Mobilization increased over the years, ensuring capital to meet customers' loan needs.

2.1.3.2. Capital use activities

In the credit activities of commercial banks, credit lending is the main and most important activity, bringing a lot of profit to the bank. Therefore, BIDV Trang An always pays attention and focuses on expanding credit lending activities at the branch. In order to expand customer relations and promote credit activities, the staff at the branch has proactively sought potential customers, projects, and feasible production and business plans, creating conditions to promptly support the capital needs for business activities of enterprises.

In addition, the bank also always pays attention to maintaining and strengthening the traditional customer base. The transaction style of credit officers and the quality of credit products of the branch have created trust and prestige for customers, creating favorable conditions for customers to do business effectively. BIDV Trang An has achieved some of the following encouraging results:

1000

900

800

700

600

500

400

300

200

100

0

949

30%

834

25%

25%

22%

689

21%

20%

551

453

14%

15%

10%

5%

0%

2016

2017

2018

2019

2020

Total outstanding debt

Capital mobilization growth rate

Figure 2.3. Outstanding debt situation of BIDV Trang An in the period 2016 - 2020

(Source: BIDV Trang An's Business Results Report over the years 2016-2020)

Over the 5 years from 2016 to 2020, the bank's annual outstanding loans increased from VND 453 billion to VND 949 billion. In 2017, outstanding loans reached VND 551 billion, an increase of VND 98 billion compared to 2016 with an increase of 21.63%. By 2018, the growth rate

Outstanding loan growth reached 25.04%, corresponding to an increase of VND 138 billion, total outstanding credit at VND 689 billion. In 2019, total outstanding loan was VND 834 billion, an increase of VND 145 billion compared to 2018, outstanding loan growth rate reached 21.05% compared to 2018. In 2020, outstanding loan increased by VND 115 billion, total outstanding loan reached VND 949 billion, growth rate 13.79%. This is the lowest growth rate in the period 2016-2020.

The branch's outstanding debt structure by customer type is as follows:

Table 2.2: Loans at BIDV Trang An in the period 2016-2020

Unit: Billion VND

Target

2016 | 2017 | 2018 | 2019 | 2020 | ||||||

Value | Proportion (%) | Value | Proportion (%) | Value | Proportion (%) | Value | Proportion (%) | Value | Proportion (%) | |

TCKT customers | 270 | 59.60 | 348 | 63.16 | 405 | 58.78 | 463 | 55.52 | 489 | 51.53 |

Individual customers | 183 | 40.40 | 203 | 26.84 | 284 | 41.22 | 371 | 44.48 | 460 | 48.47 |

Total outstanding debt | 453 | 100 | 551 | 100 | 689 | 100 | 834 | 100 | 949 | 100 |

Maybe you are interested!

-

Credit risk at Bank for Investment and Development of Vietnam: Current situation and preventive solutions - 11

Credit risk at Bank for Investment and Development of Vietnam: Current situation and preventive solutions - 11 -

Credit risk management at Joint Stock Commercial Bank for Investment and Development of Vietnam - Trang An Branch - 14

Credit risk management at Joint Stock Commercial Bank for Investment and Development of Vietnam - Trang An Branch - 14 -

Analysis of Credit Situation and Credit Risk Management of Vietnam Bank for Agriculture and Rural Development, Vinh Thuan Branch - Kien Giang

Analysis of Credit Situation and Credit Risk Management of Vietnam Bank for Agriculture and Rural Development, Vinh Thuan Branch - Kien Giang -

Credit risk management at the branch of the Bank for Agriculture and Rural Development of Kon Tum province - current situation and solutions - 2

Credit risk management at the branch of the Bank for Agriculture and Rural Development of Kon Tum province - current situation and solutions - 2 -

Basic Issues of Credit, Credit Risk and Bad Debt of Commercial Banks

Basic Issues of Credit, Credit Risk and Bad Debt of Commercial Banks

(Source: BIDV Trang An's Business Results Report over the years 2016-2020)

Lending to economic organizations accounts for the majority of the branch's total outstanding loans, but the proportion has been decreasing over the years from 59.60% to 51.53%. Along with that is the increase in the proportion of loans to individuals and businesses, which is consistent with the development trend of BIDV and the banking industry in general.

In the years 2016-2020, implementing the policy of preventing economic recession with many solutions of the government, the State Bank and BIDV, the branch has focused capital on five priority areas, continuing to implement measures to remove difficulties for production and business activities in the branch's operating area.

