Trust

satisfaction

Loyalty

Bank image

Maybe you are interested!

-

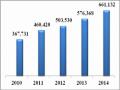

Completing the personal credit rating model at Saigon Commercial Joint Stock Bank - 12

Completing the personal credit rating model at Saigon Commercial Joint Stock Bank - 12 -

Factors affecting customer loyalty to international payment services at Asia Commercial Joint Stock Bank - 12

Factors affecting customer loyalty to international payment services at Asia Commercial Joint Stock Bank - 12 -

Solutions to increase individual customer loyalty at Vietnam Joint Stock Commercial Bank for Industry and Trade by 2018 - 2

Solutions to increase individual customer loyalty at Vietnam Joint Stock Commercial Bank for Industry and Trade by 2018 - 2 -

Building a Model of Indicators Affecting the Business Efficiency of the Military Commercial Joint Stock Bank.

Building a Model of Indicators Affecting the Business Efficiency of the Military Commercial Joint Stock Bank. -

Applying SERVQUAL model to evaluate card service quality at Vietnam Joint Stock Commercial Bank for Investment and Development - Hoa Binh Branch - 14

Applying SERVQUAL model to evaluate card service quality at Vietnam Joint Stock Commercial Bank for Investment and Development - Hoa Binh Branch - 14

Perceived service quality

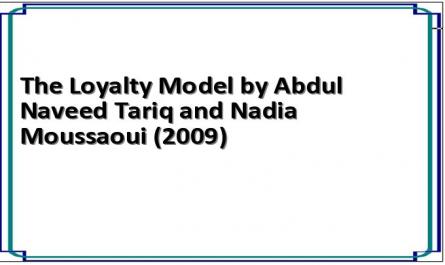

Figure 1.5 Loyalty model of Abdul Naveed Tariq and Nadia Moussaoui (2009)

(Source: Abdul Naveed Tariq and Nadia Moussaoui (2009), The Main Antecedent of Customer Loyalty in Moroccan Banking Sector )

1.4. Some factors affecting customer loyalty and research hypothesis:

After preliminary research on theoretical basis, the author found that Customer Loyalty in retail banking services at BIDV can be affected by the following four factors:

1.4.1. Service quality

1.4.1.1 Concept

For a long time, many researchers have tried to define and measure service quality. For example, Lehtinen & Lehtinen (1982) argued that service quality should be assessed on two aspects, (1) the process of service delivery and (2) the outcome of the service. Gronroos (1984) also proposed two components of service quality, which are (1) technical quality, which is what the customer receives and (2) functional quality, which describes how the service is delivered. However, when it comes to service quality, we cannot fail to mention the great contribution of Parasuraman.

Perceived service quality is defined as the result of customers' comparison between their expectations of a service and their perceptions of how the service was delivered. (Parasuraman et al., 2002).

Service quality is the level of perception of service consumption, the overall service of the enterprise brings a chain of benefits and fully satisfies the needs and expectations of customers in production and supply activities and in service distribution at the output, commensurate with the cost that customers have to pay.

In the banking industry, perceived service quality is the customer's perception and evaluation of related products and services in the stages before, during and after the provision. Perceived service quality is divided into two types. First, perceived product quality (tangible) is the customer's evaluation of banking products such as product variety, accompanying utilities, etc., meaning that customers want the core service in the bank's business to truly meet their needs and expect the bank's products or services to be truly valuable compared to the cost they pay. Second, perceived service quality (intangible) is the evaluation of services related to products such as service environment, service staff, support services, after-service customer care policies, technology and distribution channels, etc., meaning that customers expect the communication attitude of bank staff to show friendliness and warmth; get respect, listening, and good after-sales policy from the bank. Both products and services are perceived as important attributes of perceived service quality in DVNHBL.

