Maybe you are interested!

-

Current Status of Credit Rating of Corporate Customers at Asia Commercial Joint Stock Bank - Hue Branch

Current Status of Credit Rating of Corporate Customers at Asia Commercial Joint Stock Bank - Hue Branch -

Completing the personal credit rating model at Saigon Commercial Joint Stock Bank - 12

Completing the personal credit rating model at Saigon Commercial Joint Stock Bank - 12 -

Evaluation of Financial Indicators in the Credit Scoring System of Asia Commercial Joint Stock Bank for Corporate Customers

Evaluation of Financial Indicators in the Credit Scoring System of Asia Commercial Joint Stock Bank for Corporate Customers -

Completing credit rating work for corporate customers at Vietnam Maritime Commercial Joint Stock Bank - 1

Completing credit rating work for corporate customers at Vietnam Maritime Commercial Joint Stock Bank - 1 -

Analyze and propose some solutions to limit credit risks at Asia Commercial Joint Stock Bank - 1

Analyze and propose some solutions to limit credit risks at Asia Commercial Joint Stock Bank - 1

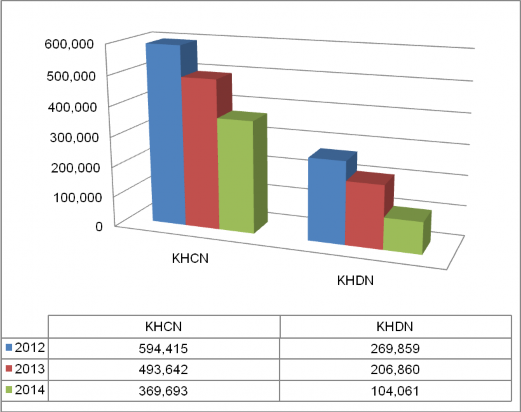

Chart 2.2 – Loan turnover 2012 - 2014

The above data shows that the lending and debt collection turnover of Hue branch gradually decreased in the period 2012 - 2014. The lending turnover in 2013 decreased by 163,774 million VND, equivalent to a decrease of 18.95% compared to 2012; continued to decrease by 226,746 million VND, equivalent to a decrease of 32.369% in 2014. Compared to the proportion of lending to individual customers, corporate customers only account for about 50% due to practical conditions. Hue market mainly focuses on family businesses, private enterprises with small and very small scale, so when approaching customers for loans, large enterprises are often very few. This explains the difference in proportion between lending turnover to individual customers and corporate customers. Debt collection turnover also decreased gradually in the period 2012 - 2014. In 2013, it decreased by 38,059 million VND, equivalent to a decrease of 5.00% compared to 2012. And in 2014, it decreased by 215,151 million VND, equivalent to a decrease of 29.75% compared to 2013. Loan turnover in the period 2012 - 2014 is on the decline, so debt collection turnover decreased significantly in 2014.

Conclusion:

The reason is that since 2012, the State Bank of Vietnam stopped mobilizing and lending in gold, causing ACB - Hue Branch to no longer have a source of gold loans (which originally accounted for a high proportion in ACB's lending structure), so the lending turnover in this period decreased sharply compared to previous years. At the same time, the impact of the economic recession in the period of 2012 - 2013, the production and business situation was poor. Enterprises had a lot of inventory stagnant, faced difficulties in the consumption process and as a result, reduced the scale of production activities. Therefore, the demand for loans was no longer high.

2.1.3.4. Outstanding debt situation

Table 2.5 - Outstanding debt for the period 2012 - 2014 (Appendix 13)

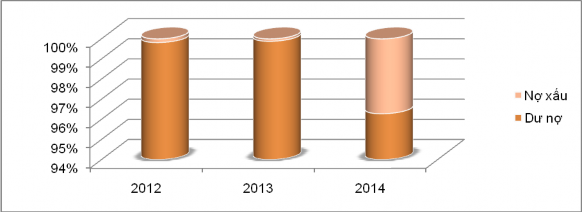

Chart 2.3 – Outstanding debt ratio in the period 2012 - 2014

In credit relations, the occurrence of bad debt is inevitable. Therefore, bad debt is the top concern of banks when granting credit to customers. Although this debt is not completely lost, loans with mortgaged assets and pledges with foreclosure procedures are still cumbersome, costly and time-consuming in debt collection, sometimes lasting until the following year. In the above 3 years, 2014 was the year with the highest overdue debt ratio of 3.86%, accounting for 12,911 million VND, higher than the average bad debt ratio of credit institutions.

