The direction is clear, so although the bad debt of the real estate business at banks has not increased as strongly as the steel industry, in terms of value, it has increased quite strongly. In 2014, the overdue debt of the real estate business was 62.68 billion VND, accounting for 13.7% of the total overdue debt. In 2015 and 2016, it was 87.7 billion VND and 72.37 billion VND, respectively 15.4% and 12.1% of the total overdue debt of the whole industry.

The food and foodstuff industry is also one of the industries with a high proportion of overdue debt of the Bank. In 2014, the overdue debt of the food and foodstuff industry was 54.9 billion VND, accounting for 12% of total overdue debt, in 2015 it was 66.06 billion VND, equivalent to 11.6% of total overdue debt, in 2016 it was 68.18 billion VND, equivalent to 11.4% of total overdue debt. In 2014, the overdue debt of the waterway and road transport industry decreased to 9% of total overdue debt, equivalent to 41.18 billion VND. However

However, in 2015 and 2016, it increased by 11% and 10.5% of total debt, respectively, to VND 62.64 billion and VND 62.8 billion.

overdue,

The main industries leading to overdue debt have tended to increase rapidly in recent times, so the overdue debt situation for other industries of the Bank has been decreasing in structural proportion. However, due to the rapid increase in overdue debt of the bank over the years, the value of overdue debt of the bank for other industries has still increased. In 2014, overdue debt was 227.38 billion VND, in 2015 it was 250.58 billion VND, in 2016 it was 288.87 billion VND.

Measured by internal credit rating scoring method

On the basis of Decision 493/2005/QD/NHNN dated April 22, 2005, OCB issued Decision No. 163/2012/QD – OCB dated March 16, 2012 on: “Internal credit rating”. Accordingly, OCB has determined that customer credit rating is the determination of the credit rating coefficient on the ability to repay debt and fulfill financial commitments for credit loans, loans payable to suppliers, and tax obligations according to the law, through analysis, evaluation, scoring and synthesis of rating scores from criteria in the categories of financial risk, business risk, management risk and reputational risk . ( Details in Appendix 02 of the thesis )

Table 2.10: Customer credit rating

Rating

Risk Classification | Detail | |

AAA | Qualified Debt | From 90 to 100 points |

AA | Qualified Debt | From 85 to 90 points |

A | Qualified Debt | From 75 to 85 points |

BBB | Debts to Watch Out For | From 70 to 75 points |

BB | Debts to Watch Out For | From 65 to 70 points |

B | Substandard debt | From 60 to 65 points |

CCC | Substandard debt | From 56 to 65 points |

CC | Substandard debt | From 53 to 56 points |

C | Doubtful debt | From 45 to 53 points |

D | Bad Debt | From 20 to 40 points |

Maybe you are interested!

-

Credit risk management at Vietnam International Commercial Joint Stock Bank - Hanoi Branch - 12

Credit risk management at Vietnam International Commercial Joint Stock Bank - Hanoi Branch - 12 -

Credit risk management for personal loans at Nam A Commercial Joint Stock Bank - Quang Ninh Branch - 13

Credit risk management for personal loans at Nam A Commercial Joint Stock Bank - Quang Ninh Branch - 13 -

The Role of Risk Management in Credit Activities at Commercial Banks

The Role of Risk Management in Credit Activities at Commercial Banks -

Credit risk management at Military Commercial Joint Stock Bank, Hue Branch - 12

Credit risk management at Military Commercial Joint Stock Bank, Hue Branch - 12 -

Current Status of Credit Risk Management at Vietnam Bank for Agriculture and Rural Development

Current Status of Credit Risk Management at Vietnam Bank for Agriculture and Rural Development

Source: Decision No. 163/2012/QD – OCB dated March 16, 2012 Regarding: “Internal credit rating”

According to OCB's current credit rating regulations, the rating scale is designed in 5 levels from 20 to 100, applied to the lowest level of assessment criteria. The scoring criteria are implemented in 5 levels: 20, 40, 60, 80, 100; corresponding to level 20 being the highest risk and 100 being the lowest risk. Accordingly, customer scoring is regulated into specific groups:

The qualified debt group includes AAA; AA; A: this is a group of customers with high ratings and best debt repayment ability.

The debt groups that need attention include BBB and BB: customers who are able to repay their debts in full. However, adverse economic conditions and changes in external factors are more likely to reduce the customers' ability to repay.

