multiplied and checked then transferred to the construction planning department for checking and review. Then transferred back to the accounting department for the chief accountant to approve as a basis for making payment vouchers.

- Product salary according to contract: Every week, the construction management board finalizes the salary for the work done by the contract team, transfers it to the construction accountant for checking, then transfers it to the construction planning department for approval, then transfers it back to the accounting department for the chief accountant to approve and make a payment voucher.

* Accounting principles

- In case of daily wage payment, accountant records:

Upon receiving the request for payment of daily wages from the construction management board, the accountant will make a payment voucher and make the following entries:

Debit account 622: Workers' salary expenses Credit account 111: Amount payable

Example 1 : On October 4, 2012, the accountant received a request for payment of daily wages from the House Foods project in the amount of 12,894,000 VND. At that time, the accountant made a payment voucher and recorded:

Debit account 622: 12,894,000

Credit account 111: 12,894,000

Example 2:On October 19, 2012, the accountant received a request for payment of daily wages from the House Foods project in the amount of 20,250,000 VND. At that time, the accountant made a payment voucher and recorded:

Debit account 622: 20,250,000

Credit account 111: 20,250,000

- In case of paying salary to the contract team

Upon receiving the set of documents requesting salary payment to the contract team, the accountant creates a payment voucher and records it in account 3388.

Debit account 622: Total salary paid to the contract team

Credit account 3388: Total salary paid to the contract team

After approval of expenditure, accountant records:

Debit account 3388: Total salary paid to the contract team.

Credit account 111: Total salary paid to the contract team.

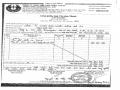

Table 2.4: Ledger account 622

Construction and Trade Joint Stock Company 2 Tax code: 0300584155 36 Ung Van Khiem, Ward 25, Binh Thanh District, Ho Chi Minh City

ACCOUNT DETAILS

From October 1, 2012 to December 31, 2012 Account name: Direct labor costs Number: 622 House Foods project

Unit: VND

Document

Content | TK DU | Number of occurrences | |||

Day | Number | In debt | Have | ||

Beginning balance: | |||||

10/04/12 | 0010/10/ PCCT | Salary of House Foods employees from 24/07 --> 10/08/12 | 1111 | 12,894,000 | |

10/19/12 | 0164/10/ PCCT | Salary of House Foods employees from 13/09 --> 05/12/12 | 1111 | 20,250,000 | |

……… …. | ……… … | ……………….. | ….. | ………… | |

12/31/12 | KC 622/12 | KC CP Account 622 to 1541, December 31, 2012 | 1541 | 2,723,134,171 | |

Total number of occurrences: | 2,723,134,171 | 2,723,134,171 | |||

Ending balance: | |||||

Maybe you are interested!

-

Accounting for revenue, expenses and determining business results at Saigon Real Estate Joint Stock Company - 1

Accounting for revenue, expenses and determining business results at Saigon Real Estate Joint Stock Company - 1 -

Completing the accounting of revenue, expenses and determining business results at Huong Duong Tourism Development and Service Company - 10

Completing the accounting of revenue, expenses and determining business results at Huong Duong Tourism Development and Service Company - 10 -

Accounting for revenue, expenses and determining business results at Hoang An private enterprise - 12

Accounting for revenue, expenses and determining business results at Hoang An private enterprise - 12 -

Accounting for revenue, expenses and determining business results at Thien Thanh Logistics Company Limited - 11

Accounting for revenue, expenses and determining business results at Thien Thanh Logistics Company Limited - 11 -

Completing the accounting of revenue, expenses and determining business results at Huong Duong Tourism Development and Service Company - 2

Completing the accounting of revenue, expenses and determining business results at Huong Duong Tourism Development and Service Company - 2

Ho Chi Minh City, December 31, 2012

Chief Accountant

c) General manufacturing costs

General production costs are collected separately for each project and project item. Including all other costs incurred such as: Cost of transporting construction materials and equipment, outsourcing costs, salary costs for construction management board, electricity and water costs for construction, construction security costs, subcontracting costs, other cash costs, etc.