1.4.1.2 Methods of measuring perceived service quality:

Over the years, many studies have been conducted to measure perceived service quality. One of the most widely used models is SERVQUAL developed by Parasuraman et al. (1988). This model proposes that service quality is measured by five dimensions: reliability, assurance, tangibles, empathy and responsiveness. Reliability refers to an organization's ability to perform the promised service dependably and accurately, ensuring

refers to the knowledge and ability of employees to create trust in customers, tangibles refer to the physical environment, such as facilities, equipment and communication materials; empathy refers to the willingness of employees to pay attention to customers, and finally, responsiveness refers to the willingness of employees to help customers and provide prompt service. Each dimension is measured by 4-5 scales. This model is a useful management tool because it aims to identify the gap between customer expectations and customer perceptions after using the service. SERVQUAL provides a technology for measuring and managing service quality. Many other researchers have used the SERVQUAL dimensions as the basis for their research, and thus SERVQUAL has certainly had a major impact on the business and academic communities (Buttle, 1996, p. 24), and is considered to be "an insightful and useful theoretical framework in service quality management." (Christopher, Payne & Ballantyne, 2002, p. 177).

The SERVPERF model proposed by Cronin and Taylor (1992) measures customer satisfaction. This model inherits the service quality scales of the SERQUAL model, but is more effective because it reduces 50% of the work of SERQUAL because SERVQUAL measures customer perceptions twice. Cronin and Taylor believe that the perception results include expectations in customer evaluation (Q=P). SERVPERF is used more for financial and banking services such as the BANKSERV model of Avkiran (1994) and the 17-factor model of banking services of James G. Barnes Darring and Howlett (1998).

1.4.1.3 The relationship between perceived service quality and loyalty, the hypothesis is:

According to Parasuraman et al (1988); Bitner (1990); Carman (1990), perceived service quality is an antecedent of satisfaction and an important factor influencing customer loyalty.

Several studies have shown that service quality is positively related to customer behavioral intention and loyalty (Zeithaml et al., 1996; Bloemer et al., 1998; and Baker and Crompton, 2000).

Through empirical research, Albert Caruanan (2002) concluded that perceived service quality positively impacts customer loyalty through customer satisfaction.

On this basis, the author puts forward hypothesis 1 in the research model:

H1: Perceived service quality has a positive impact on customer loyalty.

1.4.2. Customer satisfaction

1.4.2.1. Concept

In a highly competitive business environment, customer satisfaction is an important factor for success, because customer satisfaction helps the company retain customers and thus generate profits for the organization (Jamal and Kamal, 2002). Therefore, understanding customer satisfaction remains an important topic for business people.

Customer satisfaction is the state/feeling of the customer towards the service provider after using that service (Terrence Levesque and Gordon HG McDougall, 1996). More specifically, customer satisfaction is the emotional response/overall feeling of the customer towards the service provider based on comparing the difference between what they perceive compared to previous expectations. (Oliver, 1999 and Zineldin, 2000). Fornell (1992) defines satisfaction as an overall assessment based on the total experience of purchasing and consuming products and services performed compared to expectations over time.

Service quality and satisfaction are two different concepts but are closely related in service research (Parasuraman et al., 1988). Satisfaction is a broader concept than perceived service quality because it includes cognitive and affective evaluations while the evaluation of perceived service quality is mainly based on cognitive processes (Oliver, 1997). Previous studies have shown that service quality is the cause of satisfaction (e.g. Cronin & Taylor, 1992).

Although defined in many different ways, customer satisfaction is a four-step process (Mohr, 1982):

(1) expectation, expectation of product quality

(2) implementation and use of products and services

(3) There is no difference between expected and actual usage.

(4) satisfaction.

For banking services, customers will feel satisfied or pleased if the bank responds to their transaction requests quickly, accurately, with a respectful, friendly attitude and good information security (Elizabeth T. Jones, 2005).

1.4.2.2. The relationship between satisfaction and loyalty, hypothesized

The theory suggests:

Previously, many researchers have presented evidence of the relationship between satisfaction and loyalty. Bitner (1990) suggested that satisfaction has a direct impact on loyalty. Furthermore, Rust et al (1993) found a link between satisfaction and loyalty using data from the banking market and from a national hotel chain. Oliver (1980) stated that loyalty has a positive impact on attitude. This positive attitude modifies the attitude toward the product or brand, such as increasing the level of trust, increasing the intention to purchase.