According to Prime Minister Nguyen Tan Dung: “According to reports from credit institutions, the bad debt ratio by the end of 2014 was 3.25% and has a decreasing trend (June was 4.17%; July was 4.11%; August was 3.9%; September was 3.8%”). However, these debts were known to ACB Bank – Hue Branch in advance, so provisions were made. However, this result, according to the assessment, exceeded the Board of Directors’ expectations, especially in the difficult situation of the crisis after the 2012 incident.

2.1.3.5. Business performance results

Table 2.6 - Business performance at ACB - Hue Branch in the period 2012-2014 (Appendix 14)

About income

The main sources of income include interest income, including interest from lending activities, interest from deposits at credit institutions and other similar activities. In addition, there are also income sources from service activities, foreign exchange trading and other income sources. In general, the income situation of ACB Hue Branch over the past 3 years has continuously grown in a positive direction. Specifically, total revenue in 2012 reached 83,668 million VND, in 2013 this figure increased to 91,899 million VND, equivalent to an increase of 8,230 million VND (9.84%) compared to 2012. In 2014, total revenue of ACB Hue was 110,125 million VND, equivalent to an increase of 18,226 million VND (19.83%) compared to 2013. Total revenue of the bank has increased continuously over the years, especially in 2014 there was a huge increase in both absolute and relative terms, this reflects the good business situation of ACB Hue Branch. On the one hand, it shows the development of the bank in diversifying products and services, improving the bank's credit activities, besides that, it is also necessary to mention the great efforts of all officers and employees in the bank.

The increase in total income of ACB Hue Branch over the years, especially in 2014, was due to the rapid increase in income from interest and similar items. This was due to the fact that the lending interest rate in 2014 was always much higher than in previous years, usually at an average of 17%/year to 18%/year.

At times, it even reached 21%/year, accompanied by an increase in the competition for mobilization interest rates, continuously breaking the ceiling interest rates, at times reaching up to 15%/year. In 2012, income from interest and similar items reached 79,756 million VND, in 2013, this income increased to 87,441 million VND, equivalent to an increase of 7,685 million VND (9.64%) compared to 2012. In 2014, this figure reached 104,140 million VND, an increase of 16,699 million VND (19.10%) compared to 2013. The increasing growth rate of interest income and similar items over the years has shown that the Branch's credit activities have always achieved good results and developed stably over the years.

About cost:

Along with the increase in income, expenses also increased significantly. Specifically, in 2013, the total expenses were 77,221 million VND, an increase of more than 7,239 million VND compared to 2012, equivalent to 10.34%, and an additional large number of 16,742 million VND (equivalent to 21.68%) in 2013. Of which, interest payments by the bank accounted for the largest proportion in the total expense structure. This expense increased steadily over the years with an increasing speed in both absolute and relative terms. The reason was the increase in capital mobilization costs due to increased interest rates. In 2014, there was a real competition in interest rates among other banks. In return, the capital mobilized by the Bank in the following years also increased significantly. On the other hand, non-interest expenses increase every year because the bank spends more on promotional programs and loyalty programs for customers to attract capital for the business purposes of the unit. In addition, operating costs also increase quite a high proportion, the price index increases, so management costs and salary costs increase to contribute to improving the quality of management work of the bank in particular and the efficiency of business operations in general.

Conclusion: In general, the bank's business activities have always achieved quite good results in the past time because the growth rate of income is always higher than the growth rate of

Cost. It can be said that this is an important factor to ensure the stability of the bank's business operations and an important resource for the development of the bank in all aspects. In the past 3 years, in TT Hue province, there have been more and more competing banks, market prices have fluctuated strongly, the world economic recession has led to negative impacts on the Vietnamese economy... making the business environment of ACB - Hue Branch more difficult and challenging. One of the most prominent difficulties is the competition between banks on deposit interest rates, which has caused the cost of deposit interest to increase, increasing business costs and reducing profits. This is a disadvantage that any bank must accept, requiring banks to have effective operating policies that are competitive enough with other banks in the area.

