2.2.1. Return on total assets (ROA)

ROA is the return on total assets - a measure of operational efficiency regardless of financial structure. This indicator shows how much profit after tax a bank generates from one dong of assets. On the other hand , assets are formed from loans and equity, both of which are used to finance the bank's operations and ROA shows the efficiency of converting assets into profits. The higher the ROA, the more effective the operation and management ability of the board of directors. The return on total assets (ROA) is the indicator used in most studies measuring the profitability of banks such as the study of Deger Alper and Adem Anbar (2011) in Istanbul - Turkey; Serish Gul, Faiza Irshad and Khalid Zaman (2011) in Pakistan; Autonia Davydenko (2011) in Ukraine; Fadzlan Sufian (2011) in Korea….

Maybe you are interested!

-

Factors affecting the debt repayment ability of corporate customers at Vietnam Joint Stock Commercial Bank for Investment and Development - Long An Branch - 1

Factors affecting the debt repayment ability of corporate customers at Vietnam Joint Stock Commercial Bank for Investment and Development - Long An Branch - 1 -

Factors affecting customer satisfaction with the quality of international money transfer services at Dong A Commercial Joint Stock Bank - 1

Factors affecting customer satisfaction with the quality of international money transfer services at Dong A Commercial Joint Stock Bank - 1 -

Factors affecting customer loyalty to international payment services at Asia Commercial Joint Stock Bank - 12

Factors affecting customer loyalty to international payment services at Asia Commercial Joint Stock Bank - 12 -

Factors affecting card acceptance of Kien Long Joint Stock Commercial Bank - 18

Factors affecting card acceptance of Kien Long Joint Stock Commercial Bank - 18 -

Factors affecting the decision of customers to deposit savings at Asia Commercial Joint Stock Bank - 1

Factors affecting the decision of customers to deposit savings at Asia Commercial Joint Stock Bank - 1

ROA = Debt minus Equity

fruit explosion

Rivard & Thomas (1997) also proved that ROA is the best quantification value for bank profits because ROA is not affected by financial leverage. Besides, ROA also has its own disadvantages such as eliminating the elements of off-balance sheet assets - representing an important source of profit (Davydenko, 2011)

2.2.2. Return on equity (ROE)

ROE is the ratio of net profit to equity, reflecting the bank's ability to use capital to generate income for shareholders. In other words, ROE measures the profitability of each dollar of capital that shareholders receive from investing in the bank. The higher the ROE ratio, the more effective the use of shareholders' capital, meaning that the bank has harmoniously balanced shareholders' capital with borrowed capital to exploit its competitive advantage. Therefore, the higher the ROE ratio, the more attractive the stock is to investors.

ROE = 𝐿𝑖𝑛𝑎𝑢𝑛𝑠𝑎𝑢𝑡ℎ𝑢𝑠

Ownership number

ROE research will show how the bank has used its investment capital to generate profits (Gul, Irshad and Zaman (2011)). The efficiency of bank operations is the top criterion to attract investment from shareholders, so managers always want to increase ROE by many measures such as promoting traditional product activities, diversifying modern products and strictly controlling risks....

2.2.3. Other measurement indicators

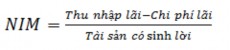

2.2.3.1. Net Interest Margin (NIM)

Net Interest Margin (NIM) is determined by total interest revenue minus total interest expenses (net interest income) over average total earning assets. In which, average total earning assets are determined by deposits at the State Bank, credit institutions, investment securities, loans to customers and other credit institutions. Net interest margin measures the difference between interest income and interest expenses through tight control of earning assets and pursuit of the lowest cost sources of funds, so the higher the NIM, the higher the bank's profitability.

The interest margin ratio is used as a dependent variable to analyze the factors affecting the profitability of banks in studies by Munyam Bonera (2013), Serish Gul, Faiza Irshad and Khalid Zaman (2011), Liu and Wilson (2010)….. However, NIM also has the disadvantage of not considering other income besides interest and operating expenses, so it does not fully reflect the profitability of banks.

2.2.3.2. Non-interest income margin (NNIM)

NNIM = 𝑇ℎ𝑢𝑛𝑔𝑜𝑖 𝑙𝑖𝑖 − 𝐶ℎ𝑖 𝑝ℎ𝑖 𝑙𝑖

Assets with 𝑙𝑖 ...

The non-interest income margin measures the difference between non-interest income and non-interest expenses. In which, non-interest income is mainly fee income from service products and non-interest expenses include salaries, repair costs, operating costs, etc. Therefore, the higher the NNIM ratio, the higher the bank's profitability.

