monetary policy tools in implementing the inflation targeting framework.

2.4.1. China's experience

2.4.1.1. Before joining the World Trade Organization (WTO)

In the late 1990s, China faced strong devaluation pressure due to the impact of the financial and monetary crisis in the region. To reduce the pressure to adjust and devalue the Renminbi during this period, in parallel with maintaining the stability of the Renminbi, China applied a series of flexible monetary and financial support policies, in which the foreign exchange control policy played a very important role.

In 1997, in order to protect the Renminbi (RMB) from the impact of the regional crisis, China paid great attention to the flow of foreign currency in and out of the country. On August 1, 1998, China ordered banks to prohibit foreign currency trading of more than 5 million USD/year to control foreign currency.

China has conducted a review and inspection of the foreign exchange situation of local agencies and enterprises, requiring them to return unused foreign currency to the state for management. At the same time, it has inspected and detected cases of enterprises violating the order to store undeclared foreign currency reserves in order to promptly prevent foreign currency loss and increase foreign exchange reserves (FORE).

To protect the RMB from attacks by international speculators, in June 1999, the People's Bank of China (PBoC) announced new regulations, prohibiting overseas trading of RMB to limit the possibility of speculation in RMB.

As early as 2000, the State Administration of Foreign Exchange and the General Administration of Customs of China assessed whether enterprises with import activities really needed to use hard currency. At the same time, Chinese banks stopped selling foreign currency in payment activities such as: payment activities for barter trade and offset trade. Banks also stipulated additional mandatory conditions for selling foreign currency to enterprises importing raw materials, accessories and enterprises importing equipment for hire-purchase activities. However, the above strict regulations on foreign exchange purchase do not apply to foreign-invested enterprises importing raw materials for processing and re-export. Thus, companies with foreign trade cooperation can buy hard currency from banks.

Thanks to these efforts, the RMB exchange rate against the USD remained almost fixed throughout the late 1990s. When the economies of the

After the regional currencies stabilized, the PBoC loosened the trading band of the RMB. The loosening of the trading band of the RMB was piloted in mid-2000, and in January 2001, China announced that it would let the RMB fluctuate within a band of about 1%. This announcement showed that the period of fixed exchange rate adjustment had begun to end. These measures helped China become more flexible and proactive in adjusting its exchange rate in response to fluctuations in regional currencies.

China's mechanism for managing the exchange rate during this period can be considered a great success. Specifically:

China's foreign exchange reserves increased rapidly, from 52.22 billion USD (in 1990) to 90 billion USD in 1994, reaching 104 billion USD in 1996. In 2000, foreign exchange reserves (FER) increased to 165 billion USD and ranked second in the world in FER (only after Japan);

RMB is freely convertible in current account, the reputation of RMB is increasing, RMB is gradually moving towards free conversion in capital account;

Create a foundation for China to integrate more deeply into the world economy in terms of currency.

Thus, with foreign exchange reform measures and flexible adjustments to the RMB exchange rate throughout the 1990s, China has gradually affirmed the RMB as a relatively strong currency in the region, supported by the second largest volume of foreign exchange reserves in the world. This is also a success in the practice of operating the exchange rate mechanism of China.

2.4.1.2. Since joining the WTO (2001) to present

Faced with the challenges posed to the economy after joining the WTO, China continues to implement a managed floating exchange rate mechanism.

The huge capital inflows into China have put upward pressure on the RMB. To control the RMB, the PBOC has to buy foreign currency, increasing liquidity for the banking system. As a result, banks have excess reserves, so the measure of increasing the required reserve to 7.5% that the PBOC introduced in April 2004 for banks and above has lost its effect. In October 2004, China's foreign exchange reserves were 540 billion USD (an increase of more than 40% compared to the beginning of the year). During this time, on the basis of building a unified foreign exchange market, the Chinese government has also gradually loosened the trading band of the RMB against the USD.

The above measures of the PBOC have limited the appreciation of the RMB and kept the currency low for a long time, helping to encourage China's exports. However, the undervaluation of the RMB is the cause of the trade deficit (BCD) of major partners with relations with China such as the US, Japan, and the EU. China's devaluation of the RMB makes Chinese goods abroad unfairly cheap, causing disadvantages not only to the US but also to the G7 countries. Therefore, countries have unanimously called on China to consider adjusting the exchange rate more flexibly (raising the price or floating the RMB in the capital account). But China has not accepted it.

On July 21, 2005, the PBoC decided to increase the value of the RMB by 2.1% against the USD, from 8.28 RMB/USD to 8.11 RMB/USD, ending a decade of maintaining a fixed exchange rate of the RMB against the USD. China announced the adoption of a managed floating exchange rate mechanism, the RMB will be managed by referring to a basket of currencies, or in other words, the peg of the RMB to the USD will end.

On August 9, 2005, the PBoC officially announced the names of 11 currencies in the currency basket, including: US dollar (USD), Euro (EUR), Japanese Yen (JPY), Korean Won (KRW), Singapore dollar (SGD), British pound (GBP), Malaysian Ringgit (MYR), Russian ruble (RUB), Australian dollar (AUD), Thai baht (THB), and Canadian dollar (CAD). The reason for choosing the above currencies comes from the great influence of these countries on China's current account balance. After that, China has made continuous efforts to form and develop spot, swap and forward markets, expanding the fluctuation range from 0.3% (in 2005) to 0.5% (in 2007), in order to create a more flexible and market-oriented basis for the exchange rate. The RMB appreciated steadily until 2008, when the government and the PBOC decided to return to the peg mechanism.

In July 2008, when statistics showed that exports had dropped by 16%, thousands of factories producing export goods were forced to close, and about 20 million foreign workers working here lost their jobs, all due to the impact of the global financial crisis, China decided to stop the RMB's appreciation. The exchange rate was kept relatively stable at 6.8 RMB/1 USD.

