The study also assessed the level of commitment in AFAS 9. Accordingly, the level of openness for mode 2 of Vietnam is quite high; meanwhile, there is a tendency to be cautious with modes 1 and 3 (when not completing the quantity and level of commitment as set out in the AEC Blueprint) and almost no commitment to open for mode 4. The sectors that Vietnam has the most open commitments under mode 3 include environmental services, education, distribution, and healthcare (See Table 3.14). In particular, in the education and healthcare sub-sectors, the level of openness of Vietnam is only lower than Singapore, while most other ASEAN countries open very little in these sub-sectors. On average for mode 3, the level of openness in Vietnam's service sector is only behind Singapore, Thailand, and Cambodia. The transportation and entertainment service sub-sectors have the lowest level of open commitments (Ishido, 2017).

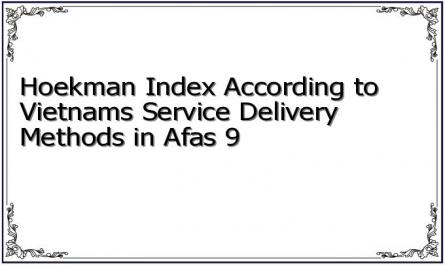

Table 3.14: Hoekman index according to Vietnam's service delivery methods in AFAS 9

STT

Service industry | Method 1 | Method 2 | Method 3 | |

1 | Business Services | 0.53 | 0.53 | 0.41 |

2 | Telecommunication services | 0.34 | ||

3 | Construction and related engineering services | 0 | 1.0 | 0.5 |

4 | Distribution services | 0.5 | 0.8 | 0.55 |

5 | Educational Services | 0.6 | 1.0 | 0.6 |

6 | Environmental Services | 0.63 | 1.0 | 0.81 |

7 | Financial Services | No pressure use | No pressure use | No pressure use |

8 | Health and social services | 0.75 | 0.75 | 0.5 |

9 | Travel services | 0.75 | 0.75 | 0.44 |

10 | Entertainment, cultural and sports services | 0 | 0.4 | 0.3 |

11 | Transportation services | 0.24 | 0.26 | 0.19 |

Medium | 0.43 | 0.69 | 0.47 |

Maybe you are interested!

-

Identify Rating Levels and Rating Scales

zt2i3t4l5ee

zt2a3gstourism,quan lan,quang ninh,ecology,ecotourism,minh chau,van don,geography,geographical basis,tourism development,science

zt2a3ge

zc2o3n4t5e6n7ts

of the islanders. Therefore, this indicator will be divided into two sub-indicators:

a1. Natural tourism attractiveness a2. Cultural tourism attractiveness

b. Tourist capacity

The two island communes in Quan Lan have different capacities to receive tourists. Minh Chau Commune is home to many standard hotels and resorts, attracting high-income domestic and international tourists. Meanwhile, Quan Lan Commune has many motels mainly built and operated by local people, so the scale and quality are not high, and will be suitable for ordinary tourists such as students.

c. Time of exploitation of Quan Lan Island Commune:

Quan Lan tourism is seasonal due to weather and climate conditions and festivals only take place on certain days of the year, specifically in spring. In Quan Lan commune, the period from April to June and from September to November is considered the best time to visit Quan Lan because the cultural tourism activities are mainly associated with festivals taking place during this time.

Minh Chau island commune:

Tourism exploitation time is all year round, because this is a place with a number of tourist attractions with diverse ecosystems such as Bai Tu Long National Park Research Center, Tram forest, Turtle Laying Beach, so besides coming to the beach for tourism and vacation in the summer, Minh Chau will attract research groups to come for tourism combined with research at other times of the year.

d. Sustainability

The sustainability of ecotourism sites in Quan Lan and Minh Chau communes depends on the sensitivity of the ecosystems to climate changes.

landscape. In general, these tourist destinations have a fairly high level of sustainability, because they are natural ecosystems, planned and protected. However, if a large number of tourists gather at certain times, it can exceed the carrying capacity and affect the sustainability of the environment (polluted beaches, damaged trees, animals moving away from their habitats, etc.), then the sustainability of the above ecosystems (natural ecosystems, human ecosystems) will also be affected and become less sustainable.

e. Location and accessibility

Both island communes have ports to take tourists to visit from Van Don wharf:

- Quan Lan – Van Don traffic route:

Phuc Thinh – Viet Anh high-speed boat and Quang Minh high-speed boat, depart at 8am and 2pm from Van Don to Quan Lan, and at 7am and 1pm from Quan Lan to Van Don. There are also wooden boats departing at 7am and 1pm.

