1.3. Detailed accounting of raw materials in manufacturing enterprises

1.3.1. Documentation procedures for Import - Export of raw materials

The system of documents on raw materials in enterprises applying the enterprise accounting regime is issued under Decision 15/2006/QD/BTC dated March 20, 2006 of the Minister of Finance.

The system of documents on materials according to the issued accounting regime includes:

-Warehouse receipt Form No. 01-VT

-Warehouse delivery note Form No. 02-VT

-Test report Form No. 03-VT

-Remaining materials report at the end of the period Form No. 04-VT

-Inventory report Form No. 05-VT

-VAT invoice (issued by seller) Form No. 01GTKT-3LL

-Regular invoice (made by seller) Form No. 02GTTT-3LL

-Internal delivery and warehouse receipt Form No. 03PXK-3LL

In which, the Inspection Report and the End-of-period Remaining Materials Report are the guiding documents, the rest are mandatory documents.

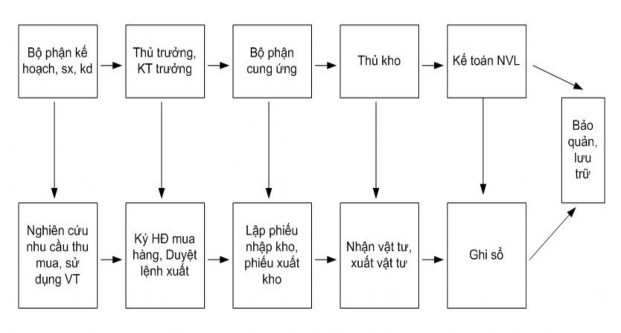

The process of creating and circulating documents about materials is summarized in the following diagram:

Diagram 1: Process of creating and circulating documents to raw materials

1.3.2. Detailed accounting of raw materials

Detailed accounting of raw materials is the tracking and recording of the changes in inventory of each material used in production and business to provide detailed information for managing each material item.

Detailed accounting work must ensure monitoring of inventory import and export according to physical indicators and the value of each material item, and must summarize the circulation and inventory situation of each item according to each warehouse, each counter, and each yard.

Currently, businesses can apply one of three detailed accounting methods for raw materials as follows:

-Parallel card method

-Rolling reconciliation method

-Balance book method

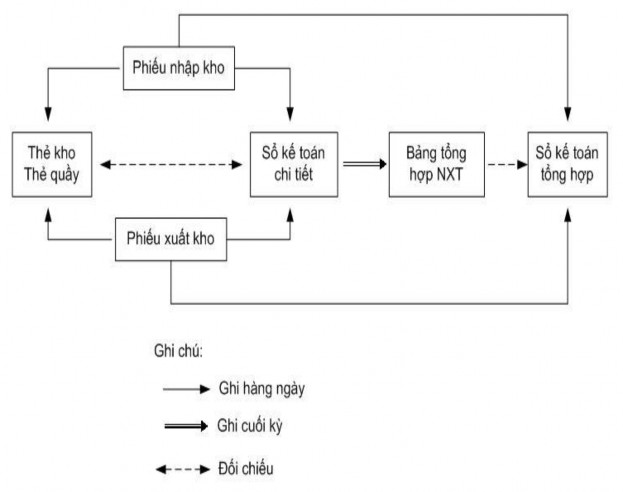

1.3.2.1 Detailed accounting of raw materials using parallel card methodAt the warehouse : The warehouse keeper uses the warehouse card to record the import, export, and inventory status of each material in each warehouse according to quantity criteria.

Every day when receiving documents for import and export of materials, the warehouse keeper checks the validity and legality of the documents and then records the actual import and export numbers on the warehouse card based on those documents.

At the end of the month, the warehouse keeper calculates the total amount of imports, exports and ending inventory of each type of material on the warehouse card and compares the data with the detailed material accounting.

At the accounting department: The accountant opens a book or a material detail card to record the changes in import, export, and inventory of each type of material, both in physical form and in value. Daily or periodically after receiving the documents for import and export of materials submitted by the warehouse keeper, the accountant checks and records the unit price, calculates the amount of money, classifies the documents, and enters them into the material detail book.

At the end of the accounting period, the books are added up and the inventory for each type of material is calculated, and the data in the detailed material accounting books is compared with the corresponding warehouse card. Based on the detailed material accounting books, the accountant takes the data to record in the Material Import and Export Inventory Summary Table.

