Sales contracts, consulting and answering customer questions, making business plans and carrying out tasks assigned by superiors.

- Accounting and Finance Department: Responsible for making financial plans for the Company, organizing payments in accordance with the Company's payment regulations, organizing accurate, timely, continuous and systematic recording and reflection of economic transactions, fluctuations in materials, labor, capital, determining financial business results and profit distribution, organizing inventory, re-evaluating materials and goods to preserve capital and income, synthesizing data on production and business situations to serve the planning of economic activity analysis and economic reporting according to the Company's regulations. Responsible for the Company's finances, managing the Company's capital sources, deciding on all financial activities, calculating all business activities of the unit

- Technical Department: Responsible for the technical side and product quality. Such as: Researching and manufacturing new products, testing water samples, assembling, repairing and maintaining machinery and consulting customers when needed.

- Design construction configurations and plan for

Design construction configurations and plan for  projects

projects

3.4.2 Organization of accounting department at the Company

Chief KT

(KT synthesis)

Warehouse KT

Treasurer

3.4.2.1 Accounting organization chart

Diagram 3.2

Functions and duties of members in the Accounting department:

The company's accounting system is organized in the form of centralized accounting. The accounting department at the company's office is responsible for performing all accounting tasks from receiving and processing documents, circulating and recording books, summarizing, preparing financial reports, analyzing economics, and guiding accounting inspections for the entire company.

- Chief Accountant (also general accountant): Organize the accounting work of the Company according to the provisions of the Law and the Company's regulations. Be responsible before the law as well as build regulations at the unit so that operations are in accordance with the regulations and laws prescribed by the State.

- Manage cash receipts and disbursements promptly, accurately and in accordance with regulations, only disburse money when approved by the Director and Chief Accountant. Update the cash book daily. Conduct periodic and ad hoc fund inventories.

- Warehouse accounting: Manage the warehouse and perform warehouse accounting tasks: Prepare documents, inventory, and reconciliation. Write import and export vouchers according to the requirements of the material departments, and check documents for legality. At the end of the month, prepare documents for importing materials, fixed assets, and goods, check, reconcile, and summarize. At the same time, prepare documents for exporting - importing - storing materials, fixed assets, and goods, and compare them with actual inventory. If there is a difference, determine the cause of excess or shortage, and make a record to submit to the Director or Deputy Director for handling.

Monitor the amount of remaining goods in the company to promptly report to the sales department for handling measures.

3.4.2.2 Organization of accounting forms applied at the Company

Based on the scale, business characteristics, number of transactions, and providing detailed, specific, and timely data to managers, the Company applies the "General Journal" accounting form. Accounting work is conducted entirely on Excel accounting software on computers.

This form includes the main books: General Journal; Ledger; Detailed books and cards.

Business operations arise

KT certificate

KT Software

General ledger

Detailed accounting book

KT Report

Diagram 3.3Accounting chart in the form of General Journal

Note:

Enter daily data Print at the end of the month, end of the year Reconciliation

3.4.2.3 Accounting regime applied at the Company

KT regime at the Company: According to Circular 200/2014/TT-BTC.

KT regime at the Company: According to Circular 200/2014/TT-BTC.

The Company's accounting year: Starts from January 1, ends on December 31, 2018. The Company shall make a final financial report at the end of each year according to the regulations of the Ministry of Finance.

The Company's accounting year: Starts from January 1, ends on December 31, 2018. The Company shall make a final financial report at the end of each year according to the regulations of the Ministry of Finance.

VAT calculation method: By deduction method.

VAT calculation method: By deduction method.

Fixed asset valuation principles: Based on original price and residual value.

Fixed asset valuation principles: Based on original price and residual value.  Depreciation calculation method: Straight-line depreciation.

Depreciation calculation method: Straight-line depreciation.

KT HTK method: Regular declaration.

KT HTK method: Regular declaration.

Method of calculating warehouse price: Weighted average for materials issued for construction and goods for sale; for completed construction projects, the cost price is calculated at the actual specific price.

Method of calculating warehouse price: Weighted average for materials issued for construction and goods for sale; for completed construction projects, the cost price is calculated at the actual specific price.

CHAPTER 4: CURRENT STATUS OF ACCOUNTING FOR REVENUE, EXPENSES AND DETERMINATION OF BUSINESS RESULTS AT TAN VIET MY TRADING AND SERVICES COMPANY LIMITED IN 2015

4.1 Accounting for revenue and other income

4.1.1 Accounting for sales revenue and service provision

4.1.1.1. Content of sales revenue and service provision

Sales revenue and service provision of Tan Viet My Company in 2015 included two main segments:

Revenue from the supply of goods, materials, medical technical equipment, experiments, and environmental treatment for hospitals, medical units, schools, biochemical laboratories, and environmental treatment plants, such as: artificial kidney dialysis machines, absorbable screws, sutures used in laparoscopic surgery, patient beds, medicine cabinets, citric acid, environmental treatment microbiological preparations, 20Na cation resin, water pumps, solenoid valves, sand, activated carbon, etc.