- Van Don - Minh Chau traffic route:

Chung Huong high-speed train, Minh Chau train, morning 7:30 and afternoon 13:30 from Van Don to Minh Chau, morning 6:30 and afternoon 13:00 from Minh Chau to Van Don.

f. Infrastructure

Despite receiving investment attention, the issue of infrastructure and technical facilities for tourism on Quan Lan Island is still an issue that needs to be resolved because it has a direct impact on the implementation of ecotourism activities. The minimum conditions for serving tourists such as accommodation, electricity, water, communication, especially medical services, and security work need to be given top priority. Ecotourism spots in Minh Chau commune are assessed to have better infrastructure and technical facilities for tourism because there are quite complete and synchronous conditions for serving tourists, meeting many needs of domestic and foreign tourists.

3.2.1.4. Determine assessment levels and assessment scales

Corresponding to the levels of each criterion, the index is the score of those levels in the order of 4, 3, 2, 1 decreasing according to the standard of each level: very attractive (4), attractive (3), average (2), less attractive (1).

3.2.1.5. Determining the coefficients of the criteria

For the assessment of DLST in the two communes of Quan Lan and Minh Chau islands, the students added evaluation coefficients to show the importance of the criteria and indicators as follows:

Coefficient 3 with criteria: Attractiveness, Exploitation time. These are the 2 most important criteria for attracting tourists to tourism in general and eco-tourism in particular, so they have the highest coefficient.

Coefficient 2 with criteria: Capacity, Infrastructure, Location and accessibility . Because the assessment area is an island commune of Van Don district, the above criteria are selected by the author with appropriate coefficients at the average level.

Coefficient 1 with criteria: Sustainability. Quan Lan has natural and human-made ecotourism sites, with high biodiversity and little impact from local human factors. Most of the ecotourism sites are still wild, so they are highly sustainable.

3.2.1.6. Results of DLST assessment on Quan Lan island

a. Assessment of the potential for natural tourism development

For Minh Chau commune:

+ Natural tourism attractiveness is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined as average (2 points) and the coefficient is quite important (coefficient 2), then the score of Capacity criterion is 2 x 2 = 4.

+ Exploitation time is long (4 points), the most important coefficient (coefficient 3) so the score of the Exploitation time criterion is 4 x 3 = 12.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is assessed as good (3 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 3 x 2 = 6 points.

The total score for evaluating DLST in Minh Chau commune according to 6 evaluation criteria is determined as: 12 + 4 + 12 + 4 + 4 + 6 = 42 points

Similar assessment for Quan Lan commune, we have the following table:

Table 3.3: Assessment of the potential for natural ecotourism development in Quan Lan and Minh Chau communes

Attractiveness of self-tourismof course

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

CommuneMinh Chau

12

12

4

8

12

12

4

4

4

8

6

8

42/52

Quan CommuneLan

6

12

6

8

9

12

4

4

4

8

4

8

33/52

b. Assessment of the potential for humanistic tourism development

For Quan Lan commune:

+ The attractiveness of human tourism is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined to be large (3 points) and the coefficient is quite important (coefficient 2), then the score of the Capacity criterion is 3 x 2 = 6.

+ Mining time is average (3 points), the most important coefficient (coefficient 3) so the score of the Mining time criterion is 3 x 3 = 9.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points.

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is rated as average (2 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 2 x 2 = 4 points.

The total score for evaluating DLST in Quan Lan commune according to 6 evaluation criteria is determined as: 12 + 6 + 6 + 4 + 4 + 4 = 36 points.

Similar assessment with Minh Chau commune we have the following table:

Table 3.4: Assessment of the potential for developing humanistic eco-tourism in Quan Lan and Minh Chau communes

Attractiveness of human tourismliterature

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Quan CommuneLan

12

12

6

8

9

12

4

4

4

8

4

8

39/52

Minh CommuneChau

6

12

4

8

12

12

4

4

4

8

6

8

36/52

Basically, both Minh Chau and Quan Lan localities have quite favorable conditions for developing ecotourism. However, Quan Lan commune has more advantages to develop ecotourism in a humanistic direction, because this is an area with many famous historical relics such as Quan Lan Communal House, Quan Lan Pagoda, Temple worshiping the hero Tran Khanh Du, ... along with local festivals held annually such as the wind praying ceremony (March 15), Quan Lan festival (June 10-19); due to its location near the port and long exploitation time, the beaches in Quan Lan commune (especially Quan Lan beach) are no longer hygienic and clean to ensure the needs of tourists coming to relax and swim; this is also an area with many beautiful landscapes such as Got Beo wind pass, Ong Phong head, Voi Voi cave, but the ability to access these places is still very limited (dirt hill road, lots of gravel and rocks), especially during rainy and windy times; In addition, other natural resources such as mangrove forests and sea worms have not been really exploited for tourism purposes and ecotourism development. On the contrary, Minh Chau commune has more advantages in developing ecotourism in the direction of natural tourism, this is an area with diverse ecosystems such as at Rua De Beach, Bai Tu Long National Park Conservation Center...; Minh Chau beach is highly appreciated for its natural beauty and cleanliness, ranked in the top ten most beautiful beaches in Vietnam; Minh Chau commune is also home to Tram forest with a large area and a purity of up to 90%, suitable for building bridges through the forest (a very effective type of natural ecotourism currently applied by many countries) for tourists to sightsee, as well as for the purpose of studying and researching.

