Timely inform the People's Credit Fund where the loan is made about cases of risky loan use to have appropriate and timely handling measures.

- Urge the Management Board of the Savings and Credit Group to implement the authorization contract signed with the People's Credit Fund, direct and supervise the Management Board of the Savings and Credit Group in the following tasks:

Urge group members to bring money to the transaction point of the People's Credit Fund to repay the principal according to the agreed repayment plan.

Collect interest and savings (for Savings and Credit Groups authorized by the People's Credit Fund to collect) or urge group members to bring money to the People's Credit Fund's Transaction Point to pay interest and deposit savings periodically as agreed (for Savings and Credit Groups not authorized by the People's Credit Fund to collect).

Periodically every quarter, 6 months, year or suddenly (at the request of the bank), coordinate with the district-level Social Policy Bank to evaluate the activities of each Group to classify the Group according to criteria, weak Groups that are no longer able to operate will be merged or dissolved according to regulations.

- Direct, monitor and inspect the borrower's capital use process; inspect the activities of the Savings and Credit Groups and the lower-level social-economic organizations under the management scope periodically or suddenly. Coordinate with the Social Policy Bank and local authorities to handle cases of overdue debts and guide borrowers to prepare documents to request handling of debts at risk due to objective reasons.

- Periodically or suddenly inspect and monitor the implementation of preferential credit policies. Organize regular meetings, interim and final reviews to evaluate the results achieved, existing problems and difficulties; discuss measures and recommendations for handling due debts, overdue debts, risky debts, encroached debts and discuss directions and implementation plans in the coming time. Organize training on entrustment skills for officers of the Association, officers of the Savings and Credit Group. Coordinate with competent agencies to disseminate and propagate policies and guidelines related to preferential credit policies and provide training on agricultural, forestry and fishery extension work... to help borrowers use loans effectively.

The entrustment of social-political organizations to manage the activities of the Savings and Credit Groups according to residential areas combined with the activities of the Association has resulted in the high efficiency of the activities of the Savings and Credit Groups. Partial entrustment through social-political organizations has contributed positively to the expansion and improvement of the quality of policy credit. In 2003, there was only a program for lending to poor households with over 8,240 billion VND, in 2004, an additional program was added.

The NS&VSMT NT program with a total entrusted loan balance of 9,595 billion VND, by December 31, 2015, the entrusted loan balance reached 140,859 billion VND with 18/19 credit programs. The entrusted loan balance accounts for 99% of the total outstanding loan balance of the VBSP, in which the Women's Union accounts for the highest proportion of 39.4%, followed by the Farmers' Association with a proportion of 33%, the Veterans' Association 15.3% and the Ho Chi Minh Communist Youth Union 11.6%. The overdue debt entrusted through CT-XH organizations is only 425 billion VND, accounting for 0.3% of the total outstanding loan balance, a decrease of 59 billion VND compared to 2014 [16].

The method of entrusting through social-political organizations saves management costs compared to entrusting through the State Bank of Vietnam. The current entrustment fee through social-political organizations is 0.045%/month. If added with the commission fee paid to the Savings and Credit Groups of 0.1%/month, then currently both of these amounts are a maximum of 0.145%/month calculated on the actual interest collected, much lower than the fee paid to the State Bank of Vietnam of 0.22%/month [16].

Figure 2.1: Scale of outstanding loans entrusted through socio-political organizations

Unit: billion VND

150,000

120,000

90,000

60,000

30,000

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

0

Farmers' Association Women's Association

Veterans Association Youth Union

Source: Annual report of the People's Credit Fund

The method of entrustment through social organizations has done a good job of socializing the goal of hunger eradication and poverty reduction, creating transparency and accuracy in identifying policy beneficiaries, and limiting the occurrence of negative phenomena. The participation of social organizations in coordination with agricultural extension organizations has contributed to helping borrowers use loans effectively. Thanks to the implementation of entrustment, the activities of social organizations have also been strengthened.

However, this method of delegation also creates problems such as the form of concurrent holding of positions, causing the executor to undertake non-professional tasks.

In addition, the workload is high while the qualifications of the staff of the CT-XH organization as well as the information technology platform of the organization are not yet developed, causing professional work to sometimes take time and not achieve the highest efficiency.

Second, the activities of the TK&VV Group

According to the experience of some poor lending banks in the world, providing small loans to the poor often requires the establishment of community support groups in the lending relationship with the bank. This is almost a replacement for the form of loan guarantee according to traditional banking methods, which is guaranteed by the effective operation of the groups and mutual support groups. Immediately after its establishment, the Social Policy Bank received all capital, outstanding loans and the number of Savings and Credit Groups from the Bank for the Poor. Receiving capital and using the Savings and Credit Groups together with the experience of managing lending groups from the State Bank of Vietnam, the Social Policy Bank has reorganized the activities of the Savings and Credit Groups. The Board of Directors issued Decision No. 783/QD-HDQT on the regulations on the organization and operation of the Savings and Credit Groups with the following basic contents:

- The Savings and Credit Group is organized as a cooperative group consisting of members who are representatives of households with similar circumstances, needs and are eligible for loans, have a spirit of solidarity and mutual assistance, reside in the same residential area, voluntarily join the Group, and together commit to using the loan for the right purpose, paying interest on time, saving small amounts of money every month, creating a sense of saving and creating self-owned capital.

- Savings and Credit Groups are established and operate to create conditions for members to help each other in production, business and daily life, for the benefit of the poor and policy beneficiaries, helping them practice and get used to borrowing and repaying capital, taking appropriate steps in production, business and financial management.

- Savings and Credit Groups operate independently from social organizations. The People's Credit Fund can sign service contracts with Savings and Credit Groups. Savings and Credit Groups are not allowed to collect principal debts, but can be authorized to collect interest if they meet the conditions and have credibility. The activities of Savings and Credit Groups are paid a maximum service commission fee of 0.1% calculated on the actual interest collected by the People's Credit Fund. Savings and Credit Groups are instructed to open books, record and monitor loans, debt repayment results, and interest payments of each member of the Group.

