Chapter 3

COMPETITIVENESS OF VIETCOMBANK

3.1. OVERVIEW OF THE FORMATION AND DEVELOPMENT PROCESS OF VIETCOMBANK

* History of formation and development of Vietcombank

Formed from the predecessor organization, the State Bank of Vietnam's Foreign Exchange Department, Vietcombank has always maintained its role as a key bank in the banking system in Vietnam. Vietcombank has gradually escaped the subsidy mindset, removed institutional barriers to access and integrate with the world financial and monetary market; performed well the role of guarantee and export support for domestic enterprises, participated in financing many key national projects, implemented the State Bank's monetary policy, contributed to stabilizing the currency, curbing inflation, managing exchange rates and increasing national foreign exchange reserves.

In the period 2000 - 2005, Vietcombank successfully built and implemented a restructuring plan focusing on improving financial capacity, risk management, technological innovation, introducing many new banking utilities to serve customers and being ready for the integration process. Thanks to its proactiveness, creativity and forward-looking vision, Vietcombank is proud to be the leading bank in the commercial banking sector in completely handling bad debts, improving capital safety ratios, completing phase 2 of the banking and payment system modernization project. On the basis of modern technology, Vietcombank has gradually provided the market with high-quality products and services such as Vietcombank online & connect 24, Vietcombank Money, I-Banking, Home Banking, SMS Banking, Vietcombank Cyber Bill Payment, Vietcombank Global Trade, ..., creating an important premise for building an electronic payment platform in Vietnam, gradually replacing "cash culture" with "card civilization and modern payment services".

In 2007, Vietcombank became a pioneer in the banking industry in implementing the policy of equitizing state-owned enterprises. With the close guidance of the Government, the State Bank, the Ministry of Finance and related ministries and branches, Vietcombank successfully carried out its initial public offering on December 26, 2007. With the advantages after converting to a joint stock form in 2008, Vietcombank had the conditions to improve its financial capacity, manage the bank more effectively and transparently, enhance its competitive position, and at the same time have more opportunities to play a key role in providing banking services and maintain a large dominant market share. Not only has Vietcombank made great strides in its financial capacity, it has also created an important turning point in its transformation and growth process by signing a strategic shareholder contract with Mizuho Corporate Bank, a member of Mizuho Financial Group - the third largest financial group in Japan in September 2011.

In the period of 2013-2015, contributing to the implementation of the general political task of the banking sector - restructuring credit institutions (CIs) and handling bad debts, Vietcombank has proactively developed and actively implemented the restructuring and handling bad debts project to improve management capacity, safety and operational efficiency. Vietcombank's restructuring process has achieved important results, creating changes, creating new positions and strengths for Vietcombank's sustainable development.

In addition to the achievements in recent years, with the impacts of the domestic and foreign macro environment, Vietcombank also faces many difficulties and challenges: fierce competition from domestic and foreign banks, Vietcombank's market share in some fields tends to narrow, the operating efficiency of some business segments is not high, some of Vietcombank's competitive advantages are gradually being lost.

Implement the Government and the State Bank's policy of restructuring credit institutions in the 2016-2020 period while continuing to strengthen internal strength and maintain position.

By 2025, Vietcombank has established the goal of striving to become one of the 100 largest banks in Asia, one of the 300 largest financial banking groups in the world, managed according to the best international practices.

* Organizational chart and functions

In the early stages of formation and development, Vietcombank's organizational model simply included the functions of a traditional commercial bank with the main functions and tasks of lending, capital mobilization and payment. During this period, the products that Vietcombank provided to customers still had many limitations such as diversity, modernity and convenience.

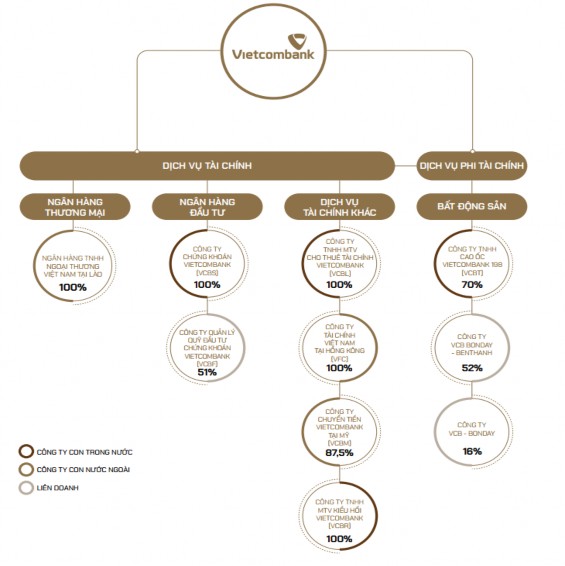

Vietcombank's ecosystem with the core of Vietnam Joint Stock Commercial Bank for Foreign Trade plays the key and most important role. Vietcombank acts as the parent bank/parent company contributing capital to establish subsidiary banks or member companies. Currently, Vietcombank has 1 subsidiary bank and 9 subsidiaries and associated companies. Vietcombank's subsidiary bank is Vietnam Foreign Trade Bank Limited in Laos, established in 2018. In addition, Vietcombank also has 9 subsidiaries and associated companies with functions such as securities, fund management, real estate, financial leasing, money transfer, remittance, etc. Vietcombank is one of the few commercial banks in Vietnam with many satellite companies serving business activities.