Figure 3.1: Thenmala Forest Bridge (India) Source: https://www.thenmalaecotourism.com/(August 21, 2019)

3.2.2. Using SWOT matrix to evaluate Quan Lan island tourism

General assessment of current tourism activities of Quan Lan island is shown through the following SWOT matrix:

Table 3.5: SWOT matrix evaluating tourism activities on Quan Lan island

Internal agent

Strengths- There is a lot of potential for tourism development, especially natural ecotourism and humanistic ecotourism.- The unskilled labor force is relatively abundant.- resource environmentunpolluted, still

Weaknesses- Poorly developed infrastructure, especially traffic routes to tourist destinations on the island.- The team of professional staff is still weak.- Tourism products in general

quite wild, originalintact

general and DLST in particularalone is monotonous.

External agents

Opportunity- Tourism is a key industry in the socio-economic development strategy of the province and Van Don economic zone.- Quan Lan was selected as a pilot area for eco-tourism development within the framework of the green growth project between Quang Ninh province and the Japanese organization JICA.- The flow of tourists and especially ecotourism in the world tends toincreasing

Challenge- Weather and climate change abnormally.- Competition in tourism products is increasingly fierce, especially with other localities in the province such as Ha Long, Mong Cai...- Awareness of tourists, especially domestic tourists, about ecotourism and nature conservation is not high.

Through summary analysis using SWOT matrix we see that:

To exploit strengths and take advantage of opportunities, it is necessary to:

- Diversify products and service types (build more tourism routes aimed at specific needs of tourists: experiential tourism immersed in nature, spiritual cultural tourism...)

- Effective exploitation of resources and differentiated products (natural resources and human resources)

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s3 { color: #0D0D0D; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -3pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -2pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -1pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s10 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s12 { color: black; font-family:Symbol, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s13 { color: black; font-family:Wingdings; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s14 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s16 { color: black; font-family:Cambria, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s17 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s18 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s19 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s20 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; } div.maincontent .s21 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 11pt; } div.maincontent .s22 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s23 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s24 { color: #212121; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Identify Rating Levels and Rating Scales

zt2i3t4l5ee

zt2a3gstourism,quan lan,quang ninh,ecology,ecotourism,minh chau,van don,geography,geographical basis,tourism development,science

zt2a3ge

zc2o3n4t5e6n7ts

of the islanders. Therefore, this indicator will be divided into two sub-indicators:

a1. Natural tourism attractiveness a2. Cultural tourism attractiveness

b. Tourist capacity

The two island communes in Quan Lan have different capacities to receive tourists. Minh Chau Commune is home to many standard hotels and resorts, attracting high-income domestic and international tourists. Meanwhile, Quan Lan Commune has many motels mainly built and operated by local people, so the scale and quality are not high, and will be suitable for ordinary tourists such as students.

c. Time of exploitation of Quan Lan Island Commune:

Quan Lan tourism is seasonal due to weather and climate conditions and festivals only take place on certain days of the year, specifically in spring. In Quan Lan commune, the period from April to June and from September to November is considered the best time to visit Quan Lan because the cultural tourism activities are mainly associated with festivals taking place during this time.

Minh Chau island commune:

Tourism exploitation time is all year round, because this is a place with a number of tourist attractions with diverse ecosystems such as Bai Tu Long National Park Research Center, Tram forest, Turtle Laying Beach, so besides coming to the beach for tourism and vacation in the summer, Minh Chau will attract research groups to come for tourism combined with research at other times of the year.

d. Sustainability

The sustainability of ecotourism sites in Quan Lan and Minh Chau communes depends on the sensitivity of the ecosystems to climate changes.

landscape. In general, these tourist destinations have a fairly high level of sustainability, because they are natural ecosystems, planned and protected. However, if a large number of tourists gather at certain times, it can exceed the carrying capacity and affect the sustainability of the environment (polluted beaches, damaged trees, animals moving away from their habitats, etc.), then the sustainability of the above ecosystems (natural ecosystems, human ecosystems) will also be affected and become less sustainable.

e. Location and accessibility

Both island communes have ports to take tourists to visit from Van Don wharf:

- Quan Lan – Van Don traffic route:

Phuc Thinh – Viet Anh high-speed boat and Quang Minh high-speed boat, depart at 8am and 2pm from Van Don to Quan Lan, and at 7am and 1pm from Quan Lan to Van Don. There are also wooden boats departing at 7am and 1pm.