Diagram 2: Detailed accounting process of raw materials according to parallel card method.

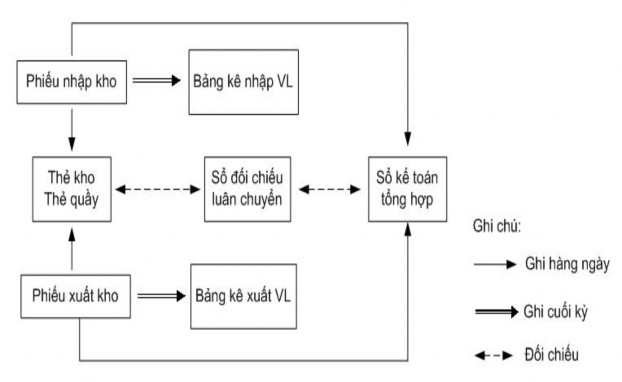

1.3.2.2 Detailed accounting of raw materials using the rotating reconciliation book methodAt the warehouse : The warehouse keeper uses the warehouse card to record like the parallel card method.

At the accounting department: The accountant opens a book to compare the circulation of raw materials by each warehouse. At the end of the month, based on the classification of documents for importing and exporting raw materials by each location and by each warehouse, the accountant makes a list of imported materials and a list of exported materials. Then record it in the circulation comparison book. At the end of the period, the warehouse card is compared with the circulation comparison book.

Diagram 3: Detailed accounting process of raw materials according to the circulation reconciliation book method

1.3.2.3 Detailed accounting of raw materials using the balance sheet method

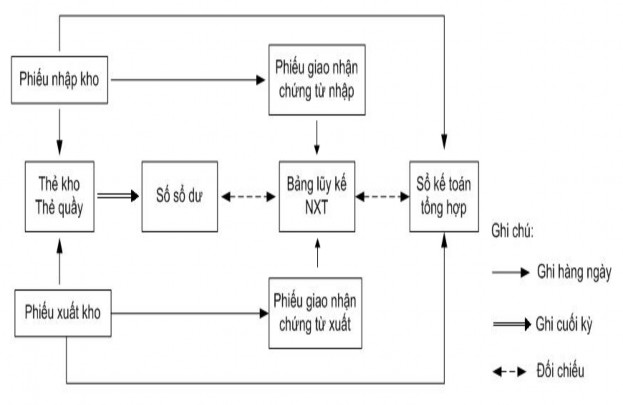

At the warehouse: The warehouse keeper still uses the warehouse card to record the import, export and inventory status. In addition, at the end of the month, the warehouse keeper must also record the inventory quantity on the warehouse card in the Balance Book.

At the accounting department: Every 5 to 10 days, the accountant receives the documents transferred by the warehouse keeper and creates a document delivery and receipt form. Based on that, the accountant creates a cumulative import-export inventory table. At the end of the period, calculate the money on the Balance Book transferred by the warehouse keeper and compare the inventory of each item of raw materials on the balance book with the cumulative import-export inventory table.

Diagram 4: Detailed accounting process for raw materials using the balance sheet method

1.4. General accounting of raw materials

1.4.1. General accounting of raw materials according to the regular declaration method.

General accounting of raw materials according to the regular declaration method is a method of regularly and continuously monitoring the fluctuations in import, export, and inventory of materials in the accounting books.

Using this method, the value of imported, exported, and existing materials can be calculated at any time in the general ledger. In this method, the raw material account is reflected according to the content of the asset account.

This method is often applied in businesses with large raw material values.

1.4.1.1 User account

Account 152 "Raw materials"

This account is used to track the current value, increase and decrease of raw materials according to actual prices. Structure of account 152:

- Debit side :

+ Actual price of raw materials in stock due to purchase, self-production, outsourcing, joint venture capital contribution, provision or import from other sources.

+ Value of excess raw materials detected during inventory.

- Side has :

+ Actual price of raw materials used in production, sale, outsourcing or joint venture capital.

+ Value of raw materials discounted, CKTM or returned to seller.

+ Value of missing raw materials detected during inventory.

- Outstanding Debt :

+ Actual price of raw materials in stock

Account 152 can be opened in detail for each type of raw material depending on the management requirements of the enterprise. Details according to function can be divided into 5 level 2 accounts:

-TK 1521 - Main raw materials

-TK 1522 - Auxiliary materials

-TK 1523 - Fuel

-TK 1524 - Spare parts

- Account 1528 - Other materials Account 151 "Goods purchased in transit"

This account is used to reflect the value of materials that the business has purchased and accepted payment from the seller but has not yet been stored at the end of the period.