Since its transformation to a joint stock model in 2008, Vietcombank has begun to shift its business orientation and organizational model towards a modern bank. Vietcombank's organizational model is similar to modern financial corporations in the world, with a diverse ecosystem of products and customers. In particular, the functions and tasks of the members in the ecosystem are clearly differentiated and related to and complement each other. The ecosystem in Vietcombank's organizational model is as follows:

Diagram 3.1. Organizational structure and functions and tasks

Source: Vietcombank

Similar to the ecosystems of large, modern financial corporations, Vietcombank's organizational model aims at the following points:

- Expand core business activities through expanding the geographical scope of business activities to find new customer files, expanding profit scale

- In parallel with the search for new customers through expanding the geographical scope of operations, Vietcombank also aims to exploit and serve customers in depth. Products of Vietcombank and its subsidiaries

The company aims to provide comprehensive financial products for customers, aiming at comprehensive service and customer retention.

Thus, Vietcombank has transformed its business organization model, aiming at a comprehensive multi-functional ecosystem, aiming to provide comprehensive products to customers.

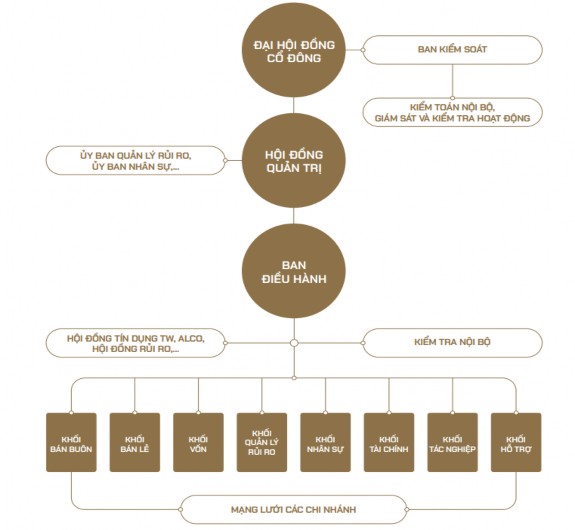

In addition to the organizational model of operation in the overall ecosystem mentioned above, Vietcombank also clearly differentiates in its business management organization model. Vietcombank's organizational management model is divided through the operating model of a commercial bank and the operating model of a limited liability/joint stock company.

For the model of commercial banks, Vietcombank is divided into the following management levels:

- The General Meeting of Shareholders is the top body, which has the highest authority to decide on all matters of Vietcombank. The largest shareholder in the General Meeting of Shareholders of Vietcombank is the State Bank of Vietnam. The General Meeting of Shareholders sets out the operating regulations and decides on important matters of Vietcombank.

- The Board of Directors is the body with authority behind the General Meeting of Shareholders, with the function of issuing specific regulations and rules according to the regulations approved by the General Meeting of Shareholders. At the same time, the Board of Directors also has the function of managing the general operations of the bank.

- The Executive Board consists of the General Director and Deputy General Directors. This is the department that directly manages the bank's business activities, through the functional departments at the Head Office.

- The business blocks at the headquarters include the wholesale block, retail block, capital block, risk management block, personnel block, finance block, operations block and support block. These blocks do not directly participate in business activities but play an indirect management and support role. These blocks are divided based on their own functions and tasks. Within the blocks, they are divided into departments to specify and detail the functions of each department.

- The business sector includes a network of branches distributed throughout the provinces and cities of the country. At the branches, the departments will be divided into departments at the branch headquarters and transaction offices. This division is based on scale, geographical location and business strategies. The branch director will be the person who manages and operates all activities of the branch.

Diagram 3.2. Ecosystem in Vietcombank's organizational model

Source: Vietcombank

Vietcombank's organizational model is also divided into vertical management, according to customer groups (wholesale, retail, ....), according to the operations of departments (accounting, human resources, support, ...) to create consistency in the system and minimize operational risks.

3.2. COMPETITIVENESS OF VIETCOMBANK ACCORDING TO CRITERIA

3.2.1. Criteria for assessing Vietcombank's competitiveness compared to domestic and foreign credit institutions from 2010 to 2020 from a financial perspective

* Evaluation of Vietcombank's achievements in 10 years of continuous development from 2010 - 2020

In the 10 consecutive years from 2010 to 2020, Vietcombank's development and expansion process has undergone many major changes. The most impressive period is from 2017 to present, when Vietcombank has continuously led in profit scale in the system of commercial banks in Vietnam for 4 consecutive years. Vietcombank's profit scale has reached about 1 billion USD in the last 2 consecutive years. Notably, Vietcombank's profit scale has made a strong breakthrough and created a large gap compared to the commercial banks behind Vietcombank.