- Van Don - Minh Chau traffic route:

Chung Huong high-speed train, Minh Chau train, morning 7:30 and afternoon 13:30 from Van Don to Minh Chau, morning 6:30 and afternoon 13:00 from Minh Chau to Van Don.

f. Infrastructure

Despite receiving investment attention, the issue of infrastructure and technical facilities for tourism on Quan Lan Island is still an issue that needs to be resolved because it has a direct impact on the implementation of ecotourism activities. The minimum conditions for serving tourists such as accommodation, electricity, water, communication, especially medical services, and security work need to be given top priority. Ecotourism spots in Minh Chau commune are assessed to have better infrastructure and technical facilities for tourism because there are quite complete and synchronous conditions for serving tourists, meeting many needs of domestic and foreign tourists.

3.2.1.4. Determine assessment levels and assessment scales

Corresponding to the levels of each criterion, the index is the score of those levels in the order of 4, 3, 2, 1 decreasing according to the standard of each level: very attractive (4), attractive (3), average (2), less attractive (1).

3.2.1.5. Determining the coefficients of the criteria

For the assessment of DLST in the two communes of Quan Lan and Minh Chau islands, the students added evaluation coefficients to show the importance of the criteria and indicators as follows:

Coefficient 3 with criteria: Attractiveness, Exploitation time. These are the 2 most important criteria for attracting tourists to tourism in general and eco-tourism in particular, so they have the highest coefficient.

Coefficient 2 with criteria: Capacity, Infrastructure, Location and accessibility . Because the assessment area is an island commune of Van Don district, the above criteria are selected by the author with appropriate coefficients at the average level.

Coefficient 1 with criteria: Sustainability. Quan Lan has natural and human-made ecotourism sites, with high biodiversity and little impact from local human factors. Most of the ecotourism sites are still wild, so they are highly sustainable.

3.2.1.6. Results of DLST assessment on Quan Lan island

a. Assessment of the potential for natural tourism development

For Minh Chau commune:

+ Natural tourism attractiveness is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined as average (2 points) and the coefficient is quite important (coefficient 2), then the score of Capacity criterion is 2 x 2 = 4.

+ Exploitation time is long (4 points), the most important coefficient (coefficient 3) so the score of the Exploitation time criterion is 4 x 3 = 12.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is assessed as good (3 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 3 x 2 = 6 points.

The total score for evaluating DLST in Minh Chau commune according to 6 evaluation criteria is determined as: 12 + 4 + 12 + 4 + 4 + 6 = 42 points

Similar assessment for Quan Lan commune, we have the following table:

Table 3.3: Assessment of the potential for natural ecotourism development in Quan Lan and Minh Chau communes

Attractiveness of self-tourismof course

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

CommuneMinh Chau

12

12

4

8

12

12

4

4

4

8

6

8

42/52

Quan CommuneLan

6

12

6

8

9

12

4

4

4

8

4

8

33/52

b. Assessment of the potential for humanistic tourism development

For Quan Lan commune:

+ The attractiveness of human tourism is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined to be large (3 points) and the coefficient is quite important (coefficient 2), then the score of the Capacity criterion is 3 x 2 = 6.

+ Mining time is average (3 points), the most important coefficient (coefficient 3) so the score of the Mining time criterion is 3 x 3 = 9.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points.

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is rated as average (2 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 2 x 2 = 4 points.

The total score for evaluating DLST in Quan Lan commune according to 6 evaluation criteria is determined as: 12 + 6 + 6 + 4 + 4 + 4 = 36 points.

Similar assessment with Minh Chau commune we have the following table:

Table 3.4: Assessment of the potential for developing humanistic eco-tourism in Quan Lan and Minh Chau communes

Attractiveness of human tourismliterature

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Quan CommuneLan

12

12

6

8

9

12

4

4

4

8

4

8

39/52

Minh CommuneChau

6

12

4

8

12

12

4

4

4

8

6

8

36/52

Basically, both Minh Chau and Quan Lan localities have quite favorable conditions for developing ecotourism. However, Quan Lan commune has more advantages to develop ecotourism in a humanistic direction, because this is an area with many famous historical relics such as Quan Lan Communal House, Quan Lan Pagoda, Temple worshiping the hero Tran Khanh Du, ... along with local festivals held annually such as the wind praying ceremony (March 15), Quan Lan festival (June 10-19); due to its location near the port and long exploitation time, the beaches in Quan Lan commune (especially Quan Lan beach) are no longer hygienic and clean to ensure the needs of tourists coming to relax and swim; this is also an area with many beautiful landscapes such as Got Beo wind pass, Ong Phong head, Voi Voi cave, but the ability to access these places is still very limited (dirt hill road, lots of gravel and rocks), especially during rainy and windy times; In addition, other natural resources such as mangrove forests and sea worms have not been really exploited for tourism purposes and ecotourism development. On the contrary, Minh Chau commune has more advantages in developing ecotourism in the direction of natural tourism, this is an area with diverse ecosystems such as at Rua De Beach, Bai Tu Long National Park Conservation Center...; Minh Chau beach is highly appreciated for its natural beauty and cleanliness, ranked in the top ten most beautiful beaches in Vietnam; Minh Chau commune is also home to Tram forest with a large area and a purity of up to 90%, suitable for building bridges through the forest (a very effective type of natural ecotourism currently applied by many countries) for tourists to sightsee, as well as for the purpose of studying and researching.

