25

From the Bank's perspective, financial appraisal of an investment project is the organization, review, analysis and scientific and comprehensive assessment of all financial aspects of the project in terms of legality, feasibility, efficiency and debt repayment capacity of the investment project, in order to help the Bank make a decision to lend or not to lend to that project .

1.3.2.2. Contents of financial appraisal of investment projects in lending activities of commercial banks 15 , 19 , 21 , 22

Financial appraisal of investment projects includes many closely related contents. The main contents that appraisers focus on are:

a) Appraisal of total investment capital and investment capital structure as well as progress

Maybe you are interested!

-

Loan Turnover for Investment Projects at Vietcombank – Hue Branch in the Period 2015-2017

Loan Turnover for Investment Projects at Vietcombank – Hue Branch in the Period 2015-2017 -

Investment Situation in Non-Credit Services at Saigon Commercial Joint Stock Bank in the Period of 2015-2019

Investment Situation in Non-Credit Services at Saigon Commercial Joint Stock Bank in the Period of 2015-2019 -

Limitations of State Management of Urban Construction Investment Projects

Limitations of State Management of Urban Construction Investment Projects -

General Assessment of the Current Situation of Public Investment Capital Management at the Ministry of Health in the Period 2016 - 2020

General Assessment of the Current Situation of Public Investment Capital Management at the Ministry of Health in the Period 2016 - 2020 -

Credit Investment at Bidv Son Tay in the period 2012-2014

Credit Investment at Bidv Son Tay in the period 2012-2014

project capital use

Check the determination of the total investment capital of the project

“Total investment capital” is the total investment and construction costs and is the maximum cost limit of the project as determined in the investment decision. This is the value of all assets required to establish and operate the project and the capital required to implement the project. According to current regulations, the total investment capital of the project includes:

Fixed capital

- Investment preparation costs: are costs that do not directly create fixed assets but are indirectly related to the creation, operation and exploitation of those assets to achieve investment goals such as: investigation and survey costs to establish and submit investment projects for approval, consulting and project design costs, technology transfer costs.

- Construction and equipment purchase costs such as: initial costs for land and water, costs for preparing construction sites, costs for constructing temporary auxiliary works serving construction, costs for demolishing old structures, costs for leveling construction sites, costs for purchasing new machinery, equipment and means of transport.

- Other costs: project management costs, training costs, expert hiring costs, insurance costs, bank loan interest costs.

Working capital

It is the capital to meet the regular expenditure needs after the end of the investment implementation phase mobilized into production according to the technical and economic conditions to achieve the proposed capacity. The working capital needs for the project are usually determined on the basis of the estimated current assets in the project's operating years such as the average reserve needs of the following factors: cash, raw materials, semi-finished products, finished products, etc.

26

ΠReserve capital

This is the cost to reserve for objects arising due to design changes as required by the investor approved by the competent authority, objects arising without foreseen or the reserve due to price fluctuations during project implementation...

Check the structure of investment capital and capital usage progress

Based on recalculation of total investment capital, equity capital and capital from other sources participating in the project as well as the financial capacity of the enterprise, the Bank will re-determine the loan capital demand to implement the project.

Loan capital = Total capital needs – Owner's capital – Other capital

Based on the results of economic, market, technical assessment and expected progress

The investment level will determine the progress of capital use.

b) Project cash flow appraisal

Project cash flows are the expected cash flows generated by the project itself and available to pay long-term debts (both principal and interest) for reinvestment and equity recovery. Contents of project cash flow appraisal:

* Check the accuracy and reasonableness of project revenue and cost figures:

- Regarding revenue: the project's revenue is estimated annually, including revenue from main products, revenue from by-products and revenue from providing services. In the analysis of the project's revenue, two main issues are clarified: selling price, annual production and consumption output. And on the basis of market assessment and technical assessment, the exploitation capacity and annual sales output corresponding to the expected price and expected costs will be calculated.

- Regarding costs: The bank will check whether the enterprise's calculation has fully included all cost factors or not? And are the costs calculated by the enterprise reasonable? Based on the production and business plan, fixed asset depreciation plan and debt repayment plan, costs include the following items: Costs of main raw materials and auxiliary materials; Costs of purchased services; Costs of fuel, energy, and motivation; Costs of salaries, allowances and deductions from salaries; Costs of fixed asset depreciation; Costs of enterprise management; Costs of workshop management, etc.

* Recalculate the project's net cash flow from the Bank's perspective:

The Bank calculates the net cash flow from the perspective of a sponsor who co-invests with the enterprise. Therefore, the net cash flow of the project calculated from the Bank's perspective includes the cash flow generated by the project for both the Bank and the enterprise.

