forming sales revenue and saving sales costs to increase profits. Currently, businesses are applying the following sales methods:

Direct sales: is the method of delivering goods to buyers directly at the warehouse (or directly at workshops without going through the warehouse) of the enterprise. The number of goods when delivered to the customer is officially considered consumed and the seller loses ownership of these goods. The buyer pays or accepts to pay for the goods that the seller has delivered.

Selling goods by consignment, agent, consignment: Agent and consignment sales are the methods in which the owner of the goods (the agent) delivers the goods to the agent or consignee (called the agent) for sale. The agent will receive agency remuneration in the form of commission or price difference.

Selling by installments: is a method of selling goods with multiple payments. The buyer will pay the first payment at the time of purchase. The buyer agrees to pay the remaining amount in installments in the following periods and must pay a certain interest rate. Usually, the amount paid in the following periods is equal, including a part of the original revenue and a part of the deferred interest.

According to the installment method in terms of accounting, when the goods are delivered to the buyer, the transferred quantity is considered consumed. In essence, only when the buyer has paid in full for the goods does the business lose ownership.

b) Payment methods

- Payment in cash.

- Non-cash payment: payment by bank deposit or other forms such as bartering goods for goods.

1.4. Basic contents of revenue accounting and determining business results.

1.4.1. Accounting for revenue and revenue deductions

Sales and service revenue

Documents used:

+ Sales invoice (VAT invoice)

+ Warehouse delivery note

+ Minutes of handover of goods and finished products

+ Detailed books, general ledgers…

+ Tax calculation documents

+ Cash receipt

+ Bank statement.

Account used: Account 511: Revenue from sales of goods and provision of services Details: Account 5111: Revenue from sales of goods

Account 5112: Revenue from sales of finished products

Account 5113: Service revenue Account 5114: Subsidy revenue

Account 5117: Real estate business revenue

This account is used to reflect the revenue and service provision of an enterprise in an accounting period of production and business activities from the following transactions and operations:

Sales : Sales of products manufactured by the enterprise, sales of purchased goods and sales of investment real estate. Conditions for recording sales revenue: Sales revenue is recorded when it simultaneously satisfies the following 5 conditions: According to standard No. 14 (issued and announced under Decision 149/2001/QD-BTC):

Sales : Sales of products manufactured by the enterprise, sales of purchased goods and sales of investment real estate. Conditions for recording sales revenue: Sales revenue is recorded when it simultaneously satisfies the following 5 conditions: According to standard No. 14 (issued and announced under Decision 149/2001/QD-BTC):

- The enterprise has transferred the significant risks and rewards of ownership of the products or goods to the buyer.

- The enterprise no longer holds the right to manage the goods as the owner of the goods or the right to control the goods.

- Revenue is determined to be relatively certain.

- The enterprise has obtained or will obtain economic benefits from the sale transaction.

row.

- Identify costs associated with sales transactions.

Service provision : Perform the work agreed upon in the contract.

one period, or many accounting periods such as providing transportation services, tourism, leasing fixed assets under the operating lease method... Conditions for recognizing revenue from providing services: Revenue from service provision transactions is recognized when the results of that transaction can be reliably determined.

In case the service provision transaction involves multiple periods, revenue is recorded in the period based on the results of the work completed on the date of the Balance Sheet of that period. The result of the service provision transaction is determined when the following four conditions are simultaneously satisfied:

- Revenue is determined relatively certainly.

- Ability to obtain economic benefits from the transaction of providing that service.

- Determine the part of work completed on the date of the Balance Sheet

- Determine the costs incurred for the transaction and the costs to complete the transaction to provide that service.

Accounting for sales revenue and service provision must respect the following regulations:

- Sales and service revenue is determined at the fair value of amounts received or to be received from transactions and revenue-generating activities such as selling products, goods, investment real estate, providing services to customers, including surcharges and additional fees outside the selling price (if any).

- In case an enterprise has sales revenue and service provision in foreign currency, it must convert foreign currency into Vietnamese Dong or the official currency used in accounting at the actual transaction exchange rate or the average transaction exchange rate on the interbank foreign exchange market announced by the State Bank of Vietnam at the time the economic transaction occurs.

- Net sales and service revenue that an enterprise makes during the accounting period may be lower than the initially recorded sales and service revenue due to the following reasons: The enterprise provides trade discounts, reduces the price of goods sold to customers or returns of sold goods (due to failure to ensure quality and specifications, recorded in economic contracts) and the enterprise must pay special consumption tax or export tax, VAT according to the direct method calculated on the actual sales and service revenue that the enterprise made during the accounting period.

