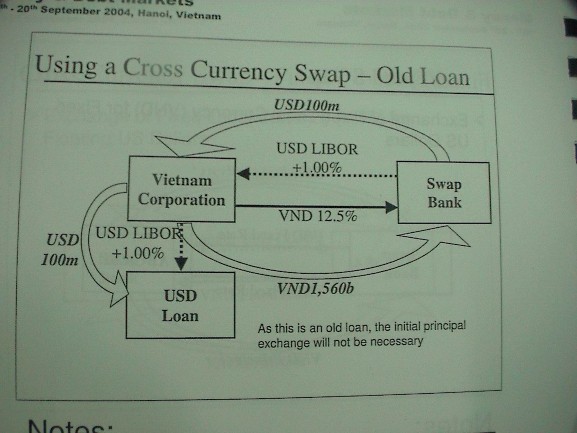

In the diagram above we see a Vietnamese company with a debt in USD of 100 million. To hedge against currency risk (exchange rate risk), this company has entered into a swap transaction with a bank.

We understand the above diagram as follows: Suppose a Vietnamese company has a foreign currency debt of 100 million USD and must pay it after 6 months. The interest rate of this debt is the floating interest rate LIBOR + 1%. To avoid exchange rate risk (because the interest rate to be paid is the floating interest rate), the company makes a Swap transaction with a bank (Swap Bank) and transfers to this bank (transfers in advance) 1,560 billion VND and considers this as a loan to Swap Bank with a fixed interest rate of 12.5% per year (this number needs to be determined in the contract). The bank will take on the exchange rate risk for itself, that is, accept to pay the company the above debt when it is due and according to the floating exchange rate LIBOR of the dollar + 1%. In return, the Vietnamese company has to calculate a fixed interest rate

12% interest rate (which the bank enjoys) on the amount of Vietnamese currency that the company deposits into the bank. This interest rate is higher than the market interest rate because it includes a risk compensation fee for the bank.

Maybe you are interested!

-

Determining the price of residential land for compensation when the State recovers land according to current Vietnamese law - 2

Determining the price of residential land for compensation when the State recovers land according to current Vietnamese law - 2 -

Training and Professional Development of Land Price Management Team

Training and Professional Development of Land Price Management Team -

Situation of Information Technology Application in Enterprises

Situation of Information Technology Application in Enterprises -

Perspectives on Improving the Quality of Law Application in Resolving Land Use Rights Disputes at the People's Court

Perspectives on Improving the Quality of Law Application in Resolving Land Use Rights Disputes at the People's Court -

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1

1.3.3. Used to determine the reference price of stocks and to determine the price of stock purchase rights (or warrant purchase fees) in case of issuing additional shares to increase capital.

Example 37: Let's value the option of Haphaco shares in the recent additional share issuance according to the data in Example 23. The total newly mobilized capital is 20 billion VND (the total legal capital of Haphaco before issuing the right to buy shares is 10 billion VND. Haphaco issues the warrant first. The reference price of this stock before the issuance is 50,000 VND/share (PR t-1 ). The capital increase ratio is 2 times the existing capital (I=1). The price of the stock to be sold to shareholders recorded in the right is 32,000 VND/share (PR). Then the reference price of this stock on the ex-rights trading day (PR t ) according to formula (1.9) is calculated as

PR t-1+ (I x PR ) PR t= ------------------------

1+ I

In which: PR tis the stock reference price after issuing warrants; This price is the price that needs to be determined.

PR t-1is the stock price before the warrant is issued.

I is the capital growth rate

PR is the price at which the stock will be sold to the warrant holder.

5 0 000 + 1 x 32000-0

PR t= -----------------------------= 41,000 VND

1+1

Thus, the value of shares after issuing rights is worth 41,000 VND.

This is the reference price of this stock on the trading day without the right to buy the stock, while the price with the right of the stock (or the strike price)

fixed) is 32,000 VND.

In this case, the price of the stock option is: 41,000-32,000 VND = 9,000 VND .

This is very important information in the process of trading this stock option.

This problem is encountered quite often in the operation of the stock market. Because issuing more shares to mobilize investment capital for production development is the most important purpose of the stock market and businesses will maximize the capital mobilized by this method.

1.3.4. Application to determine the reference price of shares on the trading day without dividend and bonus shares.

As introduced in the previous sections, many listed companies will now distribute dividends and profits in shares. In essence, this is a new issuance and sale to existing shareholders. The right to "buy" shares is implicit in this activity and is considered as the person who has the right to use the bonus or dividend to buy new shares. The need for valuation has also appeared. We distinguish two types of activities here: Profit distribution, dividend distribution and additional share issuance activities occurring at the same time.