Substandard debt group includes B; CCC and CC: is a group of customers with high risk of default. Business, financial and economic conditions will affect the ability and willingness of customers to repay.

Doubtful debt group includes class C: is a group of customers who have carried out bankruptcy procedures or have similar actions but the customer's debt repayment is still maintained.

Group of debt with the possibility of losing capital includes class D: is the group of current customers who have lost the ability to pay debt, the loss has actually occurred to the Bank.

Measurement by IRB method

Currently, OCB is building a roadmap towards a modern risk management model applying the IRB measurement method. The IRB method introduces the concept of expected capital loss due to customers' failure to repay EL debt. According to Basel II regulations, credit loss of a credit portfolio can be divided into

into two types: (i) expected losses EL (Expected Losses) and (ii)

Unexpected Losses (UL). For each loan or each customer, EL is determined by the formula:

EL = PD x LGD x EAD

For this approach, determining the risk level of an asset will be based on estimating the parameters:

PD (Probability of Default – probability of customer default).

LGD (Losses Given Default – Expected loss rate).

EAD (Exposure of Default – customer's outstanding debt at the time of default).

OCB may, subject to IRB, use an internal risk measurement model to calculate its risk-based capital requirement. Under this option, OCB must hold capital equal to the potential loss on the institution's equity holdings determined using an internal value-at-risk model (internal VaR Model) with a 99% confidence level of the difference between quarterly returns and an appropriate risk weight calculated over a long-term pilot period.

On that basis, OCB has developed a pricing policy and set up provisions to recover losses for each loan and each customer.

Thus, in order to come up with a capital policy that is necessary to face risks, OCB will have to estimate the level of unexpected losses.

within a certain period of time, from which OCB will estimate the level of economic capital sufficient to compensate for unforeseen losses.

Credit risk management will comply with Basel II management principles by establishing an internal credit rating system to calculate three components PD – probability of customer default, LGD – expected loss ratio (%) in case of customer default and EAD – risk balance. Based on the results of PD, LGD and EAD calculations, OCB will develop applications in credit risk management in many aspects, the first of which is to calculate and measure credit risk through EL – expected loss and UL – unexpected loss at the customer level.

1st: Determine the probability of customer default (PD).

PD is a parameter that measures the probability of a corresponding credit risk occurring over a period of time, usually one year. The basis of this probability is data on past debts of customers, including paid debts, debts in due date and debts that cannot be collected. According to Basel II requirements, to calculate the debt within one year of customers, banks must base on the outstanding debt data of customers within at least 5 previous years. The data is divided into the following 3 groups:

Financial data group related to customers' financial ratios as well as ratings from rating agencies

Non-financial qualitative data group related to management level, ability

research and development of new products, industry leaders.

about

ability

increase

Warning data related to warning phenomena

Signs of default on bank loans such as deposit balances and overdraft limits.

From the above data, the bank enters a predefined model, from which

Calculated probability of non-payment

owed

of the customer. That can be

is the model

linear, probit models and are usually built by professional teams.

private office

problem

2nd: Determine the expected loss of capital (LGD)

LGD is the loss arising on the basis of customer default, described as the percentage of the lost capital on the total outstanding debt at the time.

customer does not pay

owed

(value

nominal loan). LGD

includes not only loan losses but also other losses arising when customers fail to repay their debts, such as interest due but not paid and administrative costs that may arise such as: costs of handling collateral, costs for legal services and other related costs.

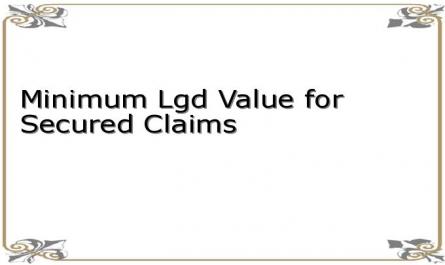

Under the FIRB method, unsecured primary claims on corporates, government agencies and banks will be assigned an LGD of 45%; secondary claims on the above entities will be assigned 75%. For collateralized claims on receivables, mortgages, commercial real estate (CRE) and residential real estate (RRE) and other collateral that satisfy the Basel Committee's criteria in paragraphs 509 to 524, the minimum LGD values described in the following table will apply:

Table 2.11 Minimum LGD for Secured Receivables

Type of collateral

Minimum LGD | |

Qualifying financial assets | 0% |

Accounts Receivable | 35% |

Commercial/real estate residence | 35% |

Other collateral | 40% |

Source: Basel Committee on Banking Supervision 2005, “International Convergence of Capital Measurement and Capital Standards (A Revised Framework).”