User account

Construction and Trade Joint Stock Company 2 uses account 627 (general production costs): reflecting all general production costs. This account is opened in detail for each project and is included in the cost of construction and installation products.

Certificate of use

- MMTB rental calculation table - CCDC

- Material transport note, CCDC, MMTB

- Material import and export vouchers, MMTB-CCDC

Document circulation order

- MMTB-CCDC rental cost: Every month, the lessor sends a rental calculation sheet to each project. The warehouse keeper and project accountant check the number of MMTB-CCDC rented, confirm the rental, transfer to the commander for confirmation and then transfer to the machinery and equipment department for payment procedures.

- Cost of transporting materials, MMTB - CCDC: When there is a material transport note, MMTB - CCDC, the supply department or MMTB department will transfer it to the accountant of each project to carry out payment procedures.

After receiving the payment request, the construction accountant will make an accounting voucher and make the following entries:

Debit account 627 (Open details for each expense item) Debit account 1331: Deductible VAT

Credit account 331: Payable to sellers (this account is opened in detail for each unit)

Example 1:On October 10, 2012, the accountant received a payment request from Le Phuong Gia Informatics Trading and Service Co., Ltd. regarding the photocopy machine rental fee for August + September (Appendix 04).

of House Foods project, the rental value is 1,980,000 VND (including 10% VAT). The accountant prepares an accounting voucher and records:

Debit account 6277: 1,800,000

Debit account 1331: 180,000

Credit account 331: 1,980,000

Example 2 : On October 6, 2012, the accountant received a payment request from the supply department for the cost of processing bricks for the House Foods project worth 2,745,600 VND. The accountant prepared an accounting receipt and recorded:

Debit account 6277: 2,745,600

Credit account 331: 2,745,600

- In case the company assigns subcontractors to other items in a project. Upon receiving the work volume settlement sheet confirmed by the project management board, the accountant records:

Debit account 6277: Value of completed work volume. Debit account 133: Deductible VAT.

Credit account 3388: Payable to subcontractors.

Example 3:On October 4, 2012, the company paid 480,000 VND for drinking water to the House Foods Project Management Board. The accountant recorded:

Debit account 6278: 480,000

Credit account 331: 480,000

Table 2.5: Ledger account 627

Construction and Trade Joint Stock Company 2 Tax code: 0300584155 36 Ung Van Khiem, Ward 25, Binh Thanh District, Ho Chi Minh City

ACCOUNT DETAILS

From 01/10/2012 to 31/12/2012

Account Name: General Manufacturing Costs

Number: 627 Tel: House Foods Construction

Unit: VND

Document

Content | TK DU | Number of occurrences | |||

Day | Number | In debt | Have | ||

Opening balance | |||||

10/04/12 | 01/10/CTHFS | Drinking water allowance for HF CTR Executive Committee September 12 | 331 | 480,000 | |

10/06/12 | 10/27/CTHFS | HF brick processing fee, contract 78111 | 331 | 2,745,600 | |

10/10/12 | 02/10/CTHFS | Photocopier rental payment for August + September of House Foods - Le Phuong Gia Company - Contract 412 | 331 | 1,800,000 | |

… … … | … … … | … … … | … | … … … | … … … |

12/31/12 | KC 627/12A | KC CP Account 627 to 1541, December 31, 2012 | 29,731,703,917 | ||

Total number of occurrences | 29,731,703,917 | 29,731,703,917 | |||

Closing balance | |||||

Ho Chi Minh City, December 31, 2012

Chief Accountant

d) General accounting of construction production costs

At the end of the accounting period, collect all construction and installation production costs into account 1541 (Unfinished production and business costs).

Debit account 1541: details for each project

There are accounts 621, 622, 627: details for each project

Example:On December 31, 2012, the accountant transferred the December construction production costs of the House Foods project.

