In order to implement Vietnam's commitments to international financial and monetary organizations, proactively integrate the activities of the Vietnamese banking system with those of countries in the region and the world, and contribute to promoting the development of the monetary market in our country, the requirement to improve the financial situation of the banking system is being raised very urgently and urgently. If the restructuring program of the commercial banking system is properly and effectively implemented, it will create a premise to contribute to the development of the monetary market.

For State-owned commercial banks, the Government has approved the Project to consolidate and restructure the system with the following basic contents: Strengthening the organization of banks on the basis of debt restructuring and applying measures to prevent the emergence of new bad debts; increasing the charter capital of State-owned commercial banks; clearly separating the business functions of commercial banks from lending according to State policies through the establishment of policy banks, creating conditions for State-owned commercial banks to truly operate according to market principles. Each bank restructures its organizational apparatus, modernizes banking technology as well as management capacity, improves the qualifications and quality of its staff to suit its operational requirements, taking into account the current trend of international integration.

For joint stock commercial banks, the work of rectification and consolidation, although complicated, is still being directed and implemented in accordance with the spirit of the project approved by the Government. Weakly operating banks with no potential for development have been and are being dissolved or merged with other banks. The main motto is to build a strong, safe joint stock commercial bank system with a worthy position in the economy, in line with the general trend of the region and the world.

3.2.1.3. Improving the financial capacity and capital management of Vietnamese commercial banks

Capital management and operation must have market characteristics, while ensuring concentration. From there, improve the quality of available capital management, in order to help commercial banks proactively and flexibly participate in activities in the money market, especially overcoming the high seasonality of the money market. The improvement of the management capacity of State-owned credit institutions after equitization will be implemented most quickly and effectively through the cooperation and assistance of foreign partners. Complete the internal organizational and administrative apparatus; carry out inspection, examination and regular reporting.

According to the commitments, when joining the WTO, the banking sector will be gradually opened according to a 7-year roadmap. Since 2006, Vietnam has had to remove restrictions on foreign financial institutions and banks investing in Vietnam. This will be a great pressure on the domestic banking system, forcing banks to accelerate the implementation of plans to improve their competitiveness so that banks can face the challenges of survival.

In recent times, the world has witnessed many financial scandals of large banks such as Citi Bank of the US and NAB of Australia. The main reason is the financial capacity of the banks. This shows that when banks have strong financial capacity, they can ensure stable business operations, thereby the economy will also grow steadily.

The most important financial factor of a commercial bank is capital, including: Legal capital and Reserve fund. Bank capital is the basic condition to ensure customer deposits, once there is a risk in business ( such as bad debt, loss in securities business, then the bank's capital is the amount to compensate for that risk and create the ability to pay customer debts ).

Legal capital is the bank's own capital contributed by the owners. If it is a state-owned bank, the capital owner is the State; if it is a joint-stock bank, it is contributed by the shareholders. The legal capital of a bank is stated in the bank's operating license and charter, it must be greater than the minimum level prescribed by the State.

Reserve funds include:

Reserve fund : is capital taken from annual profits to supplement legal capital. Vietnamese law stipulates that 5% of net profits must be calculated annually to establish this fund, and the maximum level is determined by the Central Bank.

Special reserve fund : is also a type of capital calculated from profits to compensate for risks during operations. Every year, the bank must set aside 10% of net profits until it reaches the legal capital.

In addition, the bank also has undistributed profits to shareholders or other special funds that have not been used.

Since the 1930s, economists have proposed a "rule of thumb" which is the 10% rule of bank capital compared to assets. In addition, people have also proposed a ratio between bank capital compared to risky assets ( Assets minus treasury bills and bonds ). In practice, the 10% rule is rarely implemented by banks.

But the determination of the relationship between bank capital and assets is of interest to bank managers and this ratio is considered part of management policy. In 1985, the US Federal Reserve System set this ratio at 6% for large banks (previously only 3%).

Many countries have regulated the relationship between bank capital and the amount of money mobilized as follows: Banks are not allowed to mobilize more than 20 times the capital. Although capital is the basic factor to evaluate the financial aspect of a bank, in addition to capital, we need to take into account a series of other factors such as: bank liquidity, asset risk structure, volatility of deposits and quality of bank management.

According to the US and some Western countries, to evaluate a bank, people use 5 criteria:

Target

Note | |

Capital ratio | Capital ratios (VSCH/ ∑ TS, VCSH/Assets …) |

Asset quality has | Credit quality and investments |

Quality of management | Management team, staff, network, technology… |

Interest | Income Ratios |

Liquidity | Liquidity on assets, on shares |

Maybe you are interested!