Figure 3.1: Thenmala Forest Bridge (India) Source: https://www.thenmalaecotourism.com/(August 21, 2019)

3.2.2. Using SWOT matrix to evaluate Quan Lan island tourism

General assessment of current tourism activities of Quan Lan island is shown through the following SWOT matrix:

Table 3.5: SWOT matrix evaluating tourism activities on Quan Lan island

Internal agent

Strengths- There is a lot of potential for tourism development, especially natural ecotourism and humanistic ecotourism.- The unskilled labor force is relatively abundant.- resource environmentunpolluted, still

Weaknesses- Poorly developed infrastructure, especially traffic routes to tourist destinations on the island.- The team of professional staff is still weak.- Tourism products in general

quite wild, originalintact

general and DLST in particularalone is monotonous.

External agents

Opportunity- Tourism is a key industry in the socio-economic development strategy of the province and Van Don economic zone.- Quan Lan was selected as a pilot area for eco-tourism development within the framework of the green growth project between Quang Ninh province and the Japanese organization JICA.- The flow of tourists and especially ecotourism in the world tends toincreasing

Challenge- Weather and climate change abnormally.- Competition in tourism products is increasingly fierce, especially with other localities in the province such as Ha Long, Mong Cai...- Awareness of tourists, especially domestic tourists, about ecotourism and nature conservation is not high.

Through summary analysis using SWOT matrix we see that:

To exploit strengths and take advantage of opportunities, it is necessary to:

- Diversify products and service types (build more tourism routes aimed at specific needs of tourists: experiential tourism immersed in nature, spiritual cultural tourism...)

- Effective exploitation of resources and differentiated products (natural resources and human resources)

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s3 { color: #0D0D0D; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -3pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -2pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -1pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s10 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s12 { color: black; font-family:Symbol, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s13 { color: black; font-family:Wingdings; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s14 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s16 { color: black; font-family:Cambria, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s17 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s18 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s19 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s20 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; } div.maincontent .s21 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 11pt; } div.maincontent .s22 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s23 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s24 { color: #212121; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex -

Spillover effects of foreign direct investment on enterprises in Vietnam's textile and garment industry - 8

Spillover effects of foreign direct investment on enterprises in Vietnam's textile and garment industry - 8 -

Malaysia's policy of attracting foreign direct investment in the process of international economic integration - current situation, experience and possibility of application in Vietnam - 3

Malaysia's policy of attracting foreign direct investment in the process of international economic integration - current situation, experience and possibility of application in Vietnam - 3 -

Current situation and solutions to attract foreign direct investment in Vietnam's tourism industry - 2

Current situation and solutions to attract foreign direct investment in Vietnam's tourism industry - 2 -

Malaysia's policy of attracting foreign direct investment in the process of international economic integration - current situation, experience and possibility of application in Vietnam - 1

Malaysia's policy of attracting foreign direct investment in the process of international economic integration - current situation, experience and possibility of application in Vietnam - 1

(Source: Ishido, 2017)

Vietnam's general commitments in AFAS 9 have some higher content than Vietnam's general commitments in GATS. The service sectors with many sub-sectors in which Vietnam has opened more widely than the WTO are real estate business services, telecommunications, healthcare, tourism and transportation. Vietnam's separate commitment packages on financial services, construction, distribution, culture and sports up to now are still equivalent to the WTO (see Appendix 10.1). Compared with some agreements that Vietnam has just signed such as CPTPP and EVFTA, Vietnam's commitments in AFAS are at the same level or higher in some sub-sectors (see Appendix 10.2 and 10.3).

From the analysis of the practical commitments, it can be seen that the scope and depth of the commitments in the AEC related to investment in the service sector in Vietnam have a higher level of commitment, although not significantly, compared to other agreements that Vietnam has signed.

Commitments. The reliability of commitments - the implementation of commitments by the majority of ASEAN member countries, including Vietnam - has not been achieved as planned in the AEC Blueprint (in terms of the number of sub-sectors committed and the level of commitment, the progress of implementing the AFAS 10 package) because the provisions in AFAS are not yet binding. The limitations in scope and depth, as well as the failure of members to thoroughly implement the service sector integration commitments in AFAS, may cause the impact of the provisions in economic linkages on the decisive factors of attracting FDI to not be strongly promoted.

