Analysis of Vn-Index Stock Price Index Fluctuations

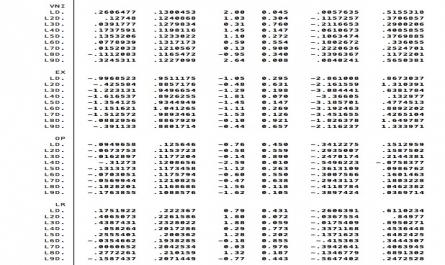

𝑌 𝑡 = 𝛽 1 + 𝛽 2 𝑋 2𝑡 +. . +𝛽 𝑘 𝑋 𝑘𝑡 + 𝑢 𝑡 (1) In which the explanatory variables can include lagged variables of other explanatory variables or lagged variables of the dependent variable. When model (1) has autocorrelation, it means that the random errors u at ...