The branch has also carried out a comprehensive transformation of the model and organizational structure under the direction of BIDV, perfecting the organization and personnel for the departments, thereby implementing vertical management for each segment of individual and corporate customers to deeply specialize, improve productivity, and efficiency in human resource use while ensuring that all business activities are always customer-oriented, meeting and satisfying all financial needs of each customer segment, which is the basis and premise for the growth process.

2.1.3.3. Business results of Vietnam Joint Stock Commercial Bank for Investment and Development - Trang An branch

For any business when participating in business activities, profit is the goal they pursue, but the profit that the business earns must be based on safety and reputation. BIDV Trang An in particular and all banks in general, business activities are mainly based on currency, this is a sensitive factor, affected by many different factors but its ultimate goal is not outside the goal of profit.

The bank's business results are considered an important factor determining the existence and development of the bank. Over the years, with the efforts and endeavors in management and operation to maximize its advantages, BIDV Trang An has achieved certain results in business activities, constantly improving its competitiveness to increasingly affirm its position and image in the market.

Thanks to appropriate business policies, the branch's operations in the last five years have developed at a high speed: market share has been expanded, income has been increased. The following table shows the business results of BIDV Trang An branch in the last five years:

Table 2.3: Business results of BIDV Trang An from 2016-2020

Unit: Billion VND

Target

2016 | 2017 | 2018 | 2019 | 2020 | |

Total revenue | 74 | 130.6 | 216.5 | 277.1 | 348.8 |

Total cost | 60.2 | 113.5 | 200.7 | 260.6 | 329.1 |

Profit before risk provision | 13.8 | 17.1 | 19.7 | 21.9 | 26.5 |

RRTD reserve | 1.1 | 2.8 | 3.9 | 5.4 | 6.8 |

Profit before tax | 12.7 | 14.3 | 15.8 | 16.5 | 19.7 |

Pre-tax profit growth rate | 12.60% | 10.49% | 4.43% | 19.39% |

(Source: BIDV Trang An's Business Results Report over the years 2016-2020)

Through the above data table, we can see that the business performance of BIDV Trang An branch is positive in the 5 years 2016-2020. The profit of the following year is higher than the previous year, that result is clearly shown through the total revenue and total cost situation.

Regarding revenue situation: In general, the branch's revenue has increased over the years. In 2016, the total revenue was 74 billion VND. After 5 years, this figure has reached 348.8 billion VND in 2020. This increase in income is due to the branch's increased encouragement for customers to borrow capital, which has brought in a very high income from loan interest, pushing the branch's income up. In addition, it can be seen that revenue from credit activities is still the main source of revenue for the branch with a proportion of approximately 90%. In addition, non-interest income services such as revenue from services, foreign exchange trading revenue and other revenue have also increased steadily over the years.

Regarding expenses: as well as income, the most money that banks have to spend is on deposit mobilization activities, interest payments always account for a high proportion of total expenses because in order for the bank's mobilized capital to ensure the increasing demand for loans, the bank has promoted the mobilization of capital from residents, economic organizations, and credit institutions. Total expenses in 2016 reached 60.2

billion VND and by 2020 it will be 329.1 billion VND. The branch's expenses are too large, reducing the branch's profits, leading to difficulties in developing and expanding its scale. The branch needs to manage its business activities well and tighten controls to minimize operating costs.

The bank's pre-tax profit increased in value during the period 2016 - 2020. However, the profit growth rate fluctuated strongly in the past 5 years. In 2017 and 2018, the pre-tax profit growth rate was stable at over 10%. However, the increase in bad debt in 2019 greatly affected the branch's profit and its business activities. Pre-tax profit in 2019 reached VND 16.5 billion, an increase of 4.43% compared to 2018, equivalent to VND 0.7 billion.

In 2020, pre-tax profit has recovered strongly, pre-tax profit in 2018 reached 19.7 billion VND, an increase of 3.2 billion VND compared to 2019, corresponding to a growth rate of 19.39%. Although there was a decrease in profit growth rate in 2019, the profit value still increased steadily every year. This is considered a positive sign for BIDV Trang An branch. The branch needs to continue to promote the credit lending process, increase revenue. Closely monitor costs to minimize unnecessary costs.

2.2. Current status of credit activities at Vietnam Joint Stock Commercial Bank for Investment and Development - Trang An branch

2.2.1 Credit methods at Vietnam Joint Stock Commercial Bank for Investment and Development - Trang An branch

BIDV Trang An provides full range of main credit methods including: One-time loans, installment loans, Overdraft loans, Credit limit loans.