2.2.3.3. Return on Capital Employed (ROCE)

ROCE = Return on Equity minus Net Income

Capital employed

Return on capital employed is an indicator that shows the bank's ability to earn profit based on the capital employed. In which, capital employed is calculated as the difference between total assets and current liabilities. The higher the ROCE, the higher the bank's profitability (Gul, Irshad and Zaman (2011))

Like all other financial indicators, each profitability ratio is used in different cases. To determine the factors affecting the profitability of commercial banks, most foreign and domestic studies often measure them by two indicators: net profit on average total assets (ROA) and net profit on average total equity (ROE). The advantages of the two indicators are that they are relatively simple, easy to calculate and highly general compared to other indicators. On the other hand, although they have different meanings, both indicate the operational efficiency to generate profits for the bank (according to Davydenko, 2011). Therefore, in this thesis, the author will take the two indicators ROA and ROE as dependent variables representing the profitability of joint stock commercial banks in Vietnam.

2.3. Factors affecting the profitability of commercial banks

Return on assets (ROA) and return on equity (ROE) – two factors measuring the profitability of banks are affected not only by internal factors but also by external macro factors. Internal factors are specific and distinct to each bank such as bank size, equity capital, outstanding loans, liquidity, etc. On the other hand, external factors are macro and are affected by the economic environment such as GDP growth rate, inflation, etc.

2.3.1. Internal factors

2.3.1.1. Bank size

Bank size is considered an intrinsic factor that determines the profitability of banks through total assets or total capital. In most studies, to avoid too large a difference in the total asset size of large banks compared to small banks, total assets are calculated by logarithm to base 10 and are the representative variable of bank size participating in the research model to avoid the phenomenon of variance change. In fact, based on the scale advantage, banks can increase their profits.

The positive relationship between bank size and profitability is the result of empirical research by Anper and Anbar (2011), Pasiouras and Kosmidou (2007). When the size is larger, banks can more easily access large capital sources at low costs, thereby meeting customers' borrowing needs and contributing to increasing bank profits. In addition, the positive relationship is also explained by economies of scale because when the size grows to a certain limit, it will bring advantages to banks in competition as well as efficiency in operations. However, there are also opposing opinions in the research of Eichengreen and Gibson (2001), Miller and Noulas (1997), Athanasoglou et al. (2005) indicating that the increase in capital size only has a positive impact on profitability to a certain extent. When the bank's scale is too large, it will increase management and operating costs, human resources cannot keep up with the growth of scale, causing the bank's risks to increase, at that time diseconomies of scale appear, leading to a decrease in the bank's TSSL.

2.3.1.2. Equity size

Owner's equity (VCSH) or bank's own capital is very important, it is the bank's own capital contributed initially by the owner and supplemented during the business operation. Owner's equity performs a number of irreplaceable functions, which are providing initial resources for the bank to maintain operations when it is newly established, creating the basis for customers to trust in transactions and preventing business risks.

business for the bank. Equity includes initial capital, additional capital during business operations and funds. Equity size is considered a valuable tool showing the capital status, safety and financial health of a bank.

The impact of equity on bank profitability can be quantified through the ratio of equity to total assets and there are two schools of thought on the above impact. According to the study of Molyneux and Thornton (1992) on the profitability of banks in 18 European countries in the period 1986-1989, they found a positive relationship between equity and bank profitability. Accordingly, banks with high equity not only meet the requirements of legal capital but also send a positive signal to the market about their ability to provide capital to the economy. In the same view, according to Short (1979), the ratio of equity to total assets of a bank is associated with its size because in fact large banks can access capital at low costs, plus good capital management and maintaining prudence in the loan portfolio will help banks generate higher profitability. Furthermore, larger equity capital will reduce the cost of capital (Molyneux and Thornton, 1992) and help banks withstand or offset financial risks including bankruptcy risk, thereby increasing bank profits. This argument is also supported in studies by Pasiouras and Kosmidou (2007), Syfari (2012).

Contrary to the above views, Ali, Khizer, Akhtar, Farhan and Zafar (2011) pointed out the negative correlation between the equity ratio and the bank's profitability, proving that the growth of equity must be accompanied by improving the efficiency of capital use, good capital management and avoiding the situation of too much excess capital that does not generate profit for the bank. In addition, there is another view according to the study of Sharma and Gounder (2012) that the relationship between capital structure and profitability is unpredictable.