2.2. Credit process of Asia Commercial Joint Stock Bank - Hue Branch for corporate customers

2.2.1. Related titles

Currently, all credit activities for corporate customers at ACB are uniformly applied according to the "Credit granting process for corporate customers". The main subjects participating in the operational process include:

Distribution channel (KPP) : are Transaction Offices, Branches, and Transaction Offices that perform business tasks according to decentralization or authorization in the ACB system.

Credit review levels: are members assigned by the Chairman of the Board of Directors responsible for reviewing and assessing the risks of customers/loans based on the Re-evaluation Request and the entire credit file. Including: Standing/overall Credit Committee, Group Credit Committee, Headquarters Corporate Credit Committee, Credit Review Specialists at all levels and Branch Credit Committees.

Approval authority : is the maximum credit limit for one, several customers and/or a group of related customers that the authorized person agrees or rejects. Approval authority is according to the hierarchy in ACB's system or by authorization. In which, the approval level is specifically divided into:

Credit approval specialists at all levels: Approval limit according to specialist level, with the director of Hue branch being credit contracts < 1 billion VND and no exception;

Headquarters Corporate Credit Department : Credit contracts <= 50 billion VND and exceptions that are not under the authority of the Branch Credit Department;

Credit Committee Group : 50 billion VND < Credit contract < 200 billion VND and exceptions that are not under the authority of the Head Office;

Standing/full credit committee : Credit contracts >= 200 billion VND and exceptions that are not under the authority of the Group credit committee.

Corporate Customer Relations (R*) : is an employee at distribution channels who is the point of contact with customers, guides and supports customers in completing credit profiles, early identification of credit risks and other tasks related to customer service.

Credit Analyst (C*) : is an employee who performs tasks of assessing customers and their business plans; managing credit quality and performing other tasks related to credit quality.

Legal Document Officer (LDO): is an employee who performs tasks related to the administrative aspect of credit such as: disbursement, opening L/C, performing procedures related to international payments at business units, preparing and monitoring reports related to credit... and performing other tasks related to credit records. Completing necessary procedures for collateral and other tasks related to collateral management.

Asset Appraiser (A/A) : is an employee who performs asset valuation tasks according to ACB's business purposes.

Credit Controller (Loan CSR) : is an employee who performs the task of independently and objectively re-evaluating loans based on the records of the loan officers, guiding the loan officers to improve the quality of credit appraisal; establishing and completing

Improve the system of policies, tools and credit assessment standards to support risk management activities.

Debt collection center : Includes staff performing tasks related to debt collection assigned by NV.QHKH, NV.PTTD (after approval by competent authorities) such as: developing policies, plans, solutions, and handling measures for each debt, proposing management solutions; organizing and implementing problem debt handling; coordinating with relevant departments and functional agencies to propose debt collection measures that bring the highest efficiency to ACB.

2.2.2. Credit process for corporate customers

Table 2.7 – General flowchart of credit process for corporate customers (Appendix 15) Table 2.8 – Detailed flowchart of credit process for corporate customers (Appendix 16)

2.3. Asia Commercial Joint Stock Bank's credit rating system for corporate customers

Corporate credit rating system for credit approval (Scoring Approval): aims to assess the risk of corporate customers and at the same time serve the purpose of credit application approval. Customer rating results are used as one of the bases for making credit decisions, building customer policies and are one of the mandatory documents when submitting credit applications for corporate customers at ACB.

Software used: TCBS Scoring_DN Module

2.3.1. User authorization

The program has three levels of user authorization:

Credit Appraiser:

- Enter and edit customer information at the unit;

- Evaluate and comment on customer profiles;

- View total score and customer classification;

- Export customer scoring results report after being accepted by competent authority.

Control level:

- No right to enter and edit customer information;

- Have the right to view comments on credit officer profiles, view total score results and customer classification;

- Have the right to accept or reject information entered and commented by credit officers;

- Export reports on scoring results for each customer at the unit;

- Have the right to view the number of customers scored by Scoring at the unit according to the status: newly entered, pending processing, accepted and rejected.

Corporate Customer Block:

- Has the same rights as credit officers and controllers;

- Have the right to export all or selective reports of detailed scoring results of all customers in the entire system;

- Have the right to view parameters and detailed results of each scoring indicator of each customer at all units;

- Have the right to adjust the value of the scoring parameters and classify customers.

2.3.2. System information

2.3.2.1. Input information

Level 1: Customer information and comments and reviews are entered by credit assessors.