Debit account 154 (Ctr House Foods): 45,128,342,062

12,673,503,974 | |

There is account 622 (Ctr House Foods): | 2,723,134,171 |

There is account 627 (Ctr House Foods): | 29,731,703,917 |

Summary of account 154: summary of works

STT

Project name | Opening balance | Debt generation | Arising has | Closing balance | Note | |

01 | ||||||

02 | ||||||

Total |

2.4.5.1.2

- The company uses accounting software, so at the end of the accounting period, the general accountant performs the transfer of production costs of each project to record the cost of goods sold.

- Account used: Account 632 – Cost of goods sold.

Example:On December 31, 2012, the general accountant transferred the construction production costs of the House Foods project in December 2012.

Debit account 632 (Ctr House Foods): 45,128,342,062

Credit account 154 (Ctr House Foods): 45,128,342,062

2.4.5.2

The Company Office does not use account 641.

2.4.5.3

2.4.5.3.1

- Payment voucher.

- IOU.

- Payment authorization.

- Advance payment voucher.

- Payment request form.

- Payroll payment.

2.4.5.3.2

Account 642: Business management expenses.

- Account 6421: Management staff costs.

- Account 6422: Management material costs.

- Account 6423: Office supplies costs.

- Account 6424: Fixed asset depreciation expenses.

- Account 6425: Taxes, fees, charges.

- Account 6437: Cost of outsourced services.

- Account 6428: Other cash expenses.

All arising transactions are paid by the enterprise in cash or bank deposits except for two amounts of fixed asset depreciation and office equipment allocation, which are tracked in the detailed books of Account 214 and Account 1421.

2.4.5.3.3

Management staff costs: At the end of the month, the payroll accountant prepares the payroll and submits it to the Chief Accountant and General Director for approval, then transfers it to the bank deposit accountant to proceed with paying the employees' salaries. After that, the bank deposit accountant enters data into the bank deposit section and issues 3 copies of the Payment Order: Copy 1: Bank deposit accountant keeps; Copy 2: Delivers to the bank; Copy 3: Internal storage.

3 copies of the Payment Authorization will be submitted to the Chief Accountant and General Director for approval, then 1 copy will be transferred to the bank with the transfer list attached.

Example:On November 30, 2012, based on the payroll provided by the payroll accountant and approved by the Chief Accountant and General Director, the bank deposit accountant prepared a payment order and submitted it to the Chief Accountant and General Director for approval, then transferred it to BIDV bank with the transfer list attached. The accountant entered the data into the bank deposit section to record the business management costs.

Debit account 6421: 650,193,269

Credit account 1121: 650,193,269

Fixed asset depreciation cost: To monitor the fixed asset situation, the Company is currently applying the straight-line depreciation method. Fixed asset depreciation has been entered as soon as entering the "Fixed Asset Accounting" screen. At the end of the month, the fixed asset accountant will make entries to allocate fixed asset depreciation to the business management costs. The software will automatically calculate the straight-line depreciation value that the company has selected and update the general journal, general ledger and detailed books of related accounts.

Office supplies costs, taxes, fees, outsourced services and cash expenses

other:

- Accounting department after receiving Payment request, VAT invoice from the supplier

Providing goods and services for business management and tax receipts, accountants will save documents and enter data into the software.

- If the payment is delayed, the accounts receivable accountant enters information about the supplier, amount owed, payment term, etc. into the purchasing section.

- If the daily payment costs are in cash: based on the payment request file signed and approved by the chief accountant and the General Director, the cash accountant enters data into the cash section and issues a payment voucher as a copy. The payment voucher will be transferred to the cashier. The cashier will make the payment to the supplier. At the end of the month, the cashier returns the payment vouchers to the cash accountant to close into a stack and store.

- If the cost is paid immediately by bank deposit, 3 copies of the Payment Order will be issued: Copy 1: kept by the bank deposit accountant; Copy 2: given to the bank; Copy 3: kept internally. The Payment Order will be submitted to the Chief Accountant and General Director for approval, then 1 copy will be transferred to the bank to transfer money to the supplier.