Every day, based on the documents that have been checked, the accountant will enter data and account for the documents accurately according to the tables set up in the accounting software. According to the software process, the information will be automatically entered into the related books such as: general journal, detailed accounting card book, ledger by account,... After entering the documents, they will be saved in the accounting department as original documents.

At the end of the period, the accountant performs closing operations to create a balance sheet of arising numbers and financial reports. The checking and comparison of data recorded in the general ledger and the detailed summary table (created from detailed accounting books and cards) is automatically performed by the software on the principle of accuracy and honesty.

The accountant prints out the documents and books from the software onto paper, checks and compares them again, then sends them to the chief accountant or director for checking, signing, approval and preservation.

Accounting documents

Diary

special

Accounting books and cards

detail

GENERAL LOG

Diagram 2.3: Sequence of recording in general journal accounting form.

LEDGER

Detailed summary table

Balance sheet of arising numbers

FINANCIAL REPORT

Computerized.

Computerized.

Note:

Daily Record.

Recorded at the end of the month or periodically. Reconciliation and checking.

(Source: Accounting Department of Hoang An Private Enterprise)

2.1.4.4.5. Financial reporting system.

Balance sheet.

Business performance report.

Cash flow statement.

Financial statement explanation.

2.1.5. Current business performance of Hoang An Private Enterprise.

Graduation thesis

36

Supervisor: MSc. Ngo Thi My Thuy

Table 2.3: Business performance of Hoang An Private Enterprise in 2011 - 2013

Unit: Dong

Target

2011 | 2012 | 2013 | Year 2012/2011 | Year 2013/2012 | |||

Value | Percentage | Value | Percentage | ||||

1. Revenue from insurance and services. | 27,847,264,316 | 25,505,088,808 | 24,926,680,655 | (2,342,175,508) | (8.41) | (578,408,153) | (2.27) |

2. Revenue deductions | |||||||

3. Net revenue from insurance and services. | 27,847,264,316 | 25,505,088,808 | 24,926,680,655 | (2,342,175,508) | (8.41) | (578,408,153) | (2.27) |

4. Cost of goods sold. | 18,431,937,099 | 17.119.003.213 | 16,276,121,788 | (1,312,933,886) | (7.12) | (842,881,425) | (4.92) |

5. Gross profit on insurance and services. | 9,415,327,217 | 8,386,085,595 | 8,650,558,867 | (1,029,241,622) | (10.93) | 264,473,272 | 3.15 |

6. Financial operating revenue. | 2,169,432 | 1,385,296 | 1,001,181 | (784,136) | (36.14) | (384,115) | (27.73) |

7. Financial costs. | 371,280,554 | 280,764,166 | 432,767,265 | (90,516,388) | (24.38) | 152,003,099 | 54.14 |

- Including: interest expense | 371,280,554 | 280,764,166 | 432,767,265 | (90,516,388) | (24.38) | 152,003,099 | 54.14 |

8. Selling expenses. | 6,584,229,297 | 5.103.876.033 | 5,112,093,985 | (1,480,353,264) | (22.48) | 8,217,952 | 0.16 |

9. Business management costs. | 2,522,764,622 | 2,670,657,896 | 2,684,156,340 | 147,893,274 | 5.86 | 13,498,444 | 0.51 |

10. Net profit from operating activities. | (60,777,824) | 332,172,796 | 422,542,458 | 392,950,620 | (646.54) | 90,396,662 | 27.21 |

11. Other income. | 196,114,000 | 209.090.909 | 1,268,181,820 | 12,976,909 | 6.62 | 1,059,090,911 | 506.52 |

12. Other costs. | 438,236,297 | 1,661,110,283 | 438,236,297 | 1,222,873,986 | 279.04 | ||

13. Other profits. | 196,114,000 | (229,145,388) | (392,928,463) | (425,259,388) | (216.84) | (163,783,075) | 71.48 |

14. Total accounting profit before tax | 135,336,176 | 103,027,408 | 29,613,995 | (32,308,768) | (23.87) | (73,413,413) | (71.26) |

15. Current corporate income tax expense. | 23,683,831 | 18,029,797 | 7,403,499 | (5,654,034) | (23.87) | (10,626,298) | (58.94) |

16. Deferred corporate income tax expense. | |||||||

17. Profit after corporate income tax. | 111,652,345 | 84,997,611 | 22,210,496 | (26,654,734) | (23.87) | (62,787,115) | (73.87) |

18. Basic earnings per share | |||||||

Maybe you are interested!