Structure of TK 151:

- Debit side :

+ Value of raw materials in transit.

- Side has :

+ Value of raw materials in transit that have been imported into the warehouse or transferred to users.

- Outstanding Debt :

+ Value of raw materials in transit that have not yet been returned to the warehouse.

In addition, the general accounting of raw materials according to the regular declaration method also uses a number of other related accounts such as accounts 111, 112, 133, 141,

331, 515...

1.4.1.2. Accounting method

Below is a diagram of the method of accounting for the synthesis of raw materials according to the regular declaration method, paying VAT according to the deduction method.

Diagram No. 5: General accounting method for raw materials according to regular declaration method, paying VAT according to deduction method.

1.4.2. General accounting of raw materials using the periodic inventory method . The periodic inventory method is a method based on actual inventory results to reflect the ending inventory value in the general accounting book and from there calculate the value of materials and goods exported.

Material value out of stock | = | Material value Beginning balance | + | Total cost of purchased materials in period | - | Material value ending balance |

Maybe you are interested!

-

Completing the accounting of raw materials at Son Thuy Production and Trading Joint Stock Company - 1

Completing the accounting of raw materials at Son Thuy Production and Trading Joint Stock Company - 1 -

Completing the accounting of raw materials for yarn production at Ha Nam Textile Company - 9

Completing the accounting of raw materials for yarn production at Ha Nam Textile Company - 9 -

Completing the management and supply of raw materials at the training equipment manufacturing factory X55 - 7

Completing the management and supply of raw materials at the training equipment manufacturing factory X55 - 7 -

Completing the management and supply of raw materials at the training equipment manufacturing factory X55 - 5

Completing the management and supply of raw materials at the training equipment manufacturing factory X55 - 5 -

Completing Marketing mix activities for tobacco raw materials products of Hoa Viet Joint Stock Company - 1

Completing Marketing mix activities for tobacco raw materials products of Hoa Viet Joint Stock Company - 1

According to this method, any fluctuations in materials are not tracked and reflected in account 152, the value of purchased materials is reflected in account 611 " Purchases ".

This method is often applied in businesses with many types of materials, low value and exported regularly.

1.4.2.1. User account

Account 611 "Purchases":

This account is used to reflect the actual price of materials purchased and issued during the period. Structure of account 611:

- Debit side :

+ Carry over the value of beginning inventory

+ Value of imported materials during the period

- Side has :

+Carry over the value of ending inventory

+Carry over the value of materials issued during the period

Account 611 has no balance at the end of the period, detailed into 2 sub-accounts:

- Account 6111 "Purchase of raw materials"

- Account 6112 "Purchase of goods" Account 152 "Raw materials", 151 "Goods purchased in transit"

- Debit side :

+ Value of inventory and transit materials at the beginning of the period

+ Value of inventory and transit materials at the end of the period

- Side has :

+ Carry over the value of inventory and transit materials at the beginning of the period

1.4.2.2. Accounting method

Below is a diagram of the method of accounting for the synthesis of raw materials according to the periodic inventory method, paying VAT according to the deduction method.

Diagram No. 6: General accounting of raw materials according to periodic inventory method, paying VAT according to deduction method.

1.5. Accounting system used in material accounting

1.5.1. For businesses applying the Journal - Ledger form .

- Journal - Ledger;

- Detailed accounting books and cards.

Diagram No. 7: Sequence of accounting for raw materials in the form of Journal - Ledger

1.5.2. For businesses applying the General Journal form.

- General journal, Special journal;

- Ledger;

- Detailed accounting books and cards.

Diagram No. 8: Sequence of accounting for raw materials in the form of General Journal

1.5.3. For businesses applying the form of Bookkeeping vouchers.

- Recording vouchers;

- Register of accounting vouchers;

- Ledger;

- Detailed accounting books and cards.

Diagram 9: Accounting sequence for raw materials in the form of accounting vouchers

1.5.4. For businesses applying the form of Journal - Voucher .

- Voucher log;

- List;

- Ledger;

- Detailed accounting books or cards.

Diagram No. 10: Sequence of accounting for raw materials in the form of Journal - Voucher