However, part of the reason is that Vietnam has a relatively high level of openness in GATS, so compared to many ASEAN countries, Vietnam's openness in some service sub-sectors such as education, healthcare, and distribution is superior. In fact, these are also service sub-sectors that attract a lot of FDI from ASEAN. VCCI (2016) also stated that although the breakthrough in promoting FDI flows in the ASEAN region thanks to the establishment of AEC is not large, for Vietnam, intra-bloc FDI flows into Vietnam can increase significantly. Research by Nguyen Duc Thanh et al. (2015) also demonstrated that Vietnam will be the country that benefits the most when AEC comes into effect in attracting intra-bloc investment, with different levels of increase depending on each scenario. In fact, FDI from ASEAN into Vietnam's service sectors has increased significantly in the number of projects and slightly increased in total investment capital after 2015 - the year the AEC was officially established.

3.3.3. Practice of implementing commitments in some service sectors

For the service sector, barriers and constraints are mainly policy, legal, regulatory and institutional barriers. Therefore, the implementation of AFAS commitments by countries in general and Vietnam in particular is mainly the promulgation or adjustment of policies, laws and regulations related to opening up this sector.

In general, Vietnam's commitments in AFAS have many similarities with those in GATS. Therefore, the process of opening up Vietnam's service sector and adjusting policies and regulations on services to comply with WTO commitments also serves to implement AFAS commitments. Basically, Vietnam is assessed to be making many efforts and seriously implementing AFAS commitments, as well as ACIA related to expanding investment portfolio.

Regarding the practice of adjusting policies in some specific service sectors, Vietnam has revised and issued policies to implement commitments in each specific sector of AFAS, especially in the banking, insurance, securities, distribution and telecommunications service sectors. The Government has also approved and signed the Protocol to implement the AFAS 9 service commitment package in accordance with ASEAN's schedule and so far has also

has completed the implementation of AFAS 9 commitment package. Some of Vietnam's efforts in implementing commitments in specific areas can be mentioned as follows.

Logistics services:As one of the priority sectors of AFAS, Vietnam has made many achievements in facilitating the implementation of commitments in AFAS. Vietnam has signed the Protocol on the ASEAN integration roadmap on logistics services and committed to opening up most of the main sub-sectors in logistics services. As a coordinating country in implementing the rapid integration roadmap in the logistics sector, Vietnam has proactively organized the Business Forum on Logistics Services on the sidelines of the 4th AEC Conference and AEM 42 (August 2010). At the same time, the completion of the system of legal documents and the improvement of the State's management capacity on logistics have also been actively promoted. Some important contributions include Project 30 on reforming customs procedures to promote the development of logistics services; Decision No. 950/QD/TTg in 2012 on the action program to implement the import-export strategy for the period 2011-2020, with a vision to 2030, emphasized the importance of socializing investment services in warehouses at major seaports, customs clearance points, logistics services, etc. In addition, for some service sub-sectors such as warehouse agents, freight forwarding agents, container loading and unloading services, customs clearance services, Vietnam has set a clear roadmap to allow increased foreign capital contribution and is considered one of the countries that most effectively promotes commitments related to logistics services in the region (Vu Thanh Huong and Tran Viet Dung, 2015).

Tourism services : Vietnam has also made many important contributions. In addition to signing the ASEAN Tourism Integration Protocol, Vietnam has presided over the development of the MRAs Implementation Guidebook for ASEAN tourism professions; proactively developed and trained tourism human resources; presided over research on the development of tourism products in ASEAN; produced documentary films to promote ASEAN tourism and actively participated in the ASEAN Tourism Forum... However, due to many weaknesses in infrastructure and unprofessional service quality, the foreign currency earned from tourism in Vietnam is still limited (Thanh Giang, 2011; My Hanh, 2014; Le Tuan Anh, 2014).

Health services : Vietnam has signed the ASEAN Health Sector Integration Protocol and actively participated in integration activities in areas such as pharmaceuticals and cosmetics, traditional medicine, preventive medicine, health services, food safety and hygiene... Vietnam also actively implemented the ASEAN Health Development Strategic Framework and hosted the 12th ASEAN Health Ministers' Meeting - helping to enhance Vietnam's position and prestige in the health sector in ASEAN (Minh Ngoc, 2013).

Distribution services:Foreign investors operating in Vietnam have had the right to establish 100% foreign-owned enterprises since January 11, 2015. At the same time, these enterprises also have more opportunities to proactively seek high-quality labor in business administration in the distribution sector from Vietnam and other countries in the ASEAN region (Tran Thi Ngoc Quyen, 2015).

Financial-banking and insurance services:By the end of 2019, Vietnam's commitments on financial services in the 7th commitment package (the package with the highest scope and level of openness) under AFAS were equivalent to the level of commitments in the WTO. However, Vietnam still maintains many measures to restrict market access with modes 3 and 4 - related to the form of enterprise establishment, land lease rights and capital contribution ratio of foreign service providers. For example, with banking services and other financial services, Vietnam stipulates that foreign commercial banks must not have a capital contribution exceeding 50% of charter capital, foreign commercial bank branches are not allowed to open transaction points other than the branch headquarters, the condition for establishing a branch of a foreign commercial bank in Vietnam is that the parent bank must have total assets of over 20 billion USD at the time of application... (Tao Thi Hue, 2020). Barriers to market entry, along with legal inconsistencies with international commitments, are the reasons for the limitations in attracting FDI from ASEAN into the finance-banking and insurance sector in Vietnam.