- The People's Credit Fund delegates some tasks to social-political organizations, focusing on guiding the establishment, management and supervision of the organization's activities.

TK&VV, together with the Social Policy Bank, disseminates and propagates the State's credit policy to the community; supervises the selection of loan recipients at the Group, organizes training, coordinates with functional agencies to integrate agricultural and forestry extension programs, and guides business methods so that borrowers can use loans effectively.

- The Social Policy Bank manages lending and debt collection directly to borrowers in the commune, every month at the Commune Transaction Point on a fixed day, when the transaction is witnessed by the Head of the Savings and Credit Group. The bank organizes accounting and monitoring for each borrower, publicly implements credit policies and borrower lists, ensuring supervision by the commune-level government and the community.

- At the Transaction Point, the Social Policy Bank organizes meetings with entrusted social organizations and Savings and Credit Groups to promptly handle problems in the process of using loans, minimize possible risks, and organize training for social organizations and Savings and Credit Groups to implement regulations and assigned tasks.

The Savings and Credit Group network plays a very important role in the current loan management system of the Vietnam Bank for Social Policies. In the context of a newly established credit institution, lacking human resources, lacking technical facilities, and having little experience in credit management, the establishment of Savings and Credit Groups in villages and hamlets is an effective "rescue" solution to bring credit capital directly to the right beneficiaries in a timely manner nationwide.

In order to manage the Savings and Credit Groups to operate nationwide while the human resources of the VBSP are limited due to the need to reduce costs to implement preferential interest rates, there is no other way for customers to entrust the management of the activities of these units through the social-political organizations, taking advantage of the network of activities of the associations. It can be said that this credit management work is considered a very successful solution of the VBSP. In the period from 1995 to 2002, the activities of the Savings and Credit Groups achieved initial results but also encountered some difficulties such as not being widely deployed (because many poor people are not members of the Women's Union, Farmers' Union), the inspection and supervision mechanism is still limited... However, the new operating mechanism suitable to the practical situation has brought about positive results. As of December 30, 2014, the number of Savings and Credit Groups reached 196,606 groups with 6,877,467 poor households with outstanding debts. Most of the Savings and Credit Groups have been operating in an orderly and effective manner according to the orientation of the Vietnam Bank for Social Policies. Each group is responsible for managing members borrowing capital according to policy credit programs in the area (usually at least 3 credit programs). On average, each group manages 35 households borrowing capital with outstanding debts.

630 million VND/team. By the end of 2015, the number of Saving and Credit Teams had decreased to 192,599 teams, of which 83.8% were classified as good, 12.8% were classified as fair, 2.1% were classified as average and 1.3% were classified as poor [16].

Regarding the relationship between entrusted social organizations and the Savings and Credit Groups, the entrusted associations encourage poor households, near-poor households and other policy beneficiaries to join the Savings and Credit Groups, practice savings, support each other in production and life, repay debts to the Social Policy Bank on time, and bring benefits to the members and the community. The Savings and Credit Groups are responsible for coordinating with the associations in linking the activities of the Group with the activities of the social organizations. The entrusted associations are also responsible for monitoring the activities of the Savings and Credit Groups to ensure compliance with the Regulations and the documents guiding the entrusted operations of the Social Policy Bank, and at the same time coordinate with the Bank to organize training to improve the management skills of the Group Management Board.

Table 2.5: Size of Savings and Loan Groups, number of households with outstanding debt, outstanding debt and overdue debt ratio at social organizations in 2015

Number of TK&VV Teams is active | Number of households currently outstanding | Outstanding debt | Debt ratio overdue | |

Farmers Association | 63,271 | 2,252,556 | 46,390,053 | 0.32% |

Women's Association | 73,786 | 2,700,396 | 56,198,645 | 0.26% |

Veterans Association | 32,071 | 1,055,656 | 21,844,766 | 0.32% |

Youth Union | 23,471 | 803,092 | 16,425,473 | 0.38% |

Maybe you are interested!

-

Outstanding Debt Situation of Bidv Trang An in the Period 2016 - 2020

Outstanding Debt Situation of Bidv Trang An in the Period 2016 - 2020 -

Medium and Long-Term Credit Structure on Total Outstanding Debt in the 2009-2011 Period

Medium and Long-Term Credit Structure on Total Outstanding Debt in the 2009-2011 Period -

Outstanding Debt and Proportion of Outstanding Debt for Personal Loans at Joint Stock Commercial Bank for Foreign Trade of Vietnam - Thanh Xuan Branch

Outstanding Debt and Proportion of Outstanding Debt for Personal Loans at Joint Stock Commercial Bank for Foreign Trade of Vietnam - Thanh Xuan Branch -

Outstanding Debt Situation by Economic Sector Over 3 Years 2006 - 2008

Outstanding Debt Situation by Economic Sector Over 3 Years 2006 - 2008 -

Identify Rating Levels and Rating Scales

zt2i3t4l5ee

zt2a3gstourism,quan lan,quang ninh,ecology,ecotourism,minh chau,van don,geography,geographical basis,tourism development,science

zt2a3ge

zc2o3n4t5e6n7ts

of the islanders. Therefore, this indicator will be divided into two sub-indicators:

a1. Natural tourism attractiveness a2. Cultural tourism attractiveness

b. Tourist capacity

The two island communes in Quan Lan have different capacities to receive tourists. Minh Chau Commune is home to many standard hotels and resorts, attracting high-income domestic and international tourists. Meanwhile, Quan Lan Commune has many motels mainly built and operated by local people, so the scale and quality are not high, and will be suitable for ordinary tourists such as students.

c. Time of exploitation of Quan Lan Island Commune:

Quan Lan tourism is seasonal due to weather and climate conditions and festivals only take place on certain days of the year, specifically in spring. In Quan Lan commune, the period from April to June and from September to November is considered the best time to visit Quan Lan because the cultural tourism activities are mainly associated with festivals taking place during this time.