- For products, goods and services subject to VAT under the deduction method, sales revenue and service provision is the selling price excluding VAT.

- For products, goods and services not subject to VAT or subject to VAT under the direct method, sales revenue and service provision is the total payment price.

- For products and goods subject to special consumption tax and export tax, sales revenue and service provision revenue includes special consumption tax and export tax.

- For businesses that record sales using the commission selling method, sales revenue and service provision revenue is the commission amount received.

- For enterprises that receive processing contracts, the processing fee received is only reflected in sales revenue and service provision, not including the value of materials and goods received for processing.

- In case the enterprise sells goods by installment payment, the revenue from sales and service provision is paid immediately, the interest on installment payment is recorded in the financial operating revenue of the period.

- For revenue from leasing assets with pre-received rental payments for many years, revenue from sales and provision of services recorded in the fiscal year is determined based on the total amount received divided by the number of periods receiving pre-receipt payments.

- For enterprises providing services at the request of the State and receiving subsidies from the State, the revenue from sales and provision of services is the amount of money subsidized by the State.

- In case the enterprise has issued invoices and collected sales proceeds but has not yet delivered them to the customer at the end of the period, it is recorded in the customer's receivable account.

- Do not record in account 511 the following cases:

+ Value of goods, materials, and semi-finished products delivered to outside parties for processing.

+ Value of products, goods and services provided between the company, parent company and dependent accounting units.

+ Value of products, goods and services provided to each other between the corporation and its member units.

+ Value of products, goods being sent for sale, completed services provided to customers but not yet determined as sold.

+ Value of goods sent for sale by agent or consignment (not yet determined as sold)

+ Financial revenue and other income are not considered sales and service revenue.

Internal sales revenue

Account used: Account 512: "Internal sales revenue", has 3 sub-accounts: Account 5121: Sales revenue of goods

Account 5122: Revenue from selling finished products Account 5123: Revenue from providing services

This account is used to reflect the revenue of products, goods, services and internal consumption within the enterprise. Internal consumption revenue is the economic benefit obtained from the sale of goods, products, and provision of internal services between dependent accounting units within the same company or corporation at internal selling prices.

Account 512 has no ending balance.

Trade discount.

Account used: Account 521: Trade discount

This account is used to reflect the trade discount that the enterprise has deducted or paid to the buyer because the buyer has purchased goods and services in large quantities and according to the agreement, the seller will give the buyer a trade discount (recorded on the economic sales contract or purchase and sale commitments).

Account 521 has no ending balance.

Returned goods

Account used: Account 531

This account is used to reflect the value of products and goods returned by customers due to the following reasons: Violation of commitments, violation of economic contracts, poor quality goods, loss of quality, incorrect type and specifications... The value of returned goods reflected in this account will adjust the actual sales revenue realized during the business period to calculate the net revenue of the volume of products and goods sold during the reporting period.

Returned goods are returned to finished goods warehouse and processed according to current tax and financial policies.

Account 531 has no ending balance.

Sale price.

Account used: Account 532

This account is used to reflect the actual sales discount that arises and the handling of sales discount during the accounting period. Sales discount is a deduction for the buyer due to poor quality, degraded or non-conforming products and goods according to the provisions of the economic contract.

Only reflect in this account the deductions due to the approval of discounts after the sale and issuance of invoices (off-invoice discounts) due to poor quality or degraded goods.

Account 532 has no ending balance.

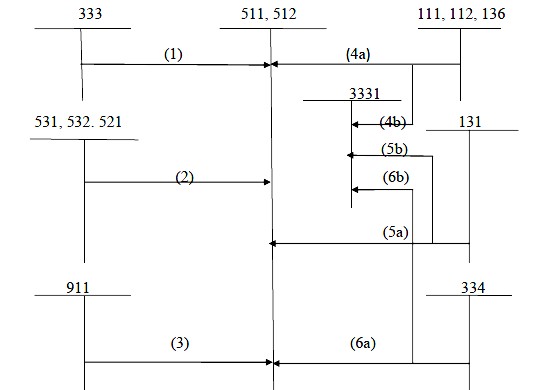

Sales revenue accounting diagram by method:

Diagram 01: General accounting of sales revenue and service provision (VAT by deduction method)

Note:

(1) Export tax, special consumption tax payable to the state budget, VAT payable by direct method

(2) At the end of the period, transfer of trade receivables, returned goods, and sales discounts arising during the period

(3) End of period net revenue transfer (4a) Revenue from sales of products and goods

(4b) VAT on output goods from selling products and goods (5a) Sales by barter method

(5b) Output VAT by barter method (6a) Paying wages in products and goods