-

Impact of Financial Market Development on Enterprise Capital Structure by National Institutional Quality

Impact of Financial Market Development on Enterprise Capital Structure by National Institutional Quality -

The impact of financial market development on the capital structure of listed enterprises in the ASEAN Economic Community - 28

The impact of financial market development on the capital structure of listed enterprises in the ASEAN Economic Community - 28 -

The impact of financial market development on the capital structure of listed enterprises in the ASEAN Economic Community - 2

The impact of financial market development on the capital structure of listed enterprises in the ASEAN Economic Community - 2 -

The impact of financial market development on the capital structure of listed enterprises in the ASEAN Economic Community - 21

The impact of financial market development on the capital structure of listed enterprises in the ASEAN Economic Community - 21 -

Improving Financial Capacity and Credit Operation Efficiency of Commercial Banks in the Southeast Region

Improving Financial Capacity and Credit Operation Efficiency of Commercial Banks in the Southeast Region

Banking agencies base on the above to score and classify banks as good, fair, weak...

For assets

In asset management, on the one hand, commercial banks must respect required reserve ratios , on the other hand, they must avoid risks in order to survive and do profitable business.

In a market economy, banks operate in an environment of risk and uncertainty, and future interest rates and securities prices are unpredictable. Therefore, bank managers must look beyond mere profit motives.

To maintain solvency, on the one hand, commercial banks must ensure that the total value of assets is greater than the payable liabilities at all times.

Points. If the loan capital business is not recoverable and there are losses in securities operations, the value of assets will fall below the liabilities and thus lead to the bank's insolvency, possibly having to close or sell assets to another bank. However, if we consider the amount of assets that are sufficient to cover the liabilities, it is not enough to say the bank's ability to pay, but we must also consider liquidity, that is, assets that can be converted into cash immediately with a sufficient amount to meet the demand for cash withdrawals, the shortfall in clearing payments or legitimate borrowing needs of related banks, while still maintaining the legal reserve ratio. Thus, there may be a case where a bank has enough ability to pay off debts but lacks liquidity to cover immediate debts, which is considered a lack of ability to pay and is at risk of bankruptcy.

In order to stand firm and compete in business, banks must keep risks within certain limits, must ensure liquidity at the necessary level in the asset structure and acceptable profitability. If too much attention is paid to this or that factor, it will negatively affect business results. Suppose a bank accepts high risks and low liquidity to expand profitable operations, it will risk insolvency. On the contrary, if it is cautious about risks and increases liquidity too much, it will lead to reduced profits and, more dangerously, it will make customers stay away, lose trust, and go elsewhere. All of these things directly affect the financial results of the bank.

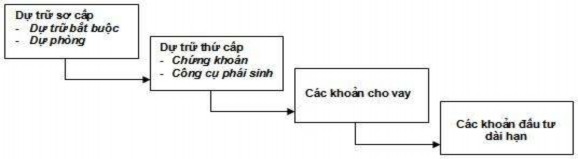

In asset structure management, banks often calculate and prioritize as follows:

Primary reserves are items of cash funds, deposits at the Central Bank , and deposits at other banks. These reserves are used to reserve

reserves as prescribed by the Central Bank and to meet unusual cash needs of customers or to make payments to other banks in inter-bank payments.

Secondary reserves include securities that can be easily converted into cash such as treasury bonds, bank acceptances, etc. Secondary reserves are used to support primary reserves for anticipated withdrawals, payments between banks, and customer borrowing.

Secondary reserves have met the anticipated seasonal and cyclical needs. For example, banks operating in rural areas have a large demand for credit during the harvest season and a sharp decrease after the harvest season. After the harvest season, the demand for cash to buy rice is very large. Banks operating in urban areas have a strong demand for reserve goods before Tet. As for the public, during the holidays, they need to withdraw money to spend. In addition, secondary reserves are also used to meet cyclical needs such as during periods of economic growth, when business is prosperous, the demand for credit increases, and conversely, during periods of recession, credit shrinks.

In addition to meeting seasonal and cyclical needs, secondary reserves are also an important additional source to handle sudden withdrawals and large payments that banks cannot anticipate.

After fully implementing primary and secondary reserves, banks prioritize safe profitable operations such as government bonds and short-term credit.

In the credit and long-term investment business, banks must be cautious and must take into account the capital resources. If the proportion of long-term capital sources is low while the proportion of credit and credit investment is high, the level of risk will increase. Therefore, it is necessary to calculate a reasonable ratio between lending and long-term investment in relation to the items considered according to the term of the debt assets.

For debt assets

Traditionally, banks have viewed the liabilities side of the balance sheet as a natural business that does not require management and control, but rather requires appropriate use of what is available, that is, asset management. However, today, bankers have begun to pay more attention to liabilities and consider asset management as a

liabilities as a factor to improve management efficiency, as well as increase additional sources for the bank's solvency.

Liability management is the use of the liability side of the balance sheet to expand funds to meet liquidity needs such as replenishing reserves or regulating new credit needs. Thus, liability management is the rapid mobilization of money in the market to create liquidity for the bank.

In developed countries, debt management is done through the purchase and sale of certificates of deposit, sources from central banks and other sources.