Minh Chau island commune:

Tourism exploitation time is all year round, because this is a place with a number of tourist attractions with diverse ecosystems such as Bai Tu Long National Park Research Center, Tram forest, Turtle Laying Beach, so besides coming to the beach for tourism and vacation in the summer, Minh Chau will attract research groups to come for tourism combined with research at other times of the year.

d. Sustainability

The sustainability of ecotourism sites in Quan Lan and Minh Chau communes depends on the sensitivity of the ecosystems to climate changes.

landscape. In general, these tourist destinations have a fairly high level of sustainability, because they are natural ecosystems, planned and protected. However, if a large number of tourists gather at certain times, it can exceed the carrying capacity and affect the sustainability of the environment (polluted beaches, damaged trees, animals moving away from their habitats, etc.), then the sustainability of the above ecosystems (natural ecosystems, human ecosystems) will also be affected and become less sustainable.

e. Location and accessibility

Both island communes have ports to take tourists to visit from Van Don wharf:

- Quan Lan – Van Don traffic route:

Phuc Thinh – Viet Anh high-speed boat and Quang Minh high-speed boat, depart at 8am and 2pm from Van Don to Quan Lan, and at 7am and 1pm from Quan Lan to Van Don. There are also wooden boats departing at 7am and 1pm.

- Van Don - Minh Chau traffic route:

Chung Huong high-speed train, Minh Chau train, morning 7:30 and afternoon 13:30 from Van Don to Minh Chau, morning 6:30 and afternoon 13:00 from Minh Chau to Van Don.

f. Infrastructure

Despite receiving investment attention, the issue of infrastructure and technical facilities for tourism on Quan Lan Island is still an issue that needs to be resolved because it has a direct impact on the implementation of ecotourism activities. The minimum conditions for serving tourists such as accommodation, electricity, water, communication, especially medical services, and security work need to be given top priority. Ecotourism spots in Minh Chau commune are assessed to have better infrastructure and technical facilities for tourism because there are quite complete and synchronous conditions for serving tourists, meeting many needs of domestic and foreign tourists.

3.2.1.4. Determine assessment levels and assessment scales

Corresponding to the levels of each criterion, the index is the score of those levels in the order of 4, 3, 2, 1 decreasing according to the standard of each level: very attractive (4), attractive (3), average (2), less attractive (1).

3.2.1.5. Determining the coefficients of the criteria

For the assessment of DLST in the two communes of Quan Lan and Minh Chau islands, the students added evaluation coefficients to show the importance of the criteria and indicators as follows:

Coefficient 3 with criteria: Attractiveness, Exploitation time. These are the 2 most important criteria for attracting tourists to tourism in general and eco-tourism in particular, so they have the highest coefficient.

Coefficient 2 with criteria: Capacity, Infrastructure, Location and accessibility . Because the assessment area is an island commune of Van Don district, the above criteria are selected by the author with appropriate coefficients at the average level.

Coefficient 1 with criteria: Sustainability. Quan Lan has natural and human-made ecotourism sites, with high biodiversity and little impact from local human factors. Most of the ecotourism sites are still wild, so they are highly sustainable.

3.2.1.6. Results of DLST assessment on Quan Lan island

a. Assessment of the potential for natural tourism development

For Minh Chau commune:

+ Natural tourism attractiveness is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined as average (2 points) and the coefficient is quite important (coefficient 2), then the score of Capacity criterion is 2 x 2 = 4.

+ Exploitation time is long (4 points), the most important coefficient (coefficient 3) so the score of the Exploitation time criterion is 4 x 3 = 12.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is assessed as good (3 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 3 x 2 = 6 points.

The total score for evaluating DLST in Minh Chau commune according to 6 evaluation criteria is determined as: 12 + 4 + 12 + 4 + 4 + 6 = 42 points

Similar assessment for Quan Lan commune, we have the following table:

Table 3.3: Assessment of the potential for natural ecotourism development in Quan Lan and Minh Chau communes

Attractiveness of self-tourismof course

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

CommuneMinh Chau

12

12

4

8

12

12

4

4

4

8

6

8

42/52

Quan CommuneLan

6

12

6

8

9

12

4

4

4

8

4

8

33/52

b. Assessment of the potential for humanistic tourism development

For Quan Lan commune:

+ The attractiveness of human tourism is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined to be large (3 points) and the coefficient is quite important (coefficient 2), then the score of the Capacity criterion is 3 x 2 = 6.

+ Mining time is average (3 points), the most important coefficient (coefficient 3) so the score of the Mining time criterion is 3 x 3 = 9.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points.

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is rated as average (2 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 2 x 2 = 4 points.

The total score for evaluating DLST in Quan Lan commune according to 6 evaluation criteria is determined as: 12 + 6 + 6 + 4 + 4 + 4 = 36 points.