EXAMPLE 38-Khanh Hoi Import-Export Joint Stock Company (KHAHOMEX) has been permitted by the State SecuritiesCommission to issue additional shares to increase capital in the form of bonus shares, increasing charter capital from 20.9 billion to one and a half times, that is, issuing an additional 1,045,000 shares with a value of 10.450 billion. The last day for shareholders to register for the right to buy shares is October 15, 2004 (Friday). The ex-rights trading day is Wednesday, October 13. The question here is what is the reference price of this share on October 13? What is the value of the right? Knowing that the share price on October 12 of KHA is 25,500 VND. (This is a real example with actual data of the Vietnamese stock market).

In this case, two events occur at the same time: KHA Company issues a bonus and KHA Company issues additional shares to increase capital. The bonus is 5000 VND/share; Issue to increase capital by 50% and sell to the right holder (shares).

existing shareholders) at the price of 10,000 VND/share. Apply the formula introduced in chapter 1 - Formula (1.9) with adjustment for the discount due to bonus:

PR t-1+ (I x PR )-TTH PR t= ------------------------------

1+ I

In which: PR tis the stock reference price after issuing warrants; This price is the price that needs to be determined.

PR t-1is the stock price before issuing warrants. (25,500 VND) I is the capital increase ratio. : 50%=0.5

PR is the price of the stock to be sold to the warrant holder (10,000 VND)

Bonus TTH (5000 VND)

25500 + (0.5x 10000 ) –5000

PR 13/10= -------------------- -------- --------- = 17,000 VND 1+ 0.5

That is, if on October 13, the KHA stock price is 17,000 VND/share, then

is considered to have no price fluctuations, no impact on the Vn-Index.

The price reduction from 25,500 VND/share to 17,000 VND/share is just a change in value, not a change in price.

The price of the right here is 17,000 VND - 10,000 VND = 7,000 VND

It is very regrettable that the Ho Chi Minh City Securities Trading Center calculated and announced the incorrect reference price of this stock on October 12 with a reference price of 20,300 VND. If this price had been announced, the cash bonus would have been omitted. This result has deceived investors because the price of this stock cannot be as high as 20,300 VND but only at 17,000 VND according to published documents and market practice.

EXAMPLE : Haphaco Company has been permitted by the State Securities Commission to pay the second dividend in shares (1,200 VND/share), with the price calculated at par value, 10,000 VND/share, meaning that shareholders with 100 shares will receive 12 more shares.

At the same time, bonus shares to shareholders to increase capital at a ratio of 2:1, meaning that two old shares will receive 1 new share. The ex-rights trading date is December 6, 2004. Let's calculate the reference price of this share on December 6, 2004 according to the formula:

PR t-1+ (I x PR )-TTH- PR dividend t= -------------------------------------

1+ I

In which: PR tis the stock reference price after issuing warrants; This price is the price that needs to be determined.

PR t-1is the stock price before the warrant is issued. (Price on December 3, 2004 was 39,300 VND)

I is the capital increase ratio. : 50%+12%=0.62

PR is the price of the stock to be sold to the warrant holder (10,000 VND)

Bonus (5000 VND) Dividend = 1200 VND

39300 + (0.62x 10000 ) –5000-1200

PR 6/12= -------------------- -------- --------- = 24259 VND

1+ 0.5

In this case, the value of the right to receive dividends and bonuses in shares is:

39300 - 24259 = 15 041 ®

However, in reality, the Ho Chi Minh City Stock Exchange has set the reference price of Haphaco in the first trading session without rights (December 6, 2004) at VND 25,000 (700 VND higher than the actual value).

This is another mistake in calculating stock value in the market.

cash bonus and dividend payment to increase capital. Haphaco's reference price on December 6, 2004 - Trading session 931 should have been announced at 24,300 instead of 25,000 VND.

This is very important information for investors so that they have a basis to trade this stock before December 6.

The decrease in Haphaco's price from 39,300 in the 930th trading session to 24,300 in the 931st session is not considered a decrease and is not included in the Vn Index, because this is a decrease in the value of the stock, not a decrease in price.

1.3.5. Application in determining the strategy of buying a call option (bought call)

EXAMPLE 39 :Take the example in section 1.e above and simplify it:

Suppose a Vietnamese company signs a contract to buy a call option for 100,000 USD with the following information:

+ Option exchange rate: VND/US = 15000

+ Spot exchange rate: VND/US = 14850

+ Option fee: 15 million VND

+ 3-month VND interest rate is 8% per year

+ 3-month USD interest rate is 2.58%/year

+ Contract term is 3 months

a) Option fee is understood according to the following options:

Option 1: %VND/USD format

(15 million VND/(100 000USDx15 000VND)x100 = 1%

Option 2: USD/VND format (usually called points)

(15 000 000/14 850)/(100 000x15 000)x1 000 000 VND =0.6733$/1 million VND

Option 3: VND/USD (Also commonly called point form) (15,000,000/100,000) = 150 VND/1USD

Option 4: %USD/US$ format

(15 000 000/14 850):100 000x100 = 1.01%

b) Option premium in VND according to the Boston-Style Option model. 15,000,000x (1+ 0.08/4) = 15,300,000 VND

c) Exchange rate F(VND/USD) 3 months according to market parameters:

1485 x (1 0.08 )

F(VND/USD) = (FV VND /FV USD ) =

4 15050

1 x (1 0.0258 )

4

The fee in VND to buy 1 USD after 3 months is:

150x (1 0.08 x 3) 153 VND / USSD

12

Let's represent the cost of buying 1 USD according to the exchange rate fluctuations.