Regarding the mode of service provision: Regarding the implementation of the general commitments under mode 3 related to allowing ASEAN service suppliers to establish commercial presence in the committed forms, Vietnam has amended a number of relevant laws and issued decrees and documents guiding these laws. The amended Investment Law, Enterprise Law, and Commercial Law of Vietnam are quite closely aligned with and consistent with Vietnam's general commitments related to the forms of commercial presence.

Regarding the implementation of commitments on commercial presence of foreign service providers, Vietnam's legal documents have been adjusted in accordance with the content of commitments on market access restrictions, conditions on ownership, operation, legal entity form and scope of operation, land lease, capital contribution in legal and sub-law documents such as the 2005 Commercial Law, the 2014 Enterprise Law, the 2014 Investment Law, Decree No. 07/2016/ND-CP dated January 25, 2016 of the Government detailing the Commercial Law on representative offices and branches of foreign traders in Vietnam.

Regarding the general regulations on representative offices and branches of foreign companies in Vietnam previously applied under Decree 72/2006/ND-CP and Circular 11/2006/TT-BTM. In 2016, the Government issued Decree No. 07/2016/ND-CP detailing the Law on Commerce on representative offices and branches of foreign traders in Vietnam, replacing Decree 72 with a number of significant changes in accordance with international treaties to which Vietnam is a member. In addition, in specialized fields and specific activities such as establishment and operation of offices, business registration, fees for establishing representative offices, Vietnam also has its own regulations related to branches and representative offices of foreign companies such as Decree 100/2011/ND-CP dated October 28, 2011, Decree 43/2010/ND-CP dated April 15, 2010, Circulars 01/2013/TT-BKHDT, Circular 133/2012/TT-BTC. It can be seen that Vietnam's efforts in updating and amending policies and laws towards implementing AFAS's mode 3 commitments in particular and integration commitments in the service industry in general are very commendable.

Thus, although the level of service liberalization in AFAS has been committed to be quite deep and wide, there are still many problems when applying in practice in most ASEAN countries, including Vietnam. Some barriers can be mentioned as structural characteristics, such as factors related to corruption, lack of transparency in regulations and the presence of state-owned enterprises in strategic sectors, as well as potential macroeconomic issues, as well as natural barriers of the service sector. This reinforces the initial findings of many researchers that the gap between commitments and economic development among member countries has reduced the harmonization in management, especially for modes 3 and 4, the transparency and predictability of AFAS has been “severely hampered by the low level of governance in the region” (Bosworth et al., 2011; Dee, 2013). Other barriers to services liberalization include domestic rules such as continued restrictions on non-ASEAN ownership in certain industries. These concerns may have limited the achievements of AFAS (The ASEAN Secretariat, 2012).

The results of interviews with experts also stated that, compared to other economic links, especially the European Economic Community, the AEC has a shallow level of connection and is not highly binding. Increasing the depth of the AEC is also difficult to implement due to many reasons as general studies have shown. In addition, services are also a special industry, in which natural barriers to market entry are relatively large (such as culture, consumer habits, etc.). With a protectionist mentality, many

In order to limit monopoly and prioritize domestic development, Vietnam is still cautious in opening the service market. In fact, unlike goods, non-tariff barriers to trade and investment in services are very large. In addition to cautiously opening the service market, Vietnam has maintained many restrictions as well as used non-tariff barriers in a number of service sectors to limit market entry from foreign investors.

The official establishment of the AEC brings significant benefits to Vietnam's intra-bloc FDI attraction. However, Vietnam is also facing great competitive pressure from ASEAN countries in attracting intra-bloc FDI. When the AEC is officially established, Vietnam will not only compete with CLMV economies in terms of labor costs and quality, but also compete with other countries such as Thailand, Malaysia, Indonesia, etc. when the sub-sectors with the potential to attract FDI in Vietnam are also the strengths of these countries such as real estate business, tourism and accommodation services, wholesale and retail, logistics, etc. (Do Nhat Hoang, 2020).

CHAPTER 3 SUMMARY

Chapter 3 focuses on the study of the investment attraction situation and reality of ASEAN in the service industry and the practice of investment attraction policy in this industry of Vietnam. Chapter 3 gives the following conclusions:

1/ In general, FDI activities in the service sector of ASEAN countries in Vietnam have achieved many remarkable results over the periods but are still not commensurate with the potential and desire for cooperation. Some limitations include: (i) Low average capital scale of projects, (ii) Uneven project structure, (iii) Uneven investment partners, (iv) FDI capital flows are unbalanced by territory . In particular, after the AEC was officially established, although the number of projects has increased significantly, these limitations have not been resolved.