27

customers and businesses. For each case of investment capital, the project's net cash flow is calculated according to different formulas. However, in principle, the project's net cash flow (NCF - Net Cash Flow) includes two parts:

- Operating Cash Flow (OCF): includes profit after tax, depreciation and interest.

- Project investment cash flow: includes two parts: investment in fixed assets and regular working capital. In which, investment in fixed assets can be spent once in the first year or spent in several years during the project implementation and operation, usually with a negative sign (-) while regular working capital can be with a negative sign (-) or a positive sign (+).

NCF = OCF + project investment cash flow

* Set up financial forecast tables including: Output and revenue spreadsheet, operating cost spreadsheet, business management cost spreadsheet, sales cost spreadsheet, fixed asset depreciation spreadsheet, business performance report, cash flow report, etc.

b) Appraisal of financial efficiency assessment criteria of the project

Investors often use the following criteria:

- Discount rate (DR)

- Net present value (NPV) indicator

- Internal rate of return (IRR)

- Modified internal rate of return (MIRR)

- Payback period (PP)

- Profitability Index (PI)

Discount rate (DR)

Before appraising the financial indicators of an investment project, a very important factor that needs to be appraised first is the project's discount rate (DR). Because DR and NPV are inversely proportional, investors often determine that a small DR leads to a large NPV to increase the project's financial efficiency and make it easier for the project to be accepted by the bank. Therefore, the bank needs to re-evaluate DR to serve as a basis for accurately calculating the project's NPV indicator.

The discount rate must be calculated on the basis of compensating for opportunity cost, inflation and risk of capital loss, then DR is considered a reasonable discount rate of the project. In case the project is financed by a mixture of the enterprise's own capital and

28

For bank loans, the project's discount rate is the weighted average cost of capital (WACC).

WACC = (W x Kđ ) + (W S x K S )

In there:

W đ Is the proportion of borrowed capital in the total investment capital W S Is the proportion of equity capital in the total investment capital K đ Is the cost of bank debt

Ks is the cost of equity

Meaning of the indicator : The discount rate is the lowest expected rate of return that an investor expects when investing in a project. That return must ensure that it covers the opportunity cost, inflation and risk level of the project.

Net present value (NPV) indicator 15

NPV(Net Present Value) is the difference between the present value of the project's future net cash flows and the present value of the investment.

Recipe :

n

N PV= Σ CF t

(1+r) t

- CF 0

In there :

t=1

CF t is the net cash flow of the project in year t CF 0 is the initial capital outlay

n is the number of years from the start of the investment to the end of the project r is the discount rate applied to the project

Meaning of the indicator : Determining NPV in a project has great economic significance, it helps us evaluate the financial efficiency of the investment project. The NPV indicator tells us the scale of net income calculated at the present time of the entire investment and operation process of the project. When using NPV to make decisions with independent projects, if NPV > NPV dm , then we should invest. As for a set of mutually exclusive projects, among the projects with NPV > NPV dm , we should choose the project with the maximum NPV.

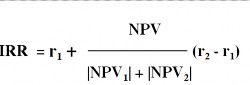

ΠInternal rate of return (IRR) 15

IRR (Internal Rate of Return) is a measure of the rate of return on investment of a project. Technically, the IRR of a project is the discount rate at which NPV = 0

Recipe :

29

n

ΣCF t

(1+IRR) t

-CF 0 =0

t=1

Normally, IRR is calculated by linear interpolation or linear extrapolation, that is, choosing two discount rates r 1 and r 2 so that NPV(r 1 ) > 0 or < 0 and NPV(r 2 ) < 0 or > 0, then calculating IRR according to the formula:

Meaning of the indicator : IRR reflects the profitability of the project, not taking into account the opportunity cost of investment capital. That is, if the cash flows are discounted according to IRR, the total present value of the cash flows (PV) will be equal to the initial investment capital (CF 0 ).

- When using IRR to make decisions for independent projects if IRR

If IRR is bad then you should invest.

- With a set of mutually exclusive projects, among the projects with IRR > IRR dm , the project with the max IRR should be chosen.

º Modified Internal Rate of Return (MIRR) 15

MIRR (Modified Internal Rate of Return) is the discount rate at which the present value of the investment cost is equal to the present value of the total future value of the net cash flows from the project, assuming that these cash flows are reinvested at an interest rate equal to the average cost of capital (denoted by k).

Recipe :

n CF t (1 + k) nt

= CF 0

t=1 (1 + MIRR) n

6 Payback period (PP) indicators 15

PP (Payback Period) is the period of time required for the additional income generated from the project to repay the initial capital. Calculation method:

By cumulative method:

T

(W + D) iPV I V0

t=0

30

In there :

T is the year of debt repayment

(W + D) iPV is the income of year i I V0 is the loan amount

According to the deduction method: If I Vi is the loan amount to be repaid in year i then

i = I Vi – (W + D)i is the remaining unrecovered loan capital of year i that must be transferred to year (i + 1) for further recovery. We have: I Vi + 1 = i (1 + r) or I Vi = i- 1 (1 + r) when i 0 then i T

◉ Profitability Index (PI) 15

PI (Profit Index) is an index reflecting the profitability of a project calculated by dividing the total present value of future cash flows by the initial investment capital.