Similar assessment with Minh Chau commune we have the following table:

Table 3.4: Assessment of the potential for developing humanistic eco-tourism in Quan Lan and Minh Chau communes

Attractiveness of human tourismliterature

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Quan CommuneLan

12

12

6

8

9

12

4

4

4

8

4

8

39/52

Minh CommuneChau

6

12

4

8

12

12

4

4

4

8

6

8

36/52

Basically, both Minh Chau and Quan Lan localities have quite favorable conditions for developing ecotourism. However, Quan Lan commune has more advantages to develop ecotourism in a humanistic direction, because this is an area with many famous historical relics such as Quan Lan Communal House, Quan Lan Pagoda, Temple worshiping the hero Tran Khanh Du, ... along with local festivals held annually such as the wind praying ceremony (March 15), Quan Lan festival (June 10-19); due to its location near the port and long exploitation time, the beaches in Quan Lan commune (especially Quan Lan beach) are no longer hygienic and clean to ensure the needs of tourists coming to relax and swim; this is also an area with many beautiful landscapes such as Got Beo wind pass, Ong Phong head, Voi Voi cave, but the ability to access these places is still very limited (dirt hill road, lots of gravel and rocks), especially during rainy and windy times; In addition, other natural resources such as mangrove forests and sea worms have not been really exploited for tourism purposes and ecotourism development. On the contrary, Minh Chau commune has more advantages in developing ecotourism in the direction of natural tourism, this is an area with diverse ecosystems such as at Rua De Beach, Bai Tu Long National Park Conservation Center...; Minh Chau beach is highly appreciated for its natural beauty and cleanliness, ranked in the top ten most beautiful beaches in Vietnam; Minh Chau commune is also home to Tram forest with a large area and a purity of up to 90%, suitable for building bridges through the forest (a very effective type of natural ecotourism currently applied by many countries) for tourists to sightsee, as well as for the purpose of studying and researching.

Figure 3.1: Thenmala Forest Bridge (India) Source: https://www.thenmalaecotourism.com/(August 21, 2019)

3.2.2. Using SWOT matrix to evaluate Quan Lan island tourism

General assessment of current tourism activities of Quan Lan island is shown through the following SWOT matrix:

Table 3.5: SWOT matrix evaluating tourism activities on Quan Lan island

Internal agent

Strengths- There is a lot of potential for tourism development, especially natural ecotourism and humanistic ecotourism.- The unskilled labor force is relatively abundant.- resource environmentunpolluted, still

Weaknesses- Poorly developed infrastructure, especially traffic routes to tourist destinations on the island.- The team of professional staff is still weak.- Tourism products in general

quite wild, originalintact

general and DLST in particularalone is monotonous.

External agents

Opportunity- Tourism is a key industry in the socio-economic development strategy of the province and Van Don economic zone.- Quan Lan was selected as a pilot area for eco-tourism development within the framework of the green growth project between Quang Ninh province and the Japanese organization JICA.- The flow of tourists and especially ecotourism in the world tends toincreasing

Challenge- Weather and climate change abnormally.- Competition in tourism products is increasingly fierce, especially with other localities in the province such as Ha Long, Mong Cai...- Awareness of tourists, especially domestic tourists, about ecotourism and nature conservation is not high.

Through summary analysis using SWOT matrix we see that:

To exploit strengths and take advantage of opportunities, it is necessary to:

- Diversify products and service types (build more tourism routes aimed at specific needs of tourists: experiential tourism immersed in nature, spiritual cultural tourism...)

- Effective exploitation of resources and differentiated products (natural resources and human resources)

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s3 { color: #0D0D0D; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -3pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -2pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -1pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s10 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s12 { color: black; font-family:Symbol, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s13 { color: black; font-family:Wingdings; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s14 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s16 { color: black; font-family:Cambria, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s17 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s18 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s19 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s20 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; } div.maincontent .s21 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 11pt; } div.maincontent .s22 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s23 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s24 { color: #212121; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Identify Rating Levels and Rating Scales

zt2i3t4l5ee

zt2a3gstourism,quan lan,quang ninh,ecology,ecotourism,minh chau,van don,geography,geographical basis,tourism development,science

zt2a3ge

zc2o3n4t5e6n7ts

of the islanders. Therefore, this indicator will be divided into two sub-indicators:

a1. Natural tourism attractiveness a2. Cultural tourism attractiveness

b. Tourist capacity

The two island communes in Quan Lan have different capacities to receive tourists. Minh Chau Commune is home to many standard hotels and resorts, attracting high-income domestic and international tourists. Meanwhile, Quan Lan Commune has many motels mainly built and operated by local people, so the scale and quality are not high, and will be suitable for ordinary tourists such as students.

c. Time of exploitation of Quan Lan Island Commune:

Quan Lan tourism is seasonal due to weather and climate conditions and festivals only take place on certain days of the year, specifically in spring. In Quan Lan commune, the period from April to June and from September to November is considered the best time to visit Quan Lan because the cultural tourism activities are mainly associated with festivals taking place during this time.

Minh Chau island commune:

Tourism exploitation time is all year round, because this is a place with a number of tourist attractions with diverse ecosystems such as Bai Tu Long National Park Research Center, Tram forest, Turtle Laying Beach, so besides coming to the beach for tourism and vacation in the summer, Minh Chau will attract research groups to come for tourism combined with research at other times of the year.

d. Sustainability

The sustainability of ecotourism sites in Quan Lan and Minh Chau communes depends on the sensitivity of the ecosystems to climate changes.

landscape. In general, these tourist destinations have a fairly high level of sustainability, because they are natural ecosystems, planned and protected. However, if a large number of tourists gather at certain times, it can exceed the carrying capacity and affect the sustainability of the environment (polluted beaches, damaged trees, animals moving away from their habitats, etc.), then the sustainability of the above ecosystems (natural ecosystems, human ecosystems) will also be affected and become less sustainable.

e. Location and accessibility

Both island communes have ports to take tourists to visit from Van Don wharf:

- Quan Lan – Van Don traffic route:

Phuc Thinh – Viet Anh high-speed boat and Quang Minh high-speed boat, depart at 8am and 2pm from Van Don to Quan Lan, and at 7am and 1pm from Quan Lan to Van Don. There are also wooden boats departing at 7am and 1pm.