-

Sequence Diagram of Recording Revenue, Expenses and Determining Business Results in the General Journal Accounting Form

Sequence Diagram of Recording Revenue, Expenses and Determining Business Results in the General Journal Accounting Form -

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1 -

Completing revenue accounting and determining business results at Ha Lam Coal Joint Stock Company - Vinacomin - 16

Completing revenue accounting and determining business results at Ha Lam Coal Joint Stock Company - Vinacomin - 16 -

Completing revenue and cost accounting and determining business results at Nakashima Vietnam Co., Ltd. - 14

Completing revenue and cost accounting and determining business results at Nakashima Vietnam Co., Ltd. - 14 -

Accounting for revenue, expenses and determining business results at Saigon Real Estate Joint Stock Company - 1

Accounting for revenue, expenses and determining business results at Saigon Real Estate Joint Stock Company - 1

(Source: Business performance report of Hoang An Private Enterprise in 2011 - 2013)

SVTH: Dinh Thi Thuy Tien

CLASS: 10DKNH01

Comment :

Net revenue from sales and service provision of the enterprise has decreased gradually over the years: in 2012, it decreased by 8.41% compared to 2011, corresponding to a decrease of 2,342,175,508 VND. In 2013, it decreased by 2.27% compared to 2012, corresponding to a decrease of 578,408,153 VND. The main reason for the decrease is that in 2012 - 2013, there were fewer orders than in 2011 , which is a sign that the consumption and production activities of the enterprise are not developing well, and the sales policy is not really effective.

Total profit after tax of the enterprise: in 2012 compared to 2011 decreased by 23.87%, or 26,654,734 VND, especially in 2013 compared to 2012 decreased by 73.87%, or 62,787,115 VND. Because in 2013 compared to 2012, the cost increased gradually, specifically:

Selling expenses increased by 0.16%.

Business management costs increased by 0.51%.

Financial expenses increased by 54.14% mainly due to short-term interest expenses.

Other expenses increased by 279.04% due to liquidation of many fixed assets in 2013.

This shows that in 2013, businesses could not control costs, the increase in costs caused profits to decrease.

Conclude :

In general, Hoang An Private Enterprise has been doing business for three years from 2011 to 2013, the revenue is quite high, the cost is relatively large to earn this revenue but still makes a profit (although the profit is not very high and has decreased over the years).

However, businesses need to have appropriate cost control measures, adjust sales policies, etc. to increase business profits and promote further business development.

2.1.6. Advantages and disadvantages.

2.1.6.1. Advantages.

The company has a team of experienced, highly qualified, dynamic employees who regularly update and apply science and technology to their work.

The system of machinery, equipment and vehicles is invested in and purchased according to new technology to ensure control, prevent errors, improve product quality and satisfy customers.

2.1.6.2. Difficulty.

Besides the advantages, businesses also face many difficulties such as: Competition from other businesses in the same industry.

Sometimes the market economy is unstable, gas prices increase and labor costs increase simultaneously, causing other costs to increase, causing businesses to face many difficulties.

Equity is small compared to the size and growth rate of the business.

2.2. CURRENT SITUATION OF REVENUE AND EXPENSE ACCOUNTING AND DETERMINATION OF BUSINESS RESULTS AT HOANG AN PRIVATE ENTERPRISE.

2.2.1. Business characteristics, consumption methods, payment, and document circulation procedures in sales operations at Hoang An Private Enterprise.

2.2.1.1. Business characteristics.

Hoang An Private Enterprise is a business specializing in distributing and selling gas products, providing specialized tank truck transportation services for other businesses.

Consumption market: mainly domestic market.

Sales policy: customers are always the top concern, satisfying customer needs through providing the best products and services.

2.2.1.2. Sales method.

Businesses use other sales methods such as wholesale, retail, and agency sales, but mainly wholesale (selling through warehouses).

Regarding the form of delivery, the buyer can come to receive it directly at the company's warehouse or according to the agreement in the signed contract.

2.2.1.3. Payment method.

Cash payment: for orders with value under 20,000,000 VND, or retail customers. When receiving all goods and payment documents, customers will have to pay for the goods through the sales staff or cashier of the business.

Payment by bank transfer: this method is mainly applied to orders with a value of over 20,000,000 VND or to large customers, specifically wholesale purchases as follows:

New customers: pay 100% of contract value before delivery and issue VAT invoice.

Customers who are cooperating: deposit 30% to 50% of the contract value before delivery. The remaining amount will be paid within 10 days at the latest when the customer has received all the goods and payment documents.

Loyal customers: delivery in advance and customers will pay 100% of the value of the goods upon receipt of full goods and payment documents, within 10 days at the latest.

2.2.1.4. Order of document circulation in sales transactions.

The sales department receiving customer orders will coordinate with the warehouse department to check the actual situation of quality, quantity, and type of goods in stock, and coordinate with the accounting department to check the customer's outstanding balance.

If the order is accepted, the price, delivery method, etc. will be agreed upon and the economic contract will be signed. Normally, the director will authorize the sales department to draft the economic contract, except in some important cases or cases with complicated conditions of agreement, in which case the director's opinion is required. The economic contract signed consists of four copies, each party keeps two copies.