Figure 16:

Cost in VND to buy 1$

15153

thanks for the right to exchange rate

click to buy 1USD

15050

Option Line

Term Line

- If the exchange rate

right now

14897

15000

g linh h

after 3 months

VND/USD spot exchange rate after 3 months

yes

following items:

The option is exercised and paid for by

15000+153=15153®

- If the spot exchange rate after 3 months is less than the option rate (<15,000 VND), the option is not exercised and the option holder will buy US$ on the spot market at a cost of: Spot rate +153 VND

- The cost of buying USD under a forward contract does not depend on the spot exchange rate, so the forward line is horizontal at 15,050 VND.

- The forward contract and the option contract have equal costs when the spot rate after 3 months is the same:

15050®-153=14897®

The payoff of a call option buyer is represented by the following diagram:

Figure 17-Option buyer's income

Income in VND

Spot-15153

15000

-153

15153

Spot exchange rate VND/USD

- When the spot rate is less than 15000, the buyer of the option loses 153 VND. In this case, the option will not be exercised.

- When the spot rate is between 15,000 VND and 15,153 VND, the option buyer still loses, but the loss is less than 153 VND - Provided that the option is exercised to minimize the loss.

- When the spot rate is exactly 15153, the option buyer breaks even (the option still has to be exercised)

- When the spot rate is greater than 15153, the option buyer wins and the profit is equal to the Spot rate – 15153

1.3.6. Application in determining put option buying strategy

Let's look at the possibility of applying hedging and forex trading through the put option strategy:

EXAMPLE 40 : Company X signs a contract to buy a put option on AUD to receive USD under the following conditions:

- Contract value 10 million AUD

- USD/AUD option rate is 0.8

- The USD/AUD spot rate is 0.8050

- Option fee is 300,000AUD or 241,500USD

- AUD 3-month term interest rate is 12%/year

- The 3-month USD interest rate is 4.64% per year

- Contract term is 3 months

a) Boston Style Option USD Put Option Fee:

241500 x (1 0.0464 ) 244300 USD

4

b) The 3-month forward rate F(USD/AUD) is determined as follows:

0.8050 x (1 0.0464 x 3)

F(USD/AUD) = (FV USD /FV AUD ) =

12 0.7906

1 x (1 0.12 x 3)

12

c) Figure 18 : Benefits of selling 1 AUD.

Collect in USD when selling 1 AUD

0.7906

0.7755

Term Line

Spot rate USD/AUD

0.8 0.8151

- The vertical axis shows the amount of revenue in USD when selling 1 AUD

- The horizontal axis shows the possible 3-month spot exchange rate between USD and AUD

- Option premium expressed in USD/AUD points: 241500/10 000 000 = 0.0242 USD/AUD = 242 points

and at 3 months:

0.0242 x (1 0.0464 ) 0.0245 USD / AUD

4

- If the spot rate has not exceeded 0.8 USD, the put option will

exercised (because the put option is more profitable) and if 1 AUD is sold, the put option seller will collect:

0.8-0.0245 =0.7755 USD

- If the spot rate is greater than 0.8, the seller will not exercise the right because they can exercise it in the spot market because selling here will earn more money. The net profit from selling 1 AUD is

Spot price – 0.0245USD fee

- The option and forward contracts have equal costs and are equal to the forward value at the spot rate in three months and are equal to:

0.7906+0.0245 = 0.8151 USD/1AUD

1.3.7. Application in determining put option selling strategy

EXAMPLE 41:A Vietnamese company sells a put option to a Bank with the following conditions:

- Contract value: 100,000 USD

- Option exchange rate (strike rate) is 15500VND/1USD

- Spot exchange rate upon signing the contract is 15420 VND/USD

- Option fee is 2000USD or 30840000VND

- The 3-month USD interest rate is 5.72% per year

- 3-month VND interest rate is 8.64% per year

- Contract term t= 3 months

a) Boston Style Option premium:

- In USD: This is the fee payable when the contract expires. 2000x(1+0.0572/4)= 2028.6USD

- In VND:

30840000x(1+ 0.0864/4) = 31506144VND

b) Buyer's fee to buy 1USD at present and after 3 months:

- At present: 30,084,000 : 100,000 = 308.4VND/USD