- Van Don - Minh Chau traffic route:

Chung Huong high-speed train, Minh Chau train, morning 7:30 and afternoon 13:30 from Van Don to Minh Chau, morning 6:30 and afternoon 13:00 from Minh Chau to Van Don.

f. Infrastructure

Despite receiving investment attention, the issue of infrastructure and technical facilities for tourism on Quan Lan Island is still an issue that needs to be resolved because it has a direct impact on the implementation of ecotourism activities. The minimum conditions for serving tourists such as accommodation, electricity, water, communication, especially medical services, and security work need to be given top priority. Ecotourism spots in Minh Chau commune are assessed to have better infrastructure and technical facilities for tourism because there are quite complete and synchronous conditions for serving tourists, meeting many needs of domestic and foreign tourists.

3.2.1.4. Determine assessment levels and assessment scales

Corresponding to the levels of each criterion, the index is the score of those levels in the order of 4, 3, 2, 1 decreasing according to the standard of each level: very attractive (4), attractive (3), average (2), less attractive (1).

3.2.1.5. Determining the coefficients of the criteria

For the assessment of DLST in the two communes of Quan Lan and Minh Chau islands, the students added evaluation coefficients to show the importance of the criteria and indicators as follows:

Coefficient 3 with criteria: Attractiveness, Exploitation time. These are the 2 most important criteria for attracting tourists to tourism in general and eco-tourism in particular, so they have the highest coefficient.

Coefficient 2 with criteria: Capacity, Infrastructure, Location and accessibility . Because the assessment area is an island commune of Van Don district, the above criteria are selected by the author with appropriate coefficients at the average level.

Coefficient 1 with criteria: Sustainability. Quan Lan has natural and human-made ecotourism sites, with high biodiversity and little impact from local human factors. Most of the ecotourism sites are still wild, so they are highly sustainable.

3.2.1.6. Results of DLST assessment on Quan Lan island

a. Assessment of the potential for natural tourism development

For Minh Chau commune:

+ Natural tourism attractiveness is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined as average (2 points) and the coefficient is quite important (coefficient 2), then the score of Capacity criterion is 2 x 2 = 4.

+ Exploitation time is long (4 points), the most important coefficient (coefficient 3) so the score of the Exploitation time criterion is 4 x 3 = 12.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is assessed as good (3 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 3 x 2 = 6 points.

The total score for evaluating DLST in Minh Chau commune according to 6 evaluation criteria is determined as: 12 + 4 + 12 + 4 + 4 + 6 = 42 points

Similar assessment for Quan Lan commune, we have the following table:

Table 3.3: Assessment of the potential for natural ecotourism development in Quan Lan and Minh Chau communes

Attractiveness of self-tourismof course

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

CommuneMinh Chau

12

12

4

8

12

12

4

4

4

8

6

8

42/52

Quan CommuneLan

6

12

6

8

9

12

4

4

4

8

4

8

33/52

b. Assessment of the potential for humanistic tourism development

For Quan Lan commune:

+ The attractiveness of human tourism is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined to be large (3 points) and the coefficient is quite important (coefficient 2), then the score of the Capacity criterion is 3 x 2 = 6.

+ Mining time is average (3 points), the most important coefficient (coefficient 3) so the score of the Mining time criterion is 3 x 3 = 9.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points.

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is rated as average (2 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 2 x 2 = 4 points.

The total score for evaluating DLST in Quan Lan commune according to 6 evaluation criteria is determined as: 12 + 6 + 6 + 4 + 4 + 4 = 36 points.

Similar assessment with Minh Chau commune we have the following table:

Table 3.4: Assessment of the potential for developing humanistic eco-tourism in Quan Lan and Minh Chau communes

Attractiveness of human tourismliterature

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Quan CommuneLan

12

12

6

8

9

12

4

4

4

8

4

8

39/52

Minh CommuneChau

6

12

4

8

12

12

4

4

4

8

6

8

36/52

Basically, both Minh Chau and Quan Lan localities have quite favorable conditions for developing ecotourism. However, Quan Lan commune has more advantages to develop ecotourism in a humanistic direction, because this is an area with many famous historical relics such as Quan Lan Communal House, Quan Lan Pagoda, Temple worshiping the hero Tran Khanh Du, ... along with local festivals held annually such as the wind praying ceremony (March 15), Quan Lan festival (June 10-19); due to its location near the port and long exploitation time, the beaches in Quan Lan commune (especially Quan Lan beach) are no longer hygienic and clean to ensure the needs of tourists coming to relax and swim; this is also an area with many beautiful landscapes such as Got Beo wind pass, Ong Phong head, Voi Voi cave, but the ability to access these places is still very limited (dirt hill road, lots of gravel and rocks), especially during rainy and windy times; In addition, other natural resources such as mangrove forests and sea worms have not been really exploited for tourism purposes and ecotourism development. On the contrary, Minh Chau commune has more advantages in developing ecotourism in the direction of natural tourism, this is an area with diverse ecosystems such as at Rua De Beach, Bai Tu Long National Park Conservation Center...; Minh Chau beach is highly appreciated for its natural beauty and cleanliness, ranked in the top ten most beautiful beaches in Vietnam; Minh Chau commune is also home to Tram forest with a large area and a purity of up to 90%, suitable for building bridges through the forest (a very effective type of natural ecotourism currently applied by many countries) for tourists to sightsee, as well as for the purpose of studying and researching.

Figure 3.1: Thenmala Forest Bridge (India) Source: https://www.thenmalaecotourism.com/(August 21, 2019)

3.2.2. Using SWOT matrix to evaluate Quan Lan island tourism

General assessment of current tourism activities of Quan Lan island is shown through the following SWOT matrix:

Table 3.5: SWOT matrix evaluating tourism activities on Quan Lan island

Internal agent

Strengths- There is a lot of potential for tourism development, especially natural ecotourism and humanistic ecotourism.- The unskilled labor force is relatively abundant.- resource environmentunpolluted, still

Weaknesses- Poorly developed infrastructure, especially traffic routes to tourist destinations on the island.- The team of professional staff is still weak.- Tourism products in general

quite wild, originalintact

general and DLST in particularalone is monotonous.