On this basis, the author puts forward hypothesis 2 in the research model:

H2: In retail banking service, satisfaction has a positive impact on customer loyalty

1.4.3. Trust

1.4.3.1. Concept

Trust is the willingness to believe in an exchange partner that we have genuine confidence in them. (Moorman et al., 1992.). It occurs when there is an exchange of reliability and integrity between two parties. (Morgan and Hunt, 1994). Trust is built on the basis of the interactions of partners and trustworthy parties will maintain a long-term relationship (Gefen and Straub, 2003). It is an essential element for

consumers, as it helps them overcome their feelings of risk and uncertainty (McKnight et al., 2002). (McKnight et al., 2002). According to Spekman (1988), a high level of mutual trust must exist to build relationships with strategic partners. Maintaining these relationships is important for businesses as it helps them grow steadily and successfully (Jones et al., 2000).

1.4.3.2. The Relationship Between Trust and Customer Loyalty

Garbarino and Johnson (1999) demonstrated that trust is an antecedent of loyalty. Lin and Wang (2006) demonstrated that trust has a positive impact on loyalty in the mobile e-commerce market. Once customers do not have trust, even if they are satisfied with the supplier's products/services, they will still not be loyal to that supplier.

Loyal customers can become advocates for the bank and its products. Furthermore, loyal customers can become advocates for the bank and its products by providing public opinions and opinions in favor of the bank and its products as well as being information carriers to other customers. Customers become consistent customers of the bank only when they have a basis to believe that the bank will honor its commitments and provide products and services that meet their needs over time. And loyalty is positively influenced by trust. (Abdul Naveed Tariq and Nadia Moussaoui, 2009).

On this basis, the author puts forward hypothesis 3 in the research model:

H3: In retail banking, trust has a positive impact on customer loyalty.

1.4.4. Bank image

1.4.4.1. Concept

Bank image is the connection between customers' memories and the overall image of the Bank (Keller and Aaker, 1992). When the bank image has left an impression in the customers' memory, it indirectly affects their purchasing decisions through good feelings about the brand. Therefore, bank image is an important tool to create differentiation from competitors (Slongo and Vieira, 2007). Thus, bank image is formed by the experience of purchasing and consuming goods and services over a long period of time. (Weiwei, 2007).

1.4.4.2. The relationship between Bank Image and Customer Loyalty and the hypothesis:

The impression of a good image of the bank will help customers easily choose the brand when buying, encouraging customers to continue using goods and services in the future. Andreassen and Lindestand (1998) concluded that a good, friendly image will help increase customer loyalty.

On this basis, the author puts forward hypothesis 4 in the research model:

H4: In retail banking, bank image has a positive impact on customer loyalty.

1.5. Proposed research model

1.5.1 Argument for the proposed research model:

From referring to studies that have been conducted in Vietnam and around the world on customer loyalty in different fields and industries, the author finds that the customer loyalty model in the Research Paper Main Premise of Customer Loyalty in Moroccan Banks, International Journal of Management and Business Science is relatively suitable for application to a bank in Vietnam.

The model mentioned above has conducted research on a fairly large scale of 4 major cities in Morocco and the data used is nearly 500 samples. The research is carried out on a large scale of 4 major cities in Morocco and the data used is nearly 500 samples.

The research is currently specialized in the Banking sector, so the factors affecting customer loyalty are specific to the industry. In addition, the research article was published in the International Journal of Management and Business Science, a relatively prestigious journal in the business sector and is archived and referenced by prestigious websites in the world such as Emerald and ProQuest.

The application of the above model certainly requires adjustments to suit the cultural environment and economic conditions in Vietnam. Because the study of Service Quality as a mediating factor affecting Customer Loyalty through Satisfaction is relatively complicated with running the regression model twice, the author proposes to only consider Service Quality as one of the factors directly affecting Loyalty.

After adjusting to suit the Vietnamese market, the proposed model is shown as follows:

Perceived service quality

satisfaction

Customer loyalty

Trust

Bank image

Figure 2.6: Proposed research model

1.5.2 Summary of hypotheses in the research model

H1: In retail banking, perceived service quality has a positive impact on customer loyalty.

H2: In retail banking services, satisfaction has a positive impact on customer loyalty.

H3: In retail banking, customer trust has a positive impact on customer loyalty.