VND; in turn to Joint Stock Commercial Bank for Foreign Trade of Vietnam (Vietcombank)

23,174 billion VND; Joint Stock Commercial Bank for Investment and Development of Vietnam (BIDV) 23,011 billion VND; Joint Stock Commercial Bank for Industry and Trade of Vietnam (Vietinbank) 20,229 billion VND.

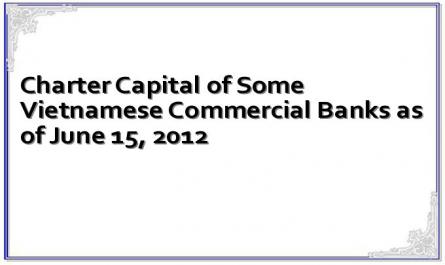

The entire system currently has 34 joint stock commercial banks. According to the State Bank of Vietnam, by the end of June 2012, there were still 2 banks, PG Bank and Bao Viet Bank, with charter capital of less than 3,000 billion VND, the remaining 32 banks had all increased to or exceeded 3,000 billion VND. Of these, 11 banks have just reached the 3,000 billion mark, 12 banks have charter capital from over 3,000 to 5,000 billion VND, 7 banks have from over 5,000 billion to 10,000 billion VND and only 3 banks have charter capital of over 10,000 billion VND.

Table 2.3: Charter capital of some Vietnamese commercial banks as of June 15, 2012

Unit: Billion VND

TT

Commercial Bank | Charter capital | |

1 | Agribank | 29,606 |

2 | Vietcombank | 23,174 |

3 | BIDV | 23,011 |

4 | Vietinbank | 20,229 |

5 | Eximbank | 12,355 |

6 | Sacombank | 10,740 |

7 | SGBank | 10,583 |

8 | ACBank | 9,376 |

9 | TechcomBank | 8,788 |

10 | MSBank | 8,000 |

11 | MBank | 7,300 |

12 | LienViet Post Bank | 6,400 |

13 | SeAbank | 5,334 |

14 | VPBank | 5,050 |

15 | OceanBank | 5,000 |

Maybe you are interested!

-

The impact of foreign bank penetration on competition and efficiency of Vietnamese commercial banks - 21

The impact of foreign bank penetration on competition and efficiency of Vietnamese commercial banks - 21 -

Increasing capital mobilization from individual customers of commercial banks - Case study of Vietnam Joint Stock Commercial Bank for Investment and Development, Phu Tho Branch - 1

Increasing capital mobilization from individual customers of commercial banks - Case study of Vietnam Joint Stock Commercial Bank for Investment and Development, Phu Tho Branch - 1 -

Solutions to enhance capital mobilization at Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch - 9

Solutions to enhance capital mobilization at Lien Viet Post Joint Stock Commercial Bank - Hai Phong Branch - 9 -

Completing the appraisal of loans for additional working capital for corporate customers at Vietnam Joint Stock Commercial Bank for Industry and Trade - Dong Anh Branch - 5

Completing the appraisal of loans for additional working capital for corporate customers at Vietnam Joint Stock Commercial Bank for Industry and Trade - Dong Anh Branch - 5 -

Testing the credit risk tolerance of Vietnamese commercial banks - Case study of Vietnam Joint Stock Commercial Bank for Industry and Trade - 21

Testing the credit risk tolerance of Vietnamese commercial banks - Case study of Vietnam Joint Stock Commercial Bank for Industry and Trade - 21

Source:[28],[33],[34],[35],[36],[37],[38],[39],[40],[41],[42],[43],[44],[45]

Equity capital is an indicator reflecting financial capacity, ensuring the competitiveness in the operations of commercial banks and creating trust with the public. However, currently, the charter capital of most Vietnamese commercial banks is still very small, including

State-owned commercial banks. Low equity means weak financial strength and poor ability to withstand risks in business operations. This is one of the important conditions for Vietnamese commercial banks to improve their competitiveness.