Revenue from the supply of goods, materials, medical technical equipment, experiments, and environmental treatment for hospitals, medical units, schools, biochemical laboratories, and environmental treatment plants, such as: artificial kidney dialysis machines, absorbable screws, sutures used in laparoscopic surgery, patient beds, medicine cabinets, citric acid, environmental treatment microbiological preparations, 20Na cation resin, water pumps, solenoid valves, sand, activated carbon, etc.

Revenue from construction and installation of medical equipment systems, waste treatment systems, environmental facilities at hospitals, schools, etc.

Revenue from construction and installation of medical equipment systems, waste treatment systems, environmental facilities at hospitals, schools, etc.

4.1.1.2. Sales method and time of revenue recognition

Sales methods:

The company mainly signs contracts for the purchase and installation of medical equipment projects (dissolvable screws, endoscope burners, joint water pump lines, automatic infusion machines, citric acid, etc.), wastewater treatment equipment (Ozone machines, water filter columns, filters, valves, etc.). The company's sales network spans all hospitals, schools, and medical projects across the country. Currently, the company has two main forms of sales: wholesale through warehouses and wholesale direct shipping:

+ Wholesale through warehouse: The Company purchases and stores small-sized goods and materials of a regular business nature at the Company's warehouse when needed.

Export and sale, the Company will export goods to customers according to the economic contract or agreement between the two parties.

When delivering goods, the accounting department will make an invoice (3 copies), give the customer copy 2 (red), and the warehouse accountant will use copy 2 to make a warehouse delivery note and deliver the goods.

+ Wholesale direct shipping: This form is often applied to items with large size and weight (such as: artificial kidney dialysis machine, 1500 liter stainless steel tank, pump...) to save costs and space, the company exports and transports directly:

o Case 1 : For purchased goods, after receiving orders from customers, the sales department will find sources of goods that meet the customer's requirements and quote prices. When the customer accepts to buy, the company will request the seller to transport the goods directly from the seller's warehouse to the customer's warehouse. When the customer notifies that the goods have been received, KT will base on the PXK sent by the seller to create a VAT invoice and send the invoice to the customer.

o Case 2 : For materials installed for the project, after detailing the equipment and materials needed to be installed for the project, there is an agreement between the two parties: the contractor (enterprise) and the investor.

(customer), the materials will be transported directly to the construction site by the seller for installation and construction. The contractor will monitor and collect all materials delivered to the project so that after completion, the total value of the project will be calculated. When the project is handed over, KT will prepare a VAT invoice and send it to the customer.

Time of recording revenue:

Case 1: For goods, revenue is recorded when the goods are shipped from the warehouse (wholesale through the warehouse) or when the customer confirms the goods imported into the warehouse (wholesale direct shipping) and at the same time the VAT invoice is created and delivered to the customer and the customer accepts payment.

Case 1: For goods, revenue is recorded when the goods are shipped from the warehouse (wholesale through the warehouse) or when the customer confirms the goods imported into the warehouse (wholesale direct shipping) and at the same time the VAT invoice is created and delivered to the customer and the customer accepts payment.

Case 2 : For projects, after completing construction and installation work, testing operation and signing the project handover minutes, KT will issue a VAT invoice to the customer after the customer accepts payment.

Case 2 : For projects, after completing construction and installation work, testing operation and signing the project handover minutes, KT will issue a VAT invoice to the customer after the customer accepts payment.

Payment methods: Customers can pay before or after the sales contract is signed or upon receipt of goods.

- If the customer makes immediate payment: Collect in cash (contract value < 20 million VND), collect via bank (contract value >= 20 million VND).

- If the customer has not paid: KT records and tracks each customer's debt.

4.1.1.3. Accounting documents and books

Economic contract: signed between 2 buying and selling parties, when the quantity of items for one shipment is large (> 5 items) and has high value (> 50 million/item) or depending on the agreement between the two parties; and for projects (Bidding contract);

VAT invoice: Based on the contract value, agreement and actual warehouse delivery (PXK), KT issues VAT invoice to customers. If the customer pays immediately in cash, the cashier will record a receipt, if there is a debt, KT will record the receivable debt;

Receipt: Prepared by the cashier for receipts from receiving payments from customers;

Bank statement when customer pays by bank transfer.

NKC book, General ledger account 511;

Detail book of account 511, account 131;

straight (seller)

Signing contracts and agreements (P.KD)

VAT invoice

(KT synthesis)

Receipt, (Cashier) Bank credit note

General Journal, General Ledger

(on the machine)

Cash book;

Warehouse export (PXK), delivery (KT warehouse )

Transport |

Maybe you are interested!

