credit expansion. 7 By the end of December 2012, the outstanding balance of SBV loans to commercial banks through refinancing channels and open market operations that have not yet matured was VND 221,112 billion, equivalent to 7.33% of the total outstanding credit balance in VND of the entire system; The balance of mobilized capital of Vietnamese commercial banks from the interbank market was VND 762,527 billion, equivalent to 18.92% of the outstanding credit balance of the economy. The scale of the interbank market by the end of December 2012 was

1,331,066 billion VND equivalent to 38.3% of the total outstanding debt of the entire system shows: A large amount of capital flows around the interbank market, creating interdependence between commercial banks; Systemic risk is very large when the market fluctuates suddenly; The market forms a group of banks specializing in investing and lending to other commercial banks to make a profit and a part of commercial banks depends on capital sources of the interbank market.

(2) Excessive lending leads to a very high capital utilization ratio of Vietnamese commercial banks, exceeding the safety level: By the end of December 2012, the ratio of total outstanding credit for the economy compared to capital mobilization from the economy was 100.4%; If other investments (investment, capital contribution, purchase of corporate bonds, other receivables) are included, the total investment of the entire system for the economy is 3,813,591 billion VND, equal to 113% of capital mobilization from the economy. Excessive lending leads to low liquidity reserves, commercial banks have to borrow from the State Bank or borrow from abroad to finance credit growth. This ratio is 110.6% for VND and 124.2% for foreign currency (the difference between credit and mobilization in foreign currency is financed by foreign currency mobilized from abroad).

7 Reports of the State Bank of Vietnam to 2012

Table 2.36: Comparison of Vietnam's loan-to-deposit balance with some other countries

Countries in the world

Nation

Outstanding_deposits (%) | |

China | 11.8 |

India | 13.6 |

Indonesia | 17.6 |

Malaysia | 16.4 |

Pakistan | 13.6 |

Philippines | 16.7 |

Thailand | 15.5 |

Argentina | 16.5 |

Brazil | 18.2 |

Chile | 13.6 |

Peru | 13.2 |

Venezuela | 12.6 |

Armenia | 20.4 |

Russia | 17.2 |

Ukraine | 19.2 |

Vietnam | 104 |

Maybe you are interested!

-

Analysis of financial capacity and some solutions to improve financial capacity at Vietnam Telecommunications Technology Investment and Development Joint Stock Company - 5

Analysis of financial capacity and some solutions to improve financial capacity at Vietnam Telecommunications Technology Investment and Development Joint Stock Company - 5 -

The Impact of the Global Financial Crisis on Vietnam's Economy

The Impact of the Global Financial Crisis on Vietnam's Economy -

Government's financial and monetary policies for the development of small and medium enterprises. Experiences of countries around the world and lessons for Vietnam - 13

Government's financial and monetary policies for the development of small and medium enterprises. Experiences of countries around the world and lessons for Vietnam - 13 -

Some Features of Vietnam's Financial Services Market Integration Process

Some Features of Vietnam's Financial Services Market Integration Process -

Bad Debt Ratio of Vietnam's Credit Institution System

Bad Debt Ratio of Vietnam's Credit Institution System

Source: World Bank report up to 2012[21]

(3) Unstable capital structure and capital use; Serious imbalance in terms between capital sources and capital use. In the total capital mobilized from the economy by the end of December 2012, non-term capital and capital with a term of less than 6 months accounted for 77.77% of the total capital mobilized from payment sources (of which: 79.44% for VND and 71.52% for foreign currency), making the capital source unstable: Meanwhile, medium and long-term credit balance accounted for 42.4% of the total credit balance (of which: 41.48% for VND and 45.47% for foreign currency) 8 leading to weak liquidity of commercial banks .

(4) Low solvency ratios: The maturity gap between liabilities and assets is large and the risk of short-term insolvency of Vietnamese commercial banks is high. The solvency of Vietnamese commercial banks is generally significantly lower than that of foreign commercial banks.

(5) Highly liquid assets to meet low maturing debt obligations limit the ability to respond to mass withdrawals. Total assets have

8 Summary from financial statement explanations of commercial banks up to 2012

VND has high liquidity as of December 2012 at 604,234 billion VND, equivalent to only the balance of non-term deposits in VND of the entire system.

+ Low capital adequacy ratio of commercial banks: By December 2012, the average capital adequacy ratio of the whole system was 11.37%. The capital adequacy ratio of Vietnamese commercial banks has not fully complied with international standards (Basel II) and is lower than that of many other developing countries, while many banking systems in the world have international capital adequacy ratios (Basel II) higher than the current standards applied in Vietnam.