Liability management techniques aim to exploit important additional sources of bank liquidity. However, this management is only supplementary, not a substitute for asset management. If too much attention is paid to exploiting additional sources and neglecting asset reserves, it will have negative consequences for bank operations, possibly leading to a serious crisis.

3.2.1.4. Improve credit quality, ensure stable operation of the credit market

The current outstanding problem is that there is still a part of low-quality credit, which is really threatening the stability of the monetary market. Overdue debt has decreased but is still at a high level. First of all, there must be measures to ensure the improvement of the quality of credit activities. For example, to limit credit risks, it is necessary to have a reasonable credit policy, screen and monitor borrowers, establish long-term customer relationships, regulate credit limits, mortgage assets, reserve funds for risks, etc.

Credit growth rate must be consistent with actual mobilized capital growth, credit targets set at the beginning of the year and the ability to control credit quality. At the same time, it is necessary to ensure available capital for payment needs and safe business operations.

Credit institutions must strengthen control over lending to housing business projects, urban and industrial park infrastructure construction projects, ensuring appropriate ratios of outstanding loans for these projects, as well as loans with real estate mortgages. Coordinate with ministries, local branches and borrowers to urgently

debt recovery policy for units borrowing capital to construct basic construction works, aiming to completely handle outstanding basic construction debts by the end of 2006.

For state-owned enterprises undergoing transformation, the State Bank also requires resolute solutions such as: in case of delay in loan repayment, credit institutions need to apply legal measures to recover debts, including handling mortgaged, pledged and guaranteed assets, and even filing lawsuits with the court.

Recently, the State Bank of Vietnam has issued Circular 13 and Circular 19 on safety ratios in the operations of credit institutions. According to this Decision, credit institutions, except foreign bank branches, must maintain a minimum ratio of 9% between equity capital and total assets with risks. For state-owned commercial banks, this ratio is currently lower than 9%, and within 2011, it must increase to at least the prescribed level. This is not an easy requirement for state-owned commercial banks, because their equity capital is currently low. In addition, the State Bank of Vietnam also requires credit institutions to implement a series of other criteria, such as specifically determining the credit limit applicable to each customer; total outstanding loans to a customer must not exceed 15% of the credit institution's equity capital; Maintain a minimum ratio of 25% between the value of “assets” that can be paid immediately and “liabilities” that will be due for payment within the next 1 month.

In fact, the situation of "hot" credit development leading to increased overdue debt has been a difficult problem for the Vietnamese credit system for many years. To solve this problem, experts say that, in addition to the strict control of the State Bank, credit institutions themselves must strictly comply with regulations on operational safety. At the macro level, the Government and ministries and branches need to soon come up with strong solutions to develop the stock market, in order to create a new capital circulation channel in the economy, capable of sharing the credit burden with the banking system.

3.2.1.5. Synchronously develop component markets including the Interbank market, GTCG market, foreign exchange market, and credit market.

+ Develop domestic and foreign exchange markets.

The State Bank needs to review documents related to these markets to supplement and edit them to reduce the segmentation of the information market. In addition, the State Bank also needs to improve the quality of collecting and providing information on the information market to create

conditions for market members to easily access necessary information to help determine limits, prices, etc. in transactions with partners.

The State Bank needs to create conditions to ensure that the relationship between the domestic currency market and the interbank foreign currency market is very close to promptly and fully convey information changes from one market to the other.

The State Bank of Vietnam needs to create a legal corridor for the interbank market, noting that hot loan transactions on the interbank market do not require collateral, thereby minimizing collateral on the interbank market. Lending and borrowing transactions can be conducted through currency brokers and should have a term of 1-15 days.

The State Bank of Vietnam creates conditions for all healthy financial institutions to become members of the interbank market, thereby contributing to reducing risks for transactions in the interbank market. At the same time, it loosens restrictions on foreign banks in mobilizing domestic deposits or lending to domestic people, gradually increasing the proportion of foreign ownership in domestic banks, but the control of domestic banks is still in the hands of Vietnamese shareholders.

+ Developing credit market and GTCG market (repo).

In this period, focusing on developing the repo market is a correct direction because after the global financial crisis, the credit market for lending and secured deposits has been focused on. The State Bank of Vietnam (SBV) in coordination with the Ministry of Finance (MOF) has developed a plan to gradually develop the repo market. This should start with further exploiting commercial banks, then developing interbank repo activities, followed by repo between banks and other institutions, such as securities companies and investment organizations.

To develop the repo market, it is necessary to develop a standard repurchase agreement that is uniformly applied to GTCG repurchase transactions for all members of the TTTT. However, some units under the Ministry of Finance (SSC, State Securities Commission) and the Association of Government Bond Traders (VNBF) are also implementing this task. To avoid overlap in the implementation of tasks between receiving units and organizations, the State Bank of Vietnam (SBV) coordinates with the Ministry of Finance and related units to establish