Types of credit products at BIDV Trang An:

BIDV Trang An provides a variety of credit products for customers. At BIDV Trang An, there are full credit products, including: Real estate loans; Consumer loans; Production and business loans; Agricultural loans; Loans secured by savings books and valuable papers.

However, for each credit product, BIDV Trang An designs many smaller products to suit each customer segment.

In consumer lending, BIDV Trang An has designed products such as Personal Loans, Loans for Employees, etc. The advantage of this product is that each credit product package has different characteristics, suitable for the characteristics of each customer to meet the maximum needs of customers. However, the disadvantage is that BIDV Trang An will have to manage more loan products than DTCT, consulting and introducing to customers will be difficult, because the staff introduces too many products, making it difficult for customers to choose.

BIDV Trang An's valuable paper mortgage loan product has the advantage of a very fast loan approval time. For valuable papers issued by BIDV Trang An: the maximum time from receiving the customer's complete application to disbursement is 1 hour. For valuable papers issued by other organizations: the maximum time from receiving the customer's complete application and confirmation of the blocking by the issuing organization to disbursement is 2 hours. However, this product is only suitable for customers with collateral.

The loan product for buying social/commercial housing has a loan value of up to 90% of the purchase/lease/hire-purchase value according to the contract/invoice, long loan repayment period, up to 15 years, the most preferential interest rate on the market: 5%/year. However, this product only applies to cadres, civil servants, public employees, armed forces or workers with a monthly income of 9 million VND/month or less.

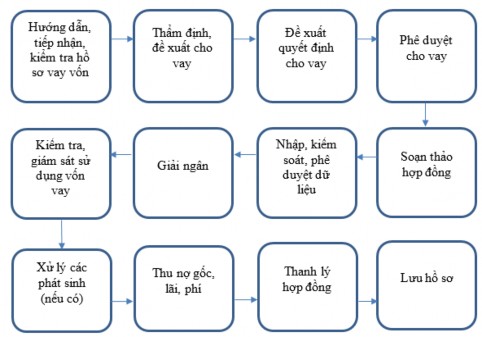

2.2.2. Credit process at Vietnam Joint Stock Commercial Bank for Investment and Development

- Trang An branch

after:

BIDV Trang An's credit operation process includes 12 steps, specifically as follows:

Figure 2.4. Credit operation process at BIDV Trang An

(Source: Internal guidance document at BIDV Trang An)

Step 1: Guide, receive, and check loan application: Customer service staff receives customer requests. Checks the completeness, reasonableness, and legality of the documents provided by the customer, and transfers all documents provided by the customer to the risk management department.

Step 2: Appraisal, loan proposal, appraisal of collateral (if the loan is secured by assets): Customer department staff collects information about the customer and the loan usage plan, appraises customer qualifications, classifies customers, prepares a report proposing approval or disapproval of the loan and submits it to the customer department leader.

Step 3: Appraisal and proposal for loan decision: Risk management department staff re-appraises the content that has been appraised by the customer department based on the proposal report.

Step 4: Approve loan for customers: Branch/Headquarter leaders review the customer department's proposal report, risk management department's appraisal report, and related documents. If the loan is approved, notify relevant departments to carry out the next steps.

Step 5: Drafting credit contracts, guarantee contracts, notarization and registration of secured transactions (if any): Customer service staff coordinates with the guarantor to carry out procedures for notarization, authentication and registration of secured transactions. Transfer the contract to relevant departments for disbursement.

Step 6: Enter, control, approve data about customers, collateral and loans, import collateral records: Customer department staff enter customer records, collateral and loan information into the system.

Step 7: Disbursement: Customer service staff receives and checks disbursement documents, submits them to the competent authority for approval. Creates a loan account on the system, and transfers it to the leader for approval. Then transfers the disbursement documents to the accounting department to make disbursement to the customer.

Step 8: Check and monitor loan usage: The customer department prepares the information that needs to be checked for each specific customer. Meet, contact, exchange information with customers and prepare a loan usage check report, transfer it to relevant departments for re-evaluation and approval.

Step 9: Handle any issues (if any) Step 10: Collect principal, interest, and fees

Step 11: Liquidate the Credit Contract, Guarantee Contract, and release the collateral (if any)

Step 12: Save the file

In this lending process, BIDV Trang An has two pre-lending appraisal steps (1 is appraisal at the customer's department and 2 is appraisal at the risk management department) to minimize credit risks that may arise. At the same time, BIDV Trang An also keeps records after lending to have a basis for credit approval for customers in subsequent credit contracts.