2/ Investment integration in Vietnam's service sectors is regulated by commitments in ACIA and AFAS. Although the level of service liberalization in AFAS has been committed quite deeply and widely, there are still many problems when applying in practice in most ASEAN countries. From the analysis of the practical commitments, it can be seen that the scope and depth of AEC integration commitments related to investment in Vietnam's service sector are higher, although not significantly, compared to other agreements that Vietnam has signed.

CHAPTER 4: ANALYSIS OF FACTORS AFFECTING FDI ATTRACTION FROM ASEAN INTO SERVICE SECTORS IN VIETNAM

IN THE CONTEXT OF AEC INTEGRATION

4.1. Quantitative analysis model

4.1.1. Research variables and data

4.1.1.1. Description of variables

Based on basic theories of FDI attraction, the author has synthesized empirical studies to identify factors affecting FDI in the service industry as shown in Figure

2.2. This is the basis for building variables in the analytical model. In addition, the model also considers the impact of AEC on FDI attraction activities in the service sector from ASEAN to Vietnam. Accordingly, the measurement variables used include: (1) dependent variable (FDI attraction variable in services); (2) independent variables and (3) dummy variables. These measurement variables will be presented in detail as follows:

Dependent variable: Dependent variable У it t is the FDI capital flow of ASEAN countries into Vietnam's service sectors in the corresponding years, taken as a logarithmic function. This variable shows that the FDI capital flow into the service sector in a specific country can be explained by providing attractive economic conditions, market potential, competitive resources, openness... The data is calculated from data of the Foreign Investment Agency - Ministry of Planning and Investment.

Independent variables: This model considers the factors that determine FDI inflows into service industries. Based on the theoretical basis of groups of factors affecting investment decisions, the model considers the investment motives of multinational companies, including the following factors: Market size and potential (GROWTH), trade openness (OPEN), human resource quality (TERTIARY 3 ), infrastructure (INFRA), exchange rate (EXR), financial development (FDIX), inflation (INF) and institutional-political quality (PS).

Dummy variable: The model examines the impact of AEC on FDI inflows into the service sector from ASEAN to Vietnam and AEC was officially established in 2015 – the dummy variable AEC will be used to explain this factor, in which the dummy variable has the value 0 before 2015 and the value 1 for the years 2015-2019.

The independent variables and research hypotheses are presented in Table 4.1. Specific descriptions of the variables are presented in detail in Appendix 11.

3 The quality of human resources is measured by the proportion of workers with general education or higher (Tertiary education), so it is denoted as TERTIARY.

4.1.1.2. Research data

The data collected and used for this study are secondary data and the tools used are excel and Stata statistical software to support the regression analysis. The data is taken from two main sources, the Foreign Investment Agency and the World Bank, besides that the author uses some other data sources from Trading Economics and The Global Economy.

The research sample includes 7 countries in the ASEAN bloc including Thailand, Singapore, Indonesia, Philippines, Malaysia, Brunei, Myanmar because these are countries that contribute a lot to FDI in Vietnam's service industry and the data of these countries are relatively complete. Data was collected in the period from 2004 to 2019 with 109 observations - this is the longest period that can get complete data. Some values of the dependent variable Y have no data because in those years these ASEAN countries did not invest in the service industry in Vietnam. In addition, there are some variables such as the openness of the economy (OPEN), the quality of human resources variable (TERTIARY) that are missing observations due to insufficient data updates.

4.1.2. Model and estimation method

4.1.2.1. Research model

The overview presented in Chapter 1 shows that most of the relevant empirical studies use panel data models. Therefore, the thesis also uses the estimation method for panel data, specifically the pooled least squares method (ROL OLS), studying two random effects models - REM (random effects model) and fixed effects model - FEM (fixed effects model). With the panel data estimation method, the research model is written in the form of a pooled regression model (ROL Mоdel) as follows:

У it = β 0 + β 1 Х it + ϒ'Х it + ε it

In which У it is the dependent variable (FDI) and Х it are the explanatory variables in the model . With the notation of the explanatory variables presented in the above section, the model can be rewritten as the Рооеd ОLS model as follows:

У it = β 0 + β 1 EXR it + β 2 OPEN it + β 3 FDIX it + β 4 GROWTH it + β 5 TERTIARY

it + β 6 INFRA it + β 7 PS it + β 8 INF it + ϒ 1 AEC it + ε it

In which: t – time (from 2004-2019) i: data of Vietnam

The pooled regression model is simply the ordinary least squares (OLS) estimation method. However, this OLS method will be suitable if there are no separate factors and time factors. According to Gujarati (2004), the use of the OLS method ignores the spatial and temporal dimensions of the pooled data, the estimation results may be biased. Therefore, the fixed effects estimation method (FEM)