2.3.1.3. Outstanding loans

Lending is the main business activity that generates profits for banks. The more the economy develops and integrates deeply, the faster the lending turnover of commercial banks increases and the types of loans become extremely diverse. Lending is understood as a form of credit granting, in which the bank transfers the right to use a sum of money to customers for a certain purpose and time according to the agreement with the principle of repayment of both principal and interest. On the other hand, as an intermediary financial institution, the amount of credit capital is mainly from mobilized capital, so the bank must control the risks and purposes of capital use of customers to avoid affecting business results.

In most studies, the impact of loan balance on bank profitability is often measured by the ratio of loan balance to total assets and there are two views on the above impact. Gul, Irshad and Zaman (2011), Sufian and Habibullah (2009), Athanasoglou et al. (2006) have shown a positive correlation between loan balance and bank profitability, meaning that if lending increases, interest income will increase, contributing to increasing bank income. However, if only focusing on lending and disbursing a lot without controlling risks, it will lead to many difficult or uncollectible loans, reducing bank profits. That argument has been supported by the research results of Syfari (2012), Alper and Anbar (2011) on the negative correlation between outstanding loans and bank's TSSL, meaning that in addition to increasing lending activities, it is also necessary to focus on credit quality to ensure efficiency in business operations.

2.3.1.4. Credit risk

Credit risk occurs when customers fail to fulfill the terms committed in the loan contract with the bank. This is the biggest type of risk, occurs frequently and causes serious consequences in business activities. Most previous studies have shown that credit risk is one of the important variables in studying the factors affecting the bank's TSSL. A typical example is the study of

Athanasoglou et al. (2005), Davydenko (2011), Miller and Noulas (1997), Duca and MC Laughlin (1990) have shown an inverse relationship between credit risk and bank profitability. That is, when the loan portfolio includes many large loans, the risk will increase sharply if customers violate the contract, at this time banks have to set up more provisions, thereby increasing operating costs and reducing profitability. Therefore, banks need to improve the quality of loans rather than racing for quantity to increase scale and at the same time must organize training and professional training for credit officers to minimize risks in the best way. However, there is also a conflicting view according to the study of Heffernan and Fu (2008) that high credit risk will have a positive impact on bank profits if asset quality is good. On that basis, if a bank wants to achieve high TSSL, it must simultaneously accept high risks but the asset quality must be good and be closely assessed to limit losses for the bank. To represent the credit risk that banks face, previous studies often use the ratio of credit risk provisions to total outstanding loans.

2.3.1.5. Operating costs

Each business activity brings a certain income to the bank and at the same time creates expenses that the bank must manage well to increase operational efficiency. Operating expenses (or non-interest expenses) of the bank include taxes, fees, and charges; salaries, allowances, and subsidies for employees; property expenses; public service management expenses; customer deposit insurance expenses; provision expenses (excluding provision expenses for credit risks and securities price reductions) and other operating expenses.

Previous studies have shown that operating costs are also one of the factors affecting the profitability and are quantified by the ratio of operating costs to total operating income of the bank. Research by Pasiouras and Kosmidou (2007), Bourke (1989) and Syfari (2012) shows that if the bank knows how to cut and manage costs effectively, it will bring high profitability, implying a negative correlation between operating costs and the profitability of the bank. However, Molyneux and Thornton

(1992) gave a contrasting opinion that operating costs have a positive correlation with TSSL when examining banks from 18 European countries during the period 1986 - 1989. The study showed that when banks increase salary costs, bonuses for employees under the condition that other factors remain unchanged, it will promote working spirit and improve their productivity, thereby increasing TSSL for banks.

2.3.1.6. Liquidity

Bank liquidity is considered as the short-run ability to meet the demand for deposit withdrawals and disburse committed credits. Therefore, banks will constantly face liquidity problems and need to maintain liquid or quick-run assets that can be easily converted into cash to avoid temporary shortages that lead to loss of bank reputation or even bankruptcy. Most previous studies have shown that liquidity is also one of the factors affecting the TSSL of banks and is quantified by the ratio of liquid assets to total assets of the bank. In which, liquid assets include: cash, gold, silver, precious stones; deposits at the State Bank of Vietnam; deposits at and loans to other credit institutions (according to research by Etienne Bordeleau and Christopher Graham (2010), Vodova (2013)). Bourke's (1989) study showed a positive relationship between liquidity and bank profitability, arguing that banks with high liquidity will reduce the risk of bankruptcy because they can withstand financial risks while reducing the cost of borrowing from external sources of funding, thereby helping to increase bank profits. However, holding assets that are easily converted into cash to ensure liquidity needs to be maintained at a reasonable level because assets at a safe level will have low profitability, thereby affecting the profitability. This argument was supported by the research results of Molyneux and Thornton (1992) on the negative relationship between liquidity and bank profitability.