External agents

Opportunity- Tourism is a key industry in the socio-economic development strategy of the province and Van Don economic zone.- Quan Lan was selected as a pilot area for eco-tourism development within the framework of the green growth project between Quang Ninh province and the Japanese organization JICA.- The flow of tourists and especially ecotourism in the world tends toincreasing

Challenge- Weather and climate change abnormally.- Competition in tourism products is increasingly fierce, especially with other localities in the province such as Ha Long, Mong Cai...- Awareness of tourists, especially domestic tourists, about ecotourism and nature conservation is not high.

Through summary analysis using SWOT matrix we see that:

To exploit strengths and take advantage of opportunities, it is necessary to:

- Diversify products and service types (build more tourism routes aimed at specific needs of tourists: experiential tourism immersed in nature, spiritual cultural tourism...)

- Effective exploitation of resources and differentiated products (natural resources and human resources)

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s3 { color: #0D0D0D; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -3pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -2pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -1pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s10 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s12 { color: black; font-family:Symbol, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s13 { color: black; font-family:Wingdings; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s14 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s16 { color: black; font-family:Cambria, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s17 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s18 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s19 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s20 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; } div.maincontent .s21 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 11pt; } div.maincontent .s22 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s23 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s24 { color: #212121; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Source: NHCSXH It can be affirmed that the Savings and Credit Group plays a very important role in the activities of the NHCSXH. The Savings and Credit Group is a widespread network in the areas of the NHCSXH, contributing to determining the scale and quality of credit of the NHCSXH. The Savings and Credit Group is the place to directly appraise loans, monitor and inspect the process of using loans, guide and assist members in the process of using loans, urge debt repayment, and interest payment.

on time and carry out risk handling procedures, collect interest as authorized by the People's Credit Fund.

Third, capital mobilization to meet credit needs

The operating capital of the Vietnam Bank for Social Policies includes capital from the State budget; mobilized capital, borrowed capital; other capital and funds.

- Capital from the State Budget: includes charter capital; capital from the State Budget to implement credit programs; and capital from local budgets entrusted to the VBSP to implement local poverty reduction goals.

The charter capital of the Social Policy Bank when it was first established was 5,000 billion VND and every year, according to actual requirements and scale of operations under the direction of the Government, the Social Policy Bank reports to the Ministry of Finance to submit to the Prime Minister for decision to supplement the charter capital with an increase rate corresponding to the credit growth rate assigned by the Prime Minister every year. Affirming its concern for the poor and policy beneficiaries, the Government has provided an additional 5,000 billion VND in charter capital, increasing the bank's charter capital to 10,000 billion VND. In 2015, the Social Policy Bank was provided 695.5 billion VND by the Prime Minister, the Ministry of Planning and Investment, and the Ministry of Finance to supplement the charter capital in 2014 and fully compensate for the missing amount of 3,200 billion VND from the state budget.

Table 2.6: Scale of mobilized capital of the Social Policy Bank

Unit: billion VND

2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | |

Borrow from SBV & KB | 1,621 | 4,821 | 7,796 | 16,796 | 23,796 | 26,796 | 24,796 | 29,825 | 29,247 | 24,995 |

Capital from credit institutions | 12,534 | 16,946 | 29,711 | 33,034 | 29,053 | 30,279 | 32,137 | 25,744 | 30,055 | 35,608 |

Customer deposits | 1,682 | 1,999 | 987 | 1,125 | 1,975 | 2,843 | 4,046 | 4,652 | 6,183 | 7,993 |

Funding for UTĐT | 1,203 | 1,656 | 2,103 | 2,886 | 3,360 | 4,022 | 4,383 | 4,237 | 4,018 | 4,895 |

GTCG Release | 0 | 0 | 0 | 0 | 11,000 | 18,297 | 27,527 | 29,406 | 28,915 | 33,848 |

Other debt capital | 338 | 596 | 993 | 3,964 | 3,468 | 5,329 | 6,492 | 10,469 | 12,962 | 11,393 |

Equity | 8,029 | 10,036 | 13,120 | 16,543 | 19,148 | 19,881 | 22,879 | 24,877 | 25,071 | 27,727 |

Source: Annual report of the People's Credit Fund

Every year, the People's Committees at all levels balance the local budget capital entrusted to the VBSP to supplement the capital for lending to the poor and policy beneficiaries in the area. The total capital entrusted for investment by the local budget and domestic and foreign investors up to December 31, 2015 reached 4,895 billion VND, accounting for 3.3% of the total capital. Some typical provinces and cities entrusting a lot to the VBSP are Hanoi (1,306 billion VND), Ho Chi Minh City (438 billion VND), Ba Ria - Vung Tau (243 billion VND)... [16]

- Mobilized capital and borrowed capital

Loans and advances include loans from the State Bank (VND 21,495 billion), advances from the State Treasury (VND 3,500 billion) and foreign loans (VND 786 billion). The total capital source reached VND 25,781 billion, accounting for 17.6% of total capital sources, down 14.4% compared to 2014 due to debt repayment to the State Bank and the State Treasury [16].

Mobilized capital and market interest rate loans include receiving 2% deposits from credit institutions in which the State holds controlling shares; issuing bonds of the Social Policy Bank guaranteed by the Government, mobilizing from organizations and individuals, including receiving savings deposits of

Member of the Savings and Credit Group [16]. The 2% deposit capital of credit institutions in which the State holds controlling shares is implemented according to Decree No. 78/2002/ND-CP and Circular No. 23/2013/TT-NHNN (replacing Circular No. 04/2003/TT-NHNN) stipulating that State-owned commercial banks and joint-stock commercial banks in which the State owns more than 50% of charter capital are responsible for maintaining a deposit balance at the Vietnam Bank for Social Policies equal to 2% of the mobilized capital balance in VND at December 31 of the previous year. As of December 31, 2015, the deposit capital of State-owned credit institutions reached VND 35,608 billion, accounting for 24.3% of the total capital, an increase of 18.5% compared to 2014 [16].