Looking back at 10 years of development, the main results that Vietcombank has achieved based on quantitative indicators are as follows:

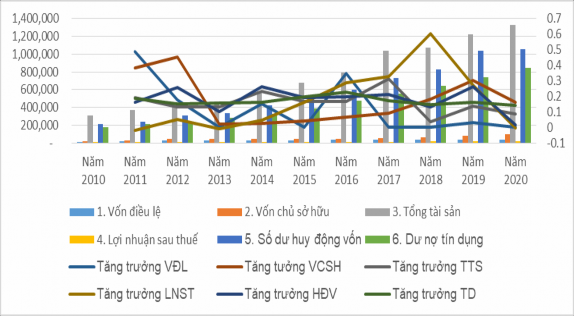

Table 3.1. Main results achieved by Vietcombank based on quantitative indicators for the period 2010 - 2020

Unit: billion VND

Year 2010 | Year 2011 | Year 2012 | Year 2013 | Year 2014 | Year 2015 | Year 2016 | Year 2017 | Year 2018 | Year 2019 | Year 2020 | |

1. Charter capital | 13,224 | 19,698 | 23,174 | 23,174 | 26,650 | 26,650 | 35,978 | 35,978 | 35,978 | 37,089 | 37,089 |

2. Equity | 20,737 | 28,639 | 41,547 | 42,386 | 43,473 | 45,172 | 48,146 | 52,558 | 62,179 | 80,954 | 94,095 |

3. Total assets | 307,621 | 366,722 | 414,488 | 468,994 | 576,996 | 674,395 | 787,907 | 1,035,293 | 1,074,027 | 1,222,814 | 1,326,230 |

4. LN ST | 4,303 | 4,217 | 4,427 | 4,378 | 4,586 | 5,332 | 6,851 | 9,111 | 14,622 | 18,597 | 18,473 |

5. Capital raising | 208,320 | 241,700 | 303,942 | 334,259 | 422,204 | 503,007 | 600,738 | 726,734 | 823,390 | 1,039,086 | 1,053,354 |

6. Credit | 176,814 | 209,418 | 241,163 | 278,357 | 323,332 | 387,152 | 475,887 | 557,688 | 639,370 | 741,387 | 845,128 |

Capital Growth | 49.0% | 17.6% | 0.0% | 15.0% | 0.0% | 35.0% | 0.0% | 0.0% | 3.1% | 0.0% | |

VCSH growth | 38.1% | 45.1% | 2.0% | 2.6% | 3.9% | 6.6% | 9.2% | 18.3% | 30.2% | 16.2% | |

TTS Growth | 19.2% | 13.0% | 13.2% | 23.0% | 16.9% | 16.8% | 31.4% | 3.7% | 13.9% | 8.5% | |

Net profit growth | -2.0% | 5.0% | -1.1% | 4.8% | 16.3% | 28.5% | 33.0% | 60.5% | 27.2% | -0.7% | |

Growth of HDV | 16.0% | 25.8% | 10.0% | 26.3% | 19.1% | 19.4% | 21.0% | 13.3% | 26.2% | 1.4% | |

TD Growth | 18.4% | 15.2% | 15.4% | 16.2% | 19.7% | 22.9% | 17.2% | 14.6% | 16.0% | 14.0% |

Maybe you are interested!

-

Overview of the History of Formation and Development of Vietnam Joint Stock Commercial Bank for Foreign Trade

Overview of the History of Formation and Development of Vietnam Joint Stock Commercial Bank for Foreign Trade -

The Formation and Development Process of Vietnam Development and Investment Bank

The Formation and Development Process of Vietnam Development and Investment Bank -

History of Formation and Development of Vietnam Joint Stock Commercial Bank for Industry and Trade

History of Formation and Development of Vietnam Joint Stock Commercial Bank for Industry and Trade -

Overview of Joint Stock Commercial Bank for Investment and Development of Vietnam

Overview of Joint Stock Commercial Bank for Investment and Development of Vietnam -

Overview of the Formation and Development Process of Vietnam Tourism

Overview of the Formation and Development Process of Vietnam Tourism

Source: Vietcombank.

Chart 3.1. Main results achieved by Vietcombank based on quantitative indicators for the period 2010 - 2020

Source: Vietcombank

There are many criteria for evaluating the scale of a commercial bank, including 6 main indicators: Charter capital, equity, total assets, profit after tax, capital mobilization balance and credit balance. In general, in the 10 consecutive years from 2010 to present, Vietcombank's main indicators have all grown. On average, the above indicators have increased from 2.8 times to 5.1 times after 10 years of development.

Specifically, Vietcombank's total assets in 2010 reached VND 307,621 billion, increasing to VND 1,326,230 billion in 2020, equivalent to an increase of 4.3 times. Owner's equity in 2010 reached VND 20,737 billion, increasing to VND 94,095 billion in 2020, equivalent to an increase of 4.5 times. Profit after tax in 2020 reached VND 18,473 billion compared to 2010, reaching VND 4,303 billion, an increase of 429%. If considering the average growth rate in 10 years, Vietcombank's total assets, owner's equity and profit after tax have an average growth rate/year of 16%/year, 17%/year and 17%/year, respectively.

Credit and capital mobilization indicators also have growth rates.