The financial capacity and scale of operations of Vietnamese commercial banks are generally low compared to banks in the region and according to international practice. Due to low equity capital, the capital safety ratio is low. However, in the past 5 years, the rapid growth in capital scale has helped the Vietnamese commercial banking system significantly improve its financial capacity and this ratio. By the end of 2007, the CAR ratio of many Vietnamese commercial banks had exceeded the requirement set by the State Bank for the target by 2008. Typical examples include VCB, ACB, Sacombank, BIDV, MHB... On average, the CAR ratio of State-owned commercial banks increased from 7% in 2006 to 9% in 2007. The minimum capital adequacy ratio in 2009 of the entire State-owned commercial banking sector was 7.46%, down from the end of 2008 (this ratio was 9.2%) because some banks had to exclude capital contributions and share purchases from their equity capital. The minimum capital adequacy ratio of joint-stock commercial banks was higher, averaging over 12%.

The capital adequacy ratio not only reflects the capital capacity of banks in static form but also shows this capacity in relation to capital usage efficiency.

According to the report as of December 31, 2010, the capital safety ratio of commercial banks, most banks operating in Vietnam ensure the minimum capital safety ratio, except for State-owned commercial banks, specifically:

- State-owned commercial banks: 3/5 banks have capital safety ratio below 8% and only MHB ensures minimum capital safety ratio.

- Joint stock commercial banks: 3/37 joint stock commercial banks, accounting for 8.1%, have a capital safety ratio of less than 9%, and 25/37 banks, accounting for 67.6%, have a ratio of equity capital to risky assets of 12% or more.

- Joint venture banking sector: 100% of banks ensure capital safety ratio, the bank with the lowest Capital Safety Ratio reaches 16.86%.

- Foreign banking sector: the bank with the lowest capital safety ratio is 21.66 % .

Table 2.4: Capital safety ratio of Vietnam's commercial banking system as of December 31, 2010

NH Block

<8% | 8% to under 9% | 9% to under 12% | >12% | |

State-owned commercial banks, specifically: | 3/5 | 1/5 | 0 | 1/5 |

- Vietinbank | 7.44% | |||

- Vietcombank | 7.03% | |||

- Agribank | 6.09% | |||

- BIDV | 8.14% | |||

- MHB | 13.24% | |||

Joint Stock Commercial Bank Block | 1/37 | 2/37 | 9/37 | 25/37 |

Source: [28],[34],[35],[36],[37]

The financial strength of a bank is expressed through its equity capital, and at the same time, its equity capital determines the scale of its operations, and is the basis for the bank to conduct business, attract other sources of capital and lend. It is considered a "cushion" to support the decrease in the value of bank assets, helping commercial banks avoid bankruptcy. In 2012, to strengthen internal strength and avoid acquisitions, many small banks wanted to increase their capital immediately. According to experts, raising more capital is a good option, but in this context, doing it massively will cause great risks for the bank itself. The content of "increasing charter capital" appeared in the 2012 Annual General Meeting of Shareholders of most banks. NamA Bank increased its capital from 3,000 billion to 3,700 billion, Orient Bank increased from 3,234 to 4,000 billion while VietAbank and ABBank's plans were both up to 5,000 billion. DongA Bank, although having just completed its capital increase to 5,000 billion, is expected to still issue 1,000 billion in charter capital to existing shareholders to increase to 6,000 billion.

According to experts in the banking sector, their capital increase is welcome and encouraging. The reason why banks are rushing to increase capital this year is to strengthen their internal strength and expand their lending capacity. For banks, the larger their equity capital, the more they can mobilize, limit

The higher the credit limit granted, the more likely it is that small banks will seek ways to increase their charter capital.

Not only small banks, but also large banks want to increase capital. Sacombank's leaders said that in 2012, they will increase their charter capital by 17% (about 1,700 billion VND) to raise their charter capital from 10,047 billion to more than 11,700 billion VND. ACB also increased its capital from 9,377 billion VND to 12,377 billion VND from undistributed profits, reserve funds to supplement charter capital and from public offering of shares.