With the Government's guarantee, the VBSP mobilized 33,848 billion VND from bond issuance, accounting for 23.1%, up 17.1% compared to 2014. The total issuance volume in the year was 14,949.3 billion VND (99.6% completed), paying off 10,000 billion VND of maturing bonds [16].

Capital mobilized from organizations and individuals is carried out according to commercial principles, with competition with other credit institutions in the area. The mobilization interest rate is in principle not to exceed the mobilization interest rate of the same type of State-owned commercial banks in the same area at the time. As of December 31, 2015, this mobilized capital reached 7,993 billion VND, accounting for 5.5% of the total capital. Of which, mobilization of savings deposits through the Savings and Credit Group reached 4,259 billion VND, an increase of 25.3% compared to 2014. According to regulations, poor households wishing to borrow capital from the Social Policy Bank need to join the local Savings and Credit Group and participate in savings activities through the Group to the bank. Although not mandatory, deposits from the poor and policy beneficiaries have also contributed a significant amount of capital to the total capital of the Social Policy Bank [16].

- Other sources of capital and funds

In addition to the above capital sources, the VBSP also makes the most of other capital sources and forms funds such as reserve fund for supplementing charter capital, development investment fund, financial reserve fund, credit risk reserve fund, unemployment reserve fund, reward fund, welfare fund, unallocated revenue-expenditure difference for funds, non-refundable aid capital from domestic and foreign organizations and individuals. As of December 31, 2015, the total of other capital sources and funds reached 10,607 billion VND, accounting for 7.2% of total capital [16].

In order to ensure the sustainability of capital sources and meet the credit needs of the poor and policy beneficiaries, the VBSP has constantly strived to find many methods and measures to mobilize capital. Thanks to that, the VBSP always promptly meets the capital needs for disbursing policy credit programs, and at the same time repays debts.

Maturity bonds, State Treasury loans and State Bank loans..., ensuring the ability to pay for the operations of the entire system.

By the end of 2015, the ratio of mobilized capital (excluding capital provided from the state budget, loans under the direction of the Government and other sources) compared to demand reached 57.77%.

d/ Adjust credit plan targets

Based on the capital situation, disbursement progress, and sudden capital needs of beneficiaries of preferential credit policies, the General Director shall balance, adjust, and supplement the credit plan targets each time for the provincial-level Social Policy Bank in the implementation year. For units, when there is a need to adjust the plan targets, the units shall prepare a report to the Head of the Board of Directors for approval to submit to the superior Social Policy Bank for consideration and decision [20].

In provincial and district-level units, the Directors of provincial and district-level banks are responsible for advising the Head of the Board of Directors of the same-level bank to flexibly adjust the planning targets for subordinate units, in accordance with the needs of implementing the local credit plan, in order to achieve the highest results in the credit plan assigned by the superior and promptly meet the borrowing needs of the poor and other policy subjects [20].

e/ Periodic summary and assessment

Periodically, the Social Policy Bank conducts a review of policy credit activities during the period, reviewing the results achieved compared to the targets, the work that has not been implemented or has been implemented but has not achieved the results according to the set targets. This work is implemented throughout the bank, from the Transaction Offices to the Head Office to grasp the reality, from there make proposals to the State management agencies, and provide timely and accurate solutions in the new period.

2.2.2.2. Policy credit management tools of the Bank for Social Policies

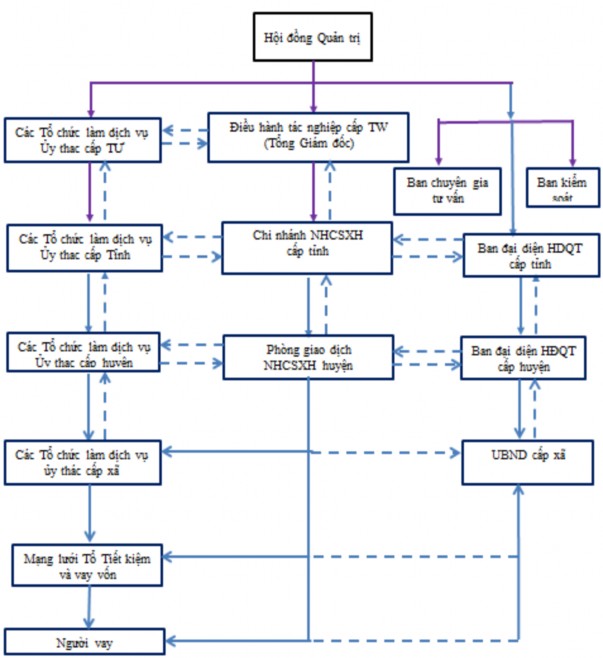

a/ Credit management network and apparatus

The Social Policy Bank was established on the basis of reorganizing the Bank for the Poor to implement the State's preferential credit policy for the poor and other policy subjects. Based on the requirement to concentrate resources, especially capital, the Social Policy Bank needs an organizational and management apparatus with the participation of State management agencies in formulating credit policies. According to Decision No. 16/2003/QD-TTg dated January 22, 2003 of the Prime Minister on promulgating the Charter of the organization

The organization and operation of the Social Policy Bank, the management organization model of the Social Policy Bank is in the form of State management agencies participating in policy issuance, while the General Director is in charge of the bank's operations. At the same time, with the participation of social-political organizations in entrusted service activities, the credit of the Social Policy Bank has been facilitated to reach policy beneficiaries in a timely, convenient, public, democratic and fair manner.