-

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1

Completing the organization of accounting for revenue, sales costs and determining business results at Hai Phong Paint Joint Stock Company - 1 -

Completing the organization of revenue and cost accounting and determining business results at VIETTEC Inspection and Logistics Joint Stock Company - 9

Completing the organization of revenue and cost accounting and determining business results at VIETTEC Inspection and Logistics Joint Stock Company - 9 -

"Completing the organization of revenue and cost accounting and determining business results" at Tan Phu Agricultural Processing Enterprise - 2

"Completing the organization of revenue and cost accounting and determining business results" at Tan Phu Agricultural Processing Enterprise - 2 -

Completing the organization of revenue and cost accounting and determining business results at Xuan Truong Hai Transport and Trading Joint Stock Company - 2

Completing the organization of revenue and cost accounting and determining business results at Xuan Truong Hai Transport and Trading Joint Stock Company - 2 -

Completing revenue accounting and determining business results at Ha Lam Coal Joint Stock Company - Vinacomin - 16

Completing revenue accounting and determining business results at Ha Lam Coal Joint Stock Company - Vinacomin - 16

Diagram 4.1 : Sales revenue recognition processing sequence

4.1.1.4 User account

The enterprise uses account 511 "Sales and service revenue" to record sales revenue. The enterprise opens detailed account 5111_ Sales revenue of goods and detailed account 5113_Service revenue. However, because in the operating situation of 2 years 2015-2016, the enterprise did not generate revenue from any service provision activities, so currently the enterprise only uses detailed account 5111.

There are also related accounts:

Account 111: Cash – VND

Account 112: Bank deposits

Account 113: Customer receivables

Account 3331: Output VAT

4.1.1.5. Actual transactions occurring at the Company

Example 1: On November 2, 2015, the Company handed over the waste treatment system installation project to Phuc An Khang General Hospital. The total pre-tax value of the project according to VAT Invoice No. 0000977 is VND 45,454,545, VAT (10%) is VND 4,545,455. The hospital has not paid yet.

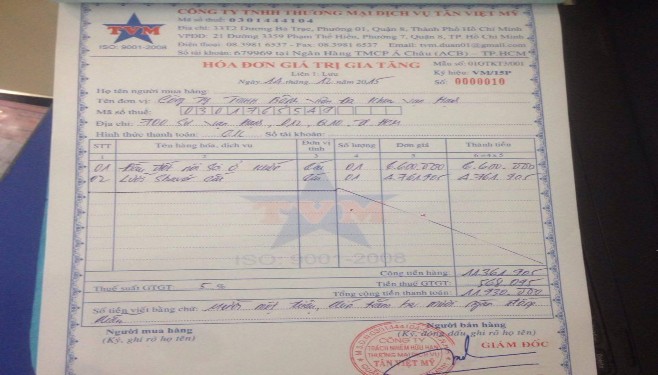

Example 2: On December 14, 2015, upon receiving a request for goods supply from Van Hanh General Hospital Company Limited transferred from the sales department, the warehouse accountant issued the goods (including: 1 endoscope burner, 1 Shaver blade). Based on the PXK sent by the warehouse accountant, the accountant synthesized and issued a VAT invoice consisting of 3 copies. The total value of the invoice excluding VAT is 11,361,905 VND, VAT (5%) is 568,095 VND and the customer has not paid for the goods.

Figure 1: VAT Invoice No. 0000010

Unit: Tan Viet My Co., Ltd. Form No. 02 - VT

Department: TVM Warehouse (Issued under Decision No. 15/2006/QD-BTC dated March 20, 2006 of the Minister of Finance)

WAREHOUSE DELIVERY NOTE

December 14, 2015 Debt: 632 Number: PXK04/12-HH Owner: 1561

Consignee's name: Van Hanh General Hospital Company Limited

Reason for release: Sales to customers

Exported from warehouse: Tan Viet My. Location: 33T2 Duong Ba Trac, Ward 01, District 8, Ho Chi Minh City.

Name, brand, specifications,

Unit

Quantity

STT

material goods, products, goods

Mao So

calculate

Love Food

export

Unit price Total price

ACD 1 2 3 4

01 Endoscopic probe 1 1 6,500,000 6,500,000

02 Shaver razor 1 1 4,650,000 4,650,000

Unit 2 2 11,150,000

Issuer Receipt of Warehouse Receipt (Signature, full name)

(Name, surname) (Name, surname)

Tran Trong

Chief Accountant (Signature, full name)

Tran Van

Director

(Name)

Myo Dung Temple

Figure 2: Goods delivery note 04/12