(6b) Output VAT of products and goods used to pay salaries to employees.

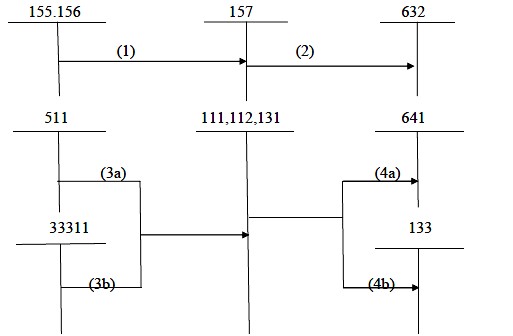

Diagram 02: Sales revenue by agent method (by selling at the right price and receiving commission)

Note:

Maybe you are interested!

-

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1 -

Completing revenue accounting and determining business results at Ha Lam Coal Joint Stock Company - Vinacomin - 16

Completing revenue accounting and determining business results at Ha Lam Coal Joint Stock Company - Vinacomin - 16 -

Completing revenue and cost accounting and determining business results at Nakashima Vietnam Co., Ltd. - 14

Completing revenue and cost accounting and determining business results at Nakashima Vietnam Co., Ltd. - 14 -

Accounting for revenue, expenses and determining business results at Saigon Real Estate Joint Stock Company - 1

Accounting for revenue, expenses and determining business results at Saigon Real Estate Joint Stock Company - 1 -

Completing the accounting of revenue, expenses and determining business results at Huong Duong Tourism Development and Service Company - 10

Completing the accounting of revenue, expenses and determining business results at Huong Duong Tourism Development and Service Company - 10

(1) When finished products are shipped from warehouse, goods are delivered to agents (according to the regular declaration method).

(2) When finished products and goods are delivered to agents for sale (3a) Agent sales revenue

(3b) Output VAT

(4a) Commission payable to the agent (4b) Input VAT

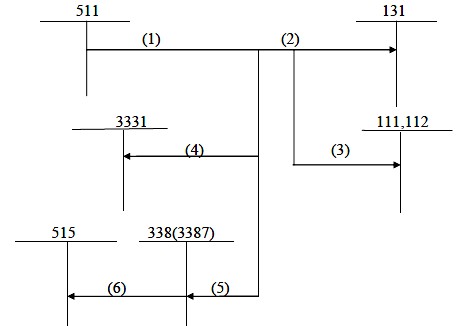

Diagram 03: Sales revenue by deferred payment (or installment payment)

Note:

(1) Sales revenue (recorded at cash price)

(2) Total amount receivable from customers

(3) Amount collected from customers

(4) Output VAT

(5) Installment interest or deferred interest receivable from customers

(6) Periodically transfer revenue is interest receivable each period.

1.4.2. Accounting for cost of goods sold.

Account used: Account 632: Cost of goods sold

This account is used to reflect the capital value of products, goods, services, investment real estate, and production costs of construction products (for construction enterprises).

In addition, this account is used to reflect expenses related to investment real estate business activities such as: depreciation costs, repair costs, and rental service costs for investment real estate under the operating lease method.

(in case of small occurrence), cost of transfer and liquidation of investment real estate.

Account 632 has no ending balance.

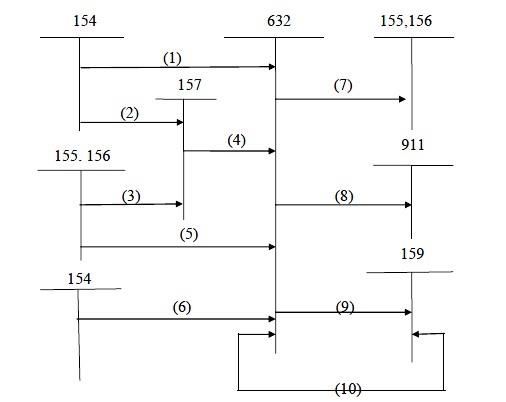

Diagram 04: Accounting for cost of goods sold using the perpetual inventory method

Note:

(1) Finished products are sold immediately without being put into storage.

(2) Finished products are sent for sale without being put into storage.

(3) When goods sent for sale are determined to be consumed

(4) Finished products, goods for sale

(5) Export finished products and goods for sale

(6) At the end of the period, the cost of completed services consumed during the period is transferred.

(7) Finished products and goods sold are returned to the warehouse.

(8) At the end of the period, transfer the cost of goods sold of finished products, goods and services consumed

(9) Reversal of inventory price reduction provision

(10) Provision for inventory price reduction.

1.4.3. Accounting for sales costs and business management costs.

1.4.3.1. Accounting for sales costs

Account used: Account 641: "Cost of sales"

This account is used to reflect actual costs incurred in the process of selling products, goods, and providing services, including costs of offering, introducing products, advertising products, sales commissions, product warranty costs (except construction activities), warranty costs, packaging, transportation, etc.