According to Decision No. 131/2002/QD-TTg dated October 4, 2002 of the Prime Minister, the apparatus of the Vietnam Bank for Social Policies includes 3 levels: Headquarters at the Central level, Provincial Branches and Transaction Offices at the district level, at each level there is an administrative apparatus and an operational apparatus.

- Headquarters located in Hanoi Capital: responsible for directing all activities of the entire VBSP system, including: Board of Directors (General Director and Deputy General Directors), 13 professional departments (Personnel Organization, Emulation - Reward, Capital Planning, Credit for the Poor, Credit for Students and Other Policy Subjects, Management and Handling of Risky Debts, Accounting and Financial Management, Basic Construction, International Cooperation and Communications, Internal Control and Audit, Finance, Legal Affairs, Office), Transaction Office, Training Center, Information Technology Center. In addition, there is also the Central VBSP Party Committee Office, Trade Union Office [17].

- Branches of the People's Credit Fund in provinces and centrally-run cities: including 63 branches of the People's Credit Fund in provinces and cities nationwide with an organizational structure including: Board of Directors and 5 professional departments (Credit Planning Department, Treasury Accounting Department, Organizational Administration Department, Internal Control and Inspection Department and Information Technology Department) with a staff of about 28 - 32 people [17].

- Transaction offices of the People's Credit Fund in districts, towns, cities under the provincial branches of the People's Credit Fund: including 629 Transaction Offices with an organizational structure consisting of the Board of Directors and 2 professional teams (Business Planning Team and Accounting Team). The Director is in charge of the District Transaction Office, assisted by Deputy Directors and Professional Team Leaders, each transaction office has a staff of 7-11 people. Transaction points at communes: to facilitate customers in the process of borrowing and repaying debts, the People's Credit Fund has established nearly 10,900 Transaction Points in communes, wards, and towns [17].

640

620

600

580

560

540

520

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

0

Number of transaction offices

Number of credit officers (right axis)

Figure 2.2: Number of transaction offices and credit officers of the People's Credit Fund

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Source: NHCSXH

With the current organizational structure, policy planning and credit policy consulting are mainly concentrated at the Head Office and operational activities are carried out at the Commune Transaction Points by the District Transaction Offices. The Provincial and District Board of Directors' Representative Boards mainly perform the task of supervising the implementation of credit policies at the local level. In order to enhance the capacity of managing credit activities at the grassroots level, the Prime Minister has allowed the pilot implementation of adding the Chairman of the Commune People's Committee to the Board of Directors of the VBSP at the district level in 03 provinces (Bac Giang, Thanh Hoa, Long An) to strengthen their role in managing and supervising policy credit activities in the area, contributing positively to consolidating the quality and improving the effectiveness of policy credit in poverty reduction and ensuring social security, associated with economic development.

- society. Up to now, nearly 100% of the Chairmen of the People's Committees at the commune level nationwide have been added by the Chairmen of the People's Committees at the provincial level to the composition of the Board of Representatives of the People's Credit Fund at the provincial level under the direction of the Prime Minister [17].

Pursuant to Article 5 of Decree No. 78/2002/ND-CP dated October 4, 2002, the Vietnam Bank for Social Policies and four socio-political organizations including the Women's Union, the Farmers' Association, the Veterans' Association, and the Ho Chi Minh Communist Youth Union signed a joint document and an agreement on the organization of the implementation of entrusted lending to poor households and other policy beneficiaries. After signing the joint document with the socio-political organizations, the Vietnam Bank for Social Policies signed an agreement with the socio-political organizations on the implementation of entrusted lending to poor households and other beneficiaries.

Other policies. After 3 years of implementation, some shortcomings have arisen, so the Social Policy Bank and the Associations and Unions have reviewed, supplemented and revised the content and methods of organizing the implementation of the entrustment with social organizations.

Figure 2.3: Organizational chart of the Social Policy Bank system

Source: NHCSXH

Basically, the credit management organization model of the VBSP has not changed since its establishment but has only been improved through the addition of a number of social-political organizations to the Board of Directors and Board of Representatives at all levels. This model with the participation of many ministries, branches and social-political organizations at all levels and especially the network of Savings and Credit Groups has increased the access opportunities of the poor and other policy beneficiaries to

policy credit sources as well as increasing the efficiency of loan use for poor beneficiaries and other policy subjects.

b/ Loan amount

The loan amount is determined based on the investment needs of customers and the ability to meet the capital of the Social Policy Bank. However, the Board of Directors has regulations on the maximum loan amount for each credit program and each borrower. The maximum loan amount of credit programs is also reviewed by the Board of Directors from time to time when there are changes in the economic and social situation and the ability to meet the investment needs of borrowers. The maximum loan amount is unified for all regions across the country according to the regulations of the Prime Minister for each program.

Table 2.7: Maximum loan levels of some credit programs for the poor and other policy subjects in 2015

STT

Loan object | Maximum loan amount maximum (million VND) | |

I | Poor household | |

Loans for the poor | 50 | |

Lending to poor households in 64 poor districts according to Resolution 30a | 10 | |

II | Near poor household | |

Loans for near poor households | 50 | |

III | Newly escaped poverty | |

Loans for newly escaped poverty households | 50 | |

IV | Students | |

Loans for students in difficult circumstances | 12.5/school year | |

V | Subjects need loans to solve employment | |

Loans for production and business establishments of war invalids and disabled people | 50 | |

Loans for war invalids and disabled people | 50 | |

Lending to other entities | 50 | |

VI | Subjects working abroad for a limited period of time | |

Loans to poor households and ethnic minorities 64 poor districts according to Resolution 30a | Do not exceed the loan ceiling of the Ministry of Labor, Invalids and Social Affairs | |

Lending to the remaining subjects in 64 poor districts according to the Resolution 30a | ||

Loan for labor export | ||

VII | Other subjects as decided by the Government |