CF t t

(1 + r) t

NPV + CFo

PI = =

CF 0 CFo

Recipe:

In there :

CF t is the net cash flow of the project in year t CF 0 is the initial capital outlay

PV is the present value of the net cash flows

Meaning of the indicator : PI shows how much current income or current net profit each initial investment brings.

The project is only accepted when PI > 1, meaning the project is profitable. In case there are many mutually exclusive projects, choose the project with PI > 1 and the largest PI.

d) Assess the project's risk level

A project usually has a lifespan of 10 to 50 years. Projects are established and calculated for financial efficiency based on the forecast of future business and profit processes. In a market economy, forecast data always changes, especially in the distant future, and the possibility of the project encountering risks is inevitable. Therefore, when evaluating and analyzing a project, we need to consider the possibilities that the project may encounter in order to have measures to prevent and limit risks, ensuring the project's ability to recover and generate profits. Especially for the Bank that is the project lender, unexpected risks that occur affect the project's ability to recover and generate profits.

31

the project's debt repayment capacity and the risk of losing capital of the Bank. Therefore, risk analysis is more necessary in project financial appraisal, assessing the level of risk of the project is also a very important information in making investment decisions.

Project risk analysis has many complex methods and different practical implications:

Sensitivity Analysis

The effectiveness of the project depends largely on the factors forecasted during project preparation. Forecasts can be misleading, especially when fluctuations occur in the distant future. Therefore, when appraising an investment project, it is necessary to assess the stability of the project's efficiency indicators when the input factors and project costs fluctuate. In other words, it is necessary to analyze the sensitivity of the project according to those fluctuating factors. During the sensitivity analysis, people predict some changing situations, future risks that cause raw material prices to increase, labor costs to increase, output to decrease and revenue to decrease... and then recalculate the financial efficiency indicators NPV, PI, IRR... If those indicators after recalculation still meet the requirements, the project is considered stable and accepted. On the contrary, if the project is considered unstable, it must be considered and recalculated before being invested. Project sensitivity analysis is typically performed in four steps:

- Step 1: Determine which factors are likely to change in a negative direction (to determine this trend, it is necessary to base on past statistics, forecast data and especially the practical experience of analysts)

- Step 2: Based on the selected factors, predict the maximum possible fluctuation amplitude compared to the initial standard value.

- Step 3: Choose an effective indicator to evaluate a certain sensitivity, such as analyzing sensitivity according to NPV or IRR indicators.

- Step 4: Re-determine NPV and IRR according to new variables, based on increasing and decreasing variables by the same percentage.

Calculation formula:

E =

In there:

F i

X i

E is the sensitivity index

F i is the fluctuation level (%) of the efficiency index

X i is the fluctuation level (%) of the influencing factor

32

The results of sensitivity analysis tell us which factors in the project need to be carefully studied and sufficient information collected to prevent and limit risks that may occur during the project's exploitation and operation.

However, this method also has some limitations:

- Sensitivity analysis does not take into account the probability of failure.

- Does not take into account the correlation between events

- Changing the value of sensitive events by a certain percentage does not always have a relationship with the variation of the observed performance variables….

Discount Rate Adjustment Method

The methods of financial appraisal of investment projects are basically present value methods, so the results of the appraisal depend largely on the selected discount rate, which is the basis for calculating the financial efficiency assessment indicators of the project. The essence of that choice is to consider the discount rate as a necessary cost for using capital, meaning that the appraiser has determined a given level of efficiency, the smaller the discount rate, the higher the efficiency achieved and vice versa. Obviously, in any case, that level of determination is always subjective, so to be on the safe side, we must assume that the efficiency can be achieved at a certain level by using a higher discount rate, that is, adjusting the discount rate to increase. That is the essence of the discount rate adjustment method.

The basic content of this method is to adjust the base discount rate which is considered to be risk-free or considered to have accepted the minimum risk level according to the principle of adding a risk premium to this base discount rate. The amount of this additional amount depends on the risk level of the project. This means that the greater the risk level of the project, the higher the discount rate. The difference between the adjusted discount rate and the cost of capital is called the risk premium. Thus, different projects often have different levels of risk, so they have different full discount rates.

After adjustment, we use this new discount rate to calculate the project's financial performance indicators. According to the above risk compensation principle, the full discount rate can be determined by two methods: subjective method and objective method.