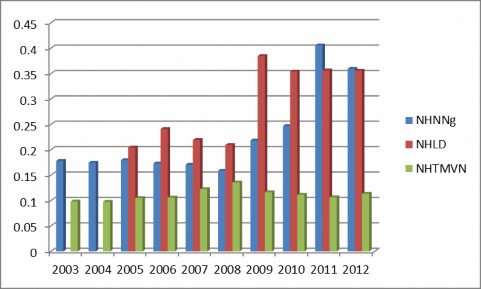

Table 2.37: Comparison of CAR ratios of

Vietnam's commercial banking system with the National Bank for Foreign Trade of Vietnam from 2003-2012

Year

CAR (%) | |||

SBV | NHLD | NHTMVN | |

2003 | 17.83 | 09.83 | |

2004 | 17.46 | 09.78 | |

2005 | 17.97 | 20.47 | 10.48 |

2006 | 17.33 | 24.10 | 10.61 |

2007 | 17.08 | 21.95 | 12.27 |

2008 | 15.89 | 20.95 | 13.57 |

2009 | 21.85 | 38.48 | 11.66 |

2010 | 24.68 | 35.44 | 11.16 |

2011 | 40.57 | 35.63 | 10.67 |

2012 | 35.96 | 35.59 | 11.37 |

Source : Author's calculation from financial statements of Vietnamese commercial banks_NHLD-NHNNg[22,23]

Chart 2.19: Comparison of CAR index of the system

Vietnamese commercial banks with foreign banks and joint stock commercial banks in the period from 2003 to 2012

Source : Author's calculation from financial statements of Vietnamese commercial banks_NHLD-NHNNg[22,23]

Through the data in Table 2.37 and Chart 2.19, it can be seen that the capital safety ratio of the commercial banks and foreign banks is superior to that of the Vietnamese commercial banking system. The higher this index is, the higher the safety in banking business, once again showing the lack of sustainability and safety in banking business of the commercial banks of the Vietnamese commercial banks compared to the commercial banks and foreign banks. To ensure the safety of the entire Vietnamese commercial banking system, the system needs to increase the CAR ratio.

- The number of commercial banks is large, but a large number of commercial banks have many potential risks, unhealthy finances, low competitiveness and are vulnerable when the business environment changes. As of the end of December 2012, 22 commercial banks had charter capital of less than VND5,000 billion; 10 commercial banks had assets of less than VND30,000 billion.

- The number of Vietnamese commercial banks is large but not strong, many commercial banks operate unprofessionally, contain many risks and weaknesses. The synchronous and serious implementation of Resolution No. 11/NQ-CP dated February 24, 2011 in the monetary and banking sector has exposed inherent weaknesses and unhealthy commercial banks. Liquidity difficulties are only an external manifestation of serious internal weaknesses in the capacity, management efficiency, finance and business of those commercial banks. These weak commercial banks are one of the important reasons for the market

money market disorder (high interest rates, unfair competition, violations of law, disruption of discipline, market discipline).

Chapter 2 Conclusion

From the contents presented and analyzed in chapter 2 with the purpose of assessing the current status of the financial capacity of the Vietnamese commercial banking system, does it meet the Camel safety framework? And the factors affecting the financial capacity of the Vietnamese commercial banking system, some conclusions can be drawn as follows:

(1) Introduction to the history of the formation of the Vietnamese banking industry after many years of innovation and development.

(2) Analyze the current financial capacity of the Vietnamese commercial banking system, as a basis for in-depth analysis according to the Camel safety framework. The assessment results show that the financial capacity of the Vietnamese commercial banking system has not yet met the Camel safety framework, there are still many weaknesses such as low equity capital scale, bad debt ratio increased significantly compared to previous years and is very large compared to the NHLD-NHNNNG, business efficiency is lower than some banks of other countries in the world, only focusing on traditional products, so it is necessary to improve the financial capacity of the Vietnamese commercial banking system from the perspective of each bank, the State Bank and the Government.

(3) Overview of 14 factors affecting financial capacity, arguments and hypotheses, from which to propose a research model.

(4) Probit regression results show that there are 13 factors affecting the financial capacity of Vietnamese commercial banks. Identifying the above mentioned factors affecting financial capacity is the scientific basis for providing convincing solutions in the next chapter 3.

CHAPTER 3

ADVANCED SOLUTIONS

FINANCIAL CAPACITY FOR COMMERCIAL BANKING SYSTEM

3.1. PURPOSE OF DEVELOPING THE SOLUTION

After studying the aspects directly and indirectly related to the financial capacity of Vietnamese commercial banks using qualitative and quantitative methods. The purpose of chapter 3 is based on the scientific foundations shown to build a system of synchronous solutions to increase the financial capacity of Vietnamese commercial banks in the coming period. At the same time, identify the factors that really affect the financial capacity of Vietnamese commercial banks and forecast that the financial capacity of Vietnamese commercial banks will increase when affecting the influencing factors, from which banks need to have effective solutions to promote financial capacity to overcome the risk of failure to achieve sustainable development. Specifically:

- Increase equity capital by increasing charter capital and combining banks with the same conditions and scale, converting debt into equity.

- How to effectively handle bad debt, this is a factor that has an adverse impact on the financial capacity of Vietnamese commercial banks, so we must focus on resolving bad debt by all possible measures.

- Increase liquidity during operations by synchronously combining solutions.

- Review the lending process as well as the personnel involved in applying this process to continue lending to reputable and effective customers and limit credit growth for ineffective customers.

- Use assets and financial leverage effectively

- Recommend to the Government and the State Bank to have a more effective mechanism to manage and supervise banks.

3.2. PROPOSED VIEWPOINT FOR SOLUTIONS

3.2.1. On the strategic development orientation of the Industry

3.2.1.1. For foreign credit institutions operating in Vietnam

- Comply with the provisions of the Vietnam-US Trade Agreement, other bilateral agreements with Japan, the EU, WTO regulations and international commitments on opening the financial and banking services market. Continue to proactively loosen restrictions on market access and banking operations of foreign credit institutions in Vietnam according to the committed roadmap. Both create opportunities for foreign credit institutions to operate legally according to international commitments and have flexible, legal and international practice-compliant management methods and mechanisms to limit manipulation, unfair competition or disadvantageous takeovers of Vietnamese credit institutions by foreign credit institutions.

3.2.1.2. For domestic credit institutions

Develop a multi-functional credit institution system in a modern direction, operating safely, effectively and firmly with a diversified structure in terms of ownership, scale and type with greater competitiveness based on a technological platform, advanced banking management in accordance with international practices and standards on banking activities to better meet the needs of financial and banking services of the economy; Enhance the competitiveness of Vietnamese commercial banks.

3.2.2. About the industry's goals

Restructuring the system of credit institutions to overcome difficulties and weaknesses and proactively deal with challenges so that credit institutions can continuously develop safely, effectively and firmly and meet the requirements of socio-economic development in the new period.

Strengthen and develop a system of credit institutions with diverse ownership, scale and type suitable to the characteristics and development level of the Vietnamese economy in the current period.

Encourage mergers, consolidations, and acquisitions of credit institutions on a voluntary basis, ensuring the rights of depositors, and the economic rights and obligations of related parties in accordance with the provisions of law.

Carry out comprehensive restructuring of finance, operations and administration of credit institutions in appropriate forms, measures and roadmaps.

Do not let banking operations collapse and become unsafe beyond the control of the State.

3.3. BASIS FOR PROPOSED SOLUTION

3.3.1. Based on the orientation and development strategy of the banking industry in the period 2011-2020

Based on Decision 254/QD-TTg dated March 1, 2012 of the Prime Minister on approving the Project on restructuring the system of credit institutions for the period 2011-2-15. Showing the strategy of the Industry:

- Develop a multi-functional credit institution system in a modern direction, operating safely, effectively and firmly with a diverse structure in terms of ownership, scale, and type with greater competitiveness based on a technological platform, advanced banking management in accordance with international practices and standards on banking operations to better meet the needs of financial and banking services of the economy;

- Improve the financial situation and strengthen the operational capacity of credit institutions, improve order, discipline and market principles in banking activities to achieve the goal of having 2 banks with scale and level equivalent to regional banks by 2015.

3.3.2. Based on the lessons learned in chapter 1

In the study of chapter 1, section 1.6.1, some key notes can be drawn in the study of NLTC of commercial banks, which are:

- Lessons on financial market liberalization

European countries, the US, and Japan have liberalized financial markets to facilitate the movement of capital flows from one country to another by floating foreign exchange transactions; floating interest rates, interest rates are determined on the basis of supply and demand in the market, the State only participates in the role of macro-regulation without direct intervention.

- Lessons on improving financial capacity

Commercial banks in China set goals in their strategy to strengthen their competitiveness such as: Building a financially autonomous banking mechanism; Improving information infrastructure to become a global bank with international capital management capabilities.