Account 641: Sales expenses has 7 sub-accounts: Account 6411: Employee expenses

Account 6412: Packaging material costs Account 6413: Tools and equipment costs Account 6414: Fixed asset depreciation costs Account 6415: Warranty costs

Account 6417: Cost of purchased external services Account 6418: Other cash expenses Account 641 has no ending balance.

1.4.3.2. Business management cost accounting.

Account used: Account 642: Business management costs.

This account is used to reflect the general management costs of the enterprise, including employee salary costs: business management department, social insurance, health insurance, union fees of business management staff, office materials costs, labor tools, depreciation of fixed assets used for business management, land rent, business license tax, provision for bad debts, outsourced services, other cash expenses (reception, conferences, etc.)

Account 642 has 8 sub-accounts:

Account 6421: Management staff costs Account 6422: Management material costs Account 6423: Office supplies costs Account 6424: Fixed asset depreciation costs Account 6425: Taxes, fees, charges

Account 6426: Provision expenses

Account 6427: Cost of purchased external services Account 6428: Other cash expenses Account 642 has no ending balance.

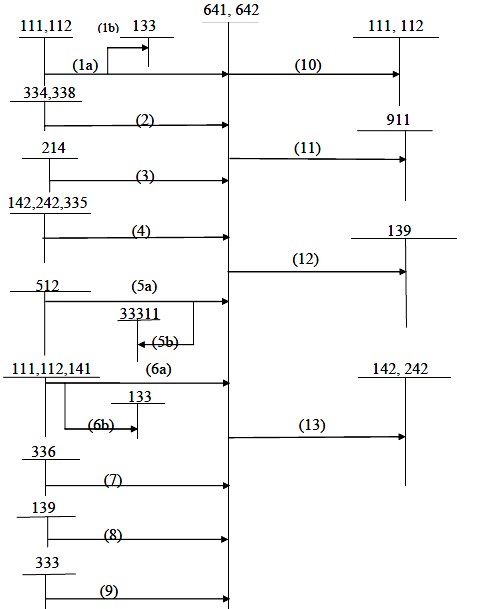

Diagram 05: Accounting for sales costs and business management costs

Note:

(1a,1b): Cost of materials, tools and equipment.

(2): Salary costs and salary deductions (3): Fixed asset depreciation costs

(4): Allocated costs, pre-deductible costs

(5a,5b): Finished products, goods, and services for internal consumption (6a): Cost of purchased external services and other cash costs.

(6b): Input VAT is not deductible if included in selling expenses.

(7): Subordinate management costs must be paid to superiors according to regulations.

(8) Provision for doubtful debts

(9): Business license tax, land rent payable to the state budget (10): Revenues reduced by expenditure

(11): Carry forward business management costs and sales costs.

(12): Reversal of the difference between the unused provision for doubtful debts set aside last year and the amount to be set aside this year.

(13): Reversal of pre-deductible expenses

1.4.4. Accounting for financial revenue and financial expenses.

1.4.4.1. Accounting for financial activity revenue

Account used: Account 515: Financial activity revenue

This account reflects the revenue from interest, royalties, dividends, shared profits and other financial revenue of the enterprise.

Financial revenue includes:

- Interest: Loan interest, bank deposit interest, deferred payment interest, installment sales interest, investment interest on bonds, treasury bills, payment discounts received from purchasing goods and services...

- Dividends, profits shared.

- Income from investment activities of buying and selling short-term and long-term securities.

- Income from recovery or liquidation of joint venture capital contributions, investments in associated companies, investments in subsidiaries, and other capital investments.

- Income from other investment activities

- Exchange rate profit

- Interest difference from selling foreign currency

- Interest difference due to capital transfer

- Other financial revenue account 515 has no ending balance.

1.4.4.2. Accounting for financial operating costs.

Account used: Account 635: Financial operating expenses

This account reflects financial operating expenses including expenses or losses related to financial investment activities, lending and borrowing costs, joint venture and association capital contribution costs, short-term securities transfer losses, etc. Provision for devaluation of securities investments, exchange rate losses, etc.

Account 635 has no ending balance.

1.4.5. Accounting for other operating income and other operating expenses

1.4.5.1. Accounting for other operating income.

- Account used: Account 711 - "Other operating income"

This account is used to reflect other operating income and revenue outside of the enterprise's production and business activities.

Account 711 - "Other income" has no ending balance.

1.4.5.2. Accounting for other costs incurred.

- Account used: Account 811 - "Other expenses"

This type of account reflects the expenses of activities other than the business activities that generate revenue for the enterprise. Other expenses are expenses (losses) caused by events or transactions separate from the normal operations of the enterprise and corporate income tax expenses.

Account 811 has no ending balance.