Based on the economic contract, the sales department creates a sales request form and sends it to the warehouse department requesting the creation of a warehouse delivery form consisting of three copies: copy 1 is kept at the end of the day and recorded on the warehouse card, copy 2 is sent to the accounting department, and copy 3 is sent to the delivery department.

The accounting department receives the economic contract and the warehouse delivery note (copy 2) and will create a delivery note and a two-copy VAT invoice: copy 1 is kept in the accounting department, copy 2 and the delivery note are transferred to the warehouse department.

The warehouse and delivery department will pack and deliver the goods along with the VAT invoice copy 2 to the customer and collect the money, the warehouse keeper and the customer will sign the delivery note and then transfer it to the accounting department. After receiving the documents, the accountant will check and classify them and record them in the accounting books such as detailed books, general journals, and general ledgers.

2.2.2. Accounting for revenue and other income.

2.2.2.1. Accounting for sales revenue and service provision.

2.2.2.1.1. Content.

Sales revenue is the amount of money Hoang An Private Enterprise receives or will receive from economic activities such as: distribution and supply of liquefied petroleum gas, gas, gas stoves.

Revenue from providing services mainly comes from specialized tanker transportation services for other gas businesses to the provinces of Da Lat, Dak Lak, Phan Rang, Phan Thiet, Nha Trang.

In general, Hoang An Private Enterprise's revenue comes from two sources: revenue from goods consumption and revenue from providing services, but mainly from goods consumption.

The time to record revenue from sales of goods and provision of services is when the customer has paid or accepted payment and the services and goods have been delivered to the customer.

2.2.2.1.2. User account.

Accountants use: Account 511 "Sales and service revenue" to track the business's sales and service revenue in an accounting period.

This 511 account has two sub-accounts:

Account 5111 “Revenue from sales of goods”.

Account 5113 “Revenue from providing services”.

2.2.2.1.3. Documents and books used.

- Document:

VAT invoice, economic contract.

Warehouse delivery note.

Payment documents: receipts, credit notes, etc.

- Books: Detailed account book 511, general journal, general ledger account 511

2.2.2.1.4. Recording sequence.

Based on revenue documents, accountants will classify services and goods and enter data into Accom Accounting software to record revenue and track debts. The software will reflect through detailed account book 511, general journal, general ledger account 511

Economic Contract, Purchase Order

VAT invoice,

Receipt,…

General journal

Ledger account 511

Detail book of account 5111, account 5113

Note : For debts, in addition to tracking debts in the software for each customer, accountants also track them separately using an excel file to compare with the software.

2.2.2.1.5. Some economic transactions arise.

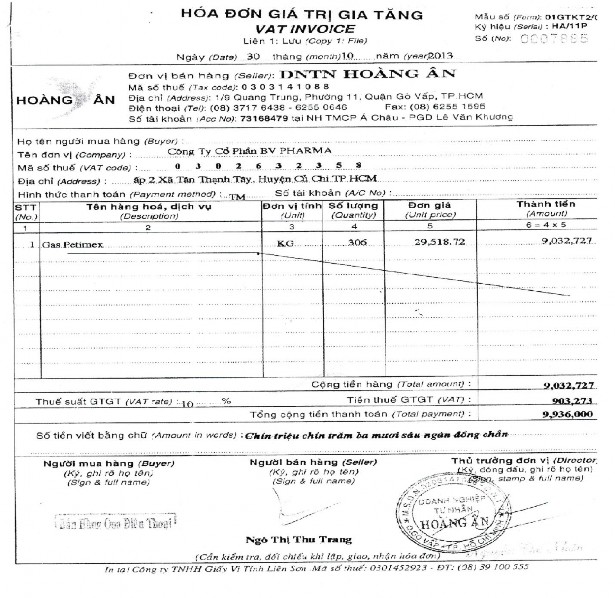

Transaction 1 : Based on VAT invoice No. 0007885 dated October 30, 2013, sold 306 kg of Petimex gas to BV Pharma Joint Stock Company, with a unit price of VND 29,518.72/kg, VAT rate is 10%, customer pays immediately in cash. Accountant records:

Debit account 111: 9,936,000 VND

Credit account 5111: 9,032,727 VND

Credit account 3331: 903,273 VND

Transaction 2 : Based on VAT invoice No. 0007898 dated October 31, 2013 of Hoang An Private Enterprise providing LPG transportation service in October 2013 for Cuu Long Petroleum Transportation Service Joint Stock Company, with pre-tax transportation fee of VND 161,812,727, VAT is 10%, the customer has not paid the enterprise. Accounting records:

Debit account 131: 177,994,000 VND

Credit account 5113: 161,812,727 VND

Credit account 3331: 16,181,273 VND

(Appendix attached to invoice number 0007898, symbol HA/11P)

Transaction 3 : Based on VAT invoice No. 0008173 dated November 29, 2013, sold 384 kg of Petimex liquefied petroleum gas to Truong Van Ngai school, unit price 30,539.77 VND/kg, VAT is 10%, customer paid immediately in cash. Accountant records:

Debit account 111: 12,900,000 VND

Credit account 5111: 11,727,273 VND

Credit account 3331: 1,172,727 VND

(Appendix attached to invoice number 0008173, symbol HA/11P)

Transaction 4 : Based on VAT invoice No. 0008179 dated November 30, 2013 of Hoang An Private Enterprise providing LPG transportation services to Cuu Long Petroleum Transportation Services Joint Stock Company, with pre-tax transportation fee of VND 120,065,455, VAT rate is 10%, the customer has not paid the enterprise. Accounting records:

Debit account 131: 132,072,000 VND

Credit account 5113: 120,065,455 VND

Credit account 3331: 12,006,545 VND

(Appendix attached to invoice number 0008179, symbol HA/11P)

Transaction 5 : Based on VAT invoice No. 0008453 dated December 31, 2013 of Hoang An Private Enterprise providing LPG transportation services to Van Loc Long An Vietnam LPG One Member Co., Ltd., with pre-tax transportation fee of VND 32,753,129, VAT is 10%, the customer has not paid the enterprise. Accounting records:

Debit account 131: 36,028,442 VND

Credit account 5113: 32,753,129 VND

Credit account 3331: 3,275,313 VND

(Appendix attached to invoice number 0008453, symbol HA/11P)

Transaction 6 : Based on VAT invoice No. 0008462 dated December 31, 2013, sold 144 kg of Petrolimex liquefied petroleum gas to Seafood Joint Stock Company No. 4, unit price 36,363.64 VND/kg, VAT is 10%, customer pays in cash. Accountant records:

Debit account 111: 5,760,000 VND

Credit account 5111: 5,236,364 VND

Credit account 3331: 523,636 VND

(Appendix attached to invoice number 0008462, symbol HA/11P)

In the fourth quarter, sales and service revenue was 7,598,593,392 VND.

Total revenue from sales of goods (account 5111) is 4,846,339,280 VND.

Total service revenue (account 5113) is 2,752,254,112 VND.

At the end of the fourth quarter, the accountant transfers net sales revenue and service revenue to account 911 to determine business results. The accountant records:

Debit account 511: 7,598,593,392 VND

Credit account 911: 7,598,593,392 VND

Illustrative book : ledger account 511

Illustrative book : ledger account 511

(Appendix includes detailed books of account 5111, account 5113 and general journal)

Hoang An Private Enterprise

1/9 Quang Trung, Ward 11, Go Vap District

LEDGER

Form No. S03b – DN

Issued under Decision No. 15/2006/QD-BTC dated March 20, 2006 of the Minister of Finance.

Quarter 4, 2013

Account Name: Sales and Service Revenue.

Serial Number: 511

Unit: Dong

Date of recording

Document | Interpretation | General Journal | TK corresponding | Number of occurrences | ||||

Number effect | Day | Page number | STT current | In debt | Have | |||

A | B | C | D | E | G | H | 1 | 2 |

Opening balance | ||||||||

……. | …….. | ……. | …….. | … | …….. | |||

October 30 | 7885 | October 30 | Sales contract 7885 | 111 | 9,032,727 | |||

October 31 | 7898 | October 31 | VC fee 7898 | 131 | 161,812,727 | |||

……. | …….. | ……. | …….. | … | …….. | |||

11/29 | 8173 | 11/29 | Sales contract 8173 | 111 | 11,727,273 | |||

11/30 | 8179 | 11/30 | Service fee 8179 | 131 | 120,065,455 | |||

……. | …….. | ……. | …….. | … | …….. | |||

12/31 | 8453 | 12/31 | VC fee contract 8453 | 131 | 32,753,129 | |||

12/31 | 8462 | 12/31 | Sales contract 8462 | 111 | 5,236,364 | |||

……. | …….. | ……. | …….. | … | …….. | |||

12/31 | Z2001 / 1213 | 12/31 | Revenue from insurance and CCDV Q4 | 911 | 7,598,593,392 | |||

Add | 7,598,593,392 | 7,598,593,392 | ||||||

Closing balance | ||||||||

- This book has….pages, numbered from page….to page….

- Date of opening the book: ………….

Date ….. Month ….. Year…..

Bookkeeper Chief Accountant Director

(Signature, full name) (Signature, full name) (Signature, full name, seal)

Nguyen Chi Cong Ngo Thi Thu Trang Nguyen The Nhan