3rd: Determine the customer's outstanding balance at the time of default

in debt.

For term loans, EAD is not too difficult to determine.

difficult, but for loans under credit lines and revolving credit, this issue is quite complicated. According to statistics from the Basel Committee, at the time of default, customers often tend to withdraw loans to a level close to the granted limit. Therefore, the Basel II Committee requires calculating EAD as follows:

EAD = Average Outstanding + LEQ x Average Unused Credit Limit

In which, LEQ – Loan Equivalent Exposure is the proportion of unused capital that is likely to be withdrawn by customers at the time of default. LEQ x Average unused credit limit is the outstanding debt that customers will withdraw at the time of default in addition to the average outstanding debt.

In addition to the three components in the formula for calculating the probability of recovery risk (EL) presented in the above sections, when applying the EL formula, banks need to calculate the effective period of payments under credit contracts.

For banks using the facility (FIRB) approach for corporate exposures, the effective maturity (M) is 2.5 years except for repo transactions where M is 6 months. Regulators may decide to require all banks under their jurisdiction (i.e. banks applying the facility and advanced approaches) to measure M for each exposure using the definitions set out below.

The effective maturity M is defined as the greater of one year and the remaining effective maturity in years. In all cases, M shall not be greater than 5 years.

For a tool

extra

belong to a defined schedule of

Cash flow, effective period M is determined as follows:

Validity period M = /

Where CFt refers to the cash flow (principal, interest and fees) that the borrower will receive under the contract.

payable in period t.

2.2.3.3 Risk management

Loan Management

When customers show signs of difficulty in repaying debts, poor financial situation, risks will occur. At that time, the bank will take response measures to limit risks. The bank has a policy of regularly re-evaluating the loan status, loan use, loan security analysis, and customer financial situation, at least once a year. The assessment is carried out by the customer department and the credit risk management department through various sources of documents such as from the customer's financial statements, reports on the use of loans according to commitments, and assessments of other credit institutions that have relationships with the customer. If there is a request for the borrower to make fundamental changes between the estimates made in the credit application and the borrower's performance, especially changes related to the expected cash flow used to repay the debt, the bank requires the customer to explain in detail. The assessment results will be an important basis for the bank to take necessary actions to minimize credit risks related to the loan, including: adjusting credit limits, changing loan contract terms, and terminating the loan contract.

Adjust credit limit: take credit with customer loan.

Adjust loan limit, time

Change the terms of the loan contract: Require customers to add collateral or withdraw collateral based on the outstanding balance and risk of the loan. Require control of customer revenue by transferring customer revenue to OCB account.

Termination of loan contract: Implemented when the customer violates the loan contract by using capital for the wrong purpose, the customer's business situation is unstable, does not guarantee income, and is late in paying periodic debts many times.

Level of Judgment Authorization

To maximize risk management functions, Orient Commercial Joint Stock Bank has 06 levels of decision authorization including:

Credit Council: Approves credit granting to a customer or group of related customers with a maximum limit of 40 billion VND.

Credit Committee: Including Level 3 Committee with maximum approval limit of 20 billion; Level 2 Credit Committee with maximum 50 billion for a customer and related customer group. Level 1 Credit Committee approves credit amounts exceeding the judgment of Level 2 Credit Committee.

General Director: Approves credit of up to 20 billion for a customer or a group of related customers.

Approved personal titles at headquarters: Assigned specifically to each title by the Credit Committee.

Director of corporate and individual customer block/region: The General Director submits to the Credit Committee the assignment of decision-making authority to each specific individual.

Business Unit Directors: General Director assigns judgment

within the scope of the Credit Committee's authorization to the General Director.

(Details in Appendix 03 of the thesis)

Provision for credit risk

During the period 2014 - 2016, OCB strictly implemented the state regulations based on Decision No. 493/2005/QDNHNN and Decision No. 18/2007/QDNHNN. On December 5, 2014, OCB issued Decision No. 383/2014/QD - General Director on "Debt classification and risk provisioning". Accordingly, the provisioning ratio for five specific debt groups is as follows:

Group 1 (standard debt) provision rate 0%

Group 2 (debts requiring attention) provision rate 5%

Group 3 (substandard debt) provision rate 20%

Group 4 (doubtful debt) provision rate 50%

Group 5 (debt with potential loss of capital) provision rate 100%