However, according to many experts, the desire to increase capital may stem from high bad debt and the risk of being acquired or merged. For many weak banks, when bad debt is critical and the possibility of losing capital is high, they will want to increase capital even more. This may not be reflected in the books, but weak banks understand very well how bad debt is "eating" into equity. When the wave of M&A (mergers and acquisitions) takes place strongly, bank owners themselves, especially listed banks, also see the risk of being acquired. Increasing capital will be a way to cope. However, not only small banks at risk of being acquired need to increase capital, but the acquiring party also needs "strong" capital to have strength when participating in negotiations.

Normally, banks increase capital by issuing more shares or paying dividends in shares. However, in 2012, the difficult economic situation combined with the sluggish stock market made it difficult to convince existing shareholders to buy more shares or to successfully offer shares to the public. Many banks had planned to increase capital since last year but had not completed it and had to postpone it to next year for this reason.

2.2.1.2. Business performance of the Vietnamese Commercial Banking system

In 2012, the economy faced many difficulties, economic production activities stagnated, thus banking risks increased and the business efficiency of banks decreased. This also accurately reflected the economic situation.

According to the report data of commercial banks in 2012, commercial banks paid interest on deposits and loans of about 408 trillion VND, and collected interest on loans from the economy of about 420 trillion VND. Meanwhile, the difference between revenue and expenditure of the entire banking sector in 2012 is estimated at more than 20 trillion VND, the lowest level since 2008 and also only nearly equivalent to the level of

The difference between revenue and expenditure in 2008 was only about 40% of the level in 2011. The difference between revenue and expenditure in the entire banking industry in 2012 decreased mainly due to the difference between output and input interest rates, increased risk provisioning costs, and low credit growth.

The business performance indicators (ROA, ROE) in 2012 of commercial banks were all lower than in previous years. As of December 31, 2012, the ROA (Profit before tax compared to assets) ratio of the whole system reached 0.48% and ROE reached 3.97%. Of which, the average ROA and ROE ratio of State-owned commercial banks was 0.76% and 11.37%; the average ROA and ROE ratio of joint-stock commercial banks was 0.22% and 1.36%; the average ROA and ROE ratio of joint-venture banks and foreign banks was 0.91% and 5.08%, respectively.

Table 2.5: Business performance of Vietnam's commercial banking system

Unit: Billion VND, %

Type of credit institution

2012 | 2013 | |||

ROA | ROE | ROA | ROE | |

State Commercial Bank | 0.76 | 11.37 | 0.45 | 5.28 |

Joint Stock Commercial Bank | 0.22 | 1.36 | 0.28 | 3.05 |

Source: [28], [66]

2.2.1.3. Capital Adequace Ratio (CAR)

According to analysis and assessment by experts in the field of banking and finance in Vietnam and by international financial organizations, one of the limitations of the Vietnamese banking system is small equity capital and low minimum capital adequacy ratio (CAR). However, in recent years, the increase in capital scale has helped banks significantly improve the CAR ratio. Although the minimum capital adequacy ratio (CAR) of Vietnamese commercial banks is still lower than that of other countries in the region, it has been raised.

If the average CAR ratio of commercial banks in 2010 was 10.98%, then in 2011 and 2012 it increased to approximately: 11.62% and 13.75% respectively. By the end of 2013, the minimum capital adequacy ratio (CAR) of Vietnamese commercial banks was approximately 13.76%. In general, the minimum capital adequacy ratio meets the regulations (≥ 9%), however, there are different fluctuations among groups of commercial banks (Table 1.9).

The minimum capital adequacy ratio (CAR) by 2013 of the group of State-owned commercial banks is 11.31%, joint-stock commercial banks is 12.81%, joint-stock banks and foreign banks is 30.82%. According to calculations and assessments of economic experts, there are still some banks with minimum capital adequacy ratio (CAR) below the prescribed level.