On June 19, 2010, with the domestic and international economic situation stabilizing, the PBoC announced the return to a managed floating exchange rate regime by appreciating the RMB, resulting in a 6% appreciation of the RMB. On March 17, 2014, the PBoC widened the exchange rate band between the RMB and the USD from 1% to 2%. This was the third adjustment since the implementation of the policy.

exchange rate reform (July 2005), contributing to increasing the flexibility of RMB exchange rate.

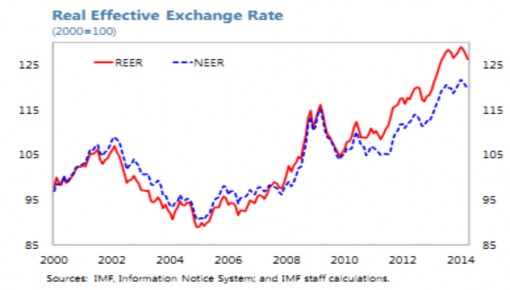

Figure 2.4: Real effective exchange rate of RMB, 2000-2014

Source: IMF (2014)

According to the PBoC, widening the band is beneficial to enhancing the flexibility of the exchange rate, enhancing the role of the market, promoting adjustment and transforming China's economic development mode. On the one hand, the PBOC still controls the fluctuations of the RMB exchange rate, on the other hand, gradually increasing the marketization level of the RMB exchange rate: The official RMB exchange rate is determined daily with the increase and decrease determined by supply and demand in the interbank market.

On August 11, 2015, China announced the transition from a crawling band exchange rate to a managed floating exchange rate. The China Foreign Exchange Trade System (CFETS) sets the reference exchange rate at the beginning of each trading session based on the previous day's interbank closing exchange rate and on supply and demand in the currency market and the movements of major currencies. The fluctuation range is still maintained at +/-2%.

In 2015, after three consecutive days (August 11, 12, 13), the average exchange rate announced by PBoC increased by 4.66%. On August 25, 2015, PBoC injected 150 billion RMB (23.4 billion USD) into the financial system through reverse repurchase agreements (repo), causing the RMB to continue to decrease by 0.2% against the USD. These developments had a significant impact on the international financial market in general and Vietnam in particular.

On November 30, 2015, the IMF's Executive Board completed its regular review (every 5 years) and decided that the RMB would be included in the SDR basket (Standard Drawing Rights basket).

(special) of the IMF because it has met both current criteria and is effective from October 1, 2016. Specifically:

- RMB meets export criteria : China is the world's third largest exporter of goods and services, and is considered the "gateway" to the IMF's SDR.

- Along with USD, EUR, JPY, GBP, RMB is considered "freely usable", meaning that the currency is actually commonly used in international payments and is widely traded in major foreign exchange markets.

The IMF's decision to include the RMB in the SDR basket is an important milestone in China's integration into global finance. The IMF also recognizes the progress in reforming the financial and monetary systems that the Chinese government has made in recent years, which has helped support growth and stability in China and the global economy.

* The impact of RMB becoming an international reserve currency. It is difficult to accurately assess the importance of RMB being included in the SDR basket for the entire international monetary system. First of all, it affects the country itself:

+ The RMB becoming a strong currency will contribute to reducing exchange rate risks, reducing transaction costs of trade, investment, financial services, foreign debt... of China due to reduced dependence on USD and other strong currencies (Euro, JPY, GBP).

+ Create confidence for investors and businesses, thereby reducing foreign capital flight from China due to fluctuations in exchange rates and the stock market.

+ China's monetary policy will become more complicated in the context of more liberalized capital transactions, which will also reduce the independence of the central bank in operating monetary policy. China's capital balance will loosen and therefore China will have more challenges in controlling capital flows into/out of the economy, as well as ensuring macroeconomic stability.

On exchange rate management according to China's central exchange rate mechanism

China has been operating according to the central exchange rate since January 4, 2006 (10 years before Vietnam). Up to now, China still applies this exchange rate management mechanism, however, it has been adjusted by PBoC many times to suit market fluctuations. In the early period of applying the central exchange rate mechanism, the central exchange rate (TGTT) of RMB was the spot exchange rate on the interbank market and the buying and selling exchange rate at banks. Up to now, the function of the central exchange rate of RMB has been adjusted, it is only the spot exchange rate on the interbank market and the reference basis for banks to set their transaction exchange rates, no longer playing the role of the buying exchange rate.

sold at banks as before.

The number of currencies in the basket of foreign currencies determining the central rate of RMB has gradually increased: The China Foreign Exchange Center is the unit that announces the exchange rate. Every day, at 9:15 a.m., the China Foreign Exchange Center will announce the exchange rate between RMB and 12 foreign currencies, including: USD, British pound (GBP), euro (EUR), Japanese yen (JPY), Hong Kong dollar (HKD), Malaysian ringgit (MYR), Russian ruble (RUB), Australian dollar (AUD), Canadian dollar (CAD), New Zealand dollar (NZD), Singapore dollar (SGD) and Swiss franc (CHF). Compared to the time of application, PBoC has added 8 more foreign currencies to the basket of foreign currencies determining the central rate of RMB. Previously, China only announced the exchange rate between RMB and 4 foreign currencies: USD, EUR, JPY and HKD.

Since August 11, 2015, the central rate between RMB/USD has been determined by the State Administration of Foreign Exchange of China based on three main factors: i) The closing RMB/USD exchange rate on the interbank market on the previous trading day; ii) The foreign exchange supply and demand situation of the market; iii) Exchange rate fluctuations of some important foreign currencies