Table 2.6: Minimum capital adequacy ratio of Vietnam's commercial banking system

Unit: %

Year

2010 | 2011 | 2012 | 2013 | |

State Commercial Bank | 7.09 | 9.06 | 10.28 | 11.31 |

Joint Stock Commercial Bank | 14.8 | 12.99 | 14.01 | 12.81 |

Whole system | 10.98 | 11.62 | 13.75 | 13.76 |

Source: [28], [64]

2.2.2. Current status of distribution channel system of Vietnam Commercial Banking system

2.2.2.1. Number and distribution of areas

In recent years, especially after Vietnam became an official member of the WTO, the number of commercial banks has increased rapidly. Currently, the commercial banking system nationwide has 50 commercial banks and 51 foreign bank branches.

Although the number of commercial banks is relatively large, they are unevenly distributed, mainly concentrated in two key economic areas: Hanoi and Ho Chi Minh City.

Chart 2.1: Distribution proportion (headquarters) of Vietnam's commercial banking system in 2013

10%

35%

55%

Hanoi

Ho Chi Minh City

Other locations

Source: [28], [64]

2.2.2.2. Network operations

Regarding the number of branches, transaction offices and transaction offices: As of 2013, the Vietnamese commercial banking system has a total of 2,059 branches and transaction offices; with more than 5,212 transaction offices. Thus, on average, each commercial bank has about 40 branches and 106 transaction offices; 1 commercial bank branch has 2.5 transaction offices. Of which:

- The State-owned commercial bank sector has the largest operating network with 1,299 branches and 3,329 transaction offices, accounting for 63.09% of the entire system.

- The joint stock commercial bank block has 760 branches and 1,883 transaction offices, accounting for 36.91% of the entire system.

2.2.2.3. About branch allocation

The operating network of the Vietnamese commercial banking system is quite dense but is only concentrated in large, densely populated cities such as Ho Chi Minh City, Hanoi, Can Tho, Da Nang... Among the current credit institutions, the Vietnamese commercial banking system (State-owned commercial banks and joint-stock commercial banks) is leading in terms of operating network. The group of commercial banks with foreign elements has almost no change in operating network with a total of more than 30 branches in the past few years. 100% foreign-owned banks currently only account for a small number of operating network hubs but have shown great ambition and development potential. After just over 02 years of operation, 05 100% foreign-owned banks have had 14 branches in major provinces and cities across the country and the demand for network expansion of this group is still very large.

2.2.2.4. About market share

Chart 2.2: Market share structure of mobilization

Unit: %

100%

1 8 . . 3 8

30.4

1 8 . . 7 1

33.1

7 2 .5

40.8

1 6 . . 6 6

1 7 . . 7 6

46.7

47.1

50%

59.5

57.1

49.7

45.1

43.6

0%

Source: [28]

Chart 2.3: Credit market share structure

Unit: %

100%

3.8

9.2

4.4

11

4.8

9.1

6

9

4.6

8.6

80%

27.7

26.5

32

33.14

35.5

60%

40%

59.3

58.1

54.1

51.86

51.3

20%

0%

Source: [28]

Statistics from the State Bank show that, if at the end of 2007, the State-owned commercial banks (Agribank, Vietcombank, Vietinbank, BIDV, MHB) still dominated both lending and deposit market share, respectively 59.3% and 59.5%; then by the end of 2013, it was only 51.36% and especially the deposit market share was only 45.29%.

The reason is that the joint stock commercial banking sector has had a "Thanh Giong process" in terms of scale, especially during the boom period of the stock market in 2006 - 2007, creating such a strong shift in market share.

However, throughout 2011-2013 and the first quarter of 2014, the above market share structure did not change much; even the State-owned commercial banks tended to rebound in the lending market share. After the rapid encroachment of the joint-stock commercial banks from 2008-2010, the picture of Vietnam's banking market share has been relatively stable for over a year, or rather, there has been a clear tug-of-war. In the past two years, there has been and is witnessing a rapid expansion in scale. In 2012, Agribank's charter capital was nearly tripled compared to 2010, which was 29,606 billion VND (in 2010, it was 10,200 billion VND). Vietcombank and Vietinbank, after being "untied" by equitization, also continuously increased their capital scale; the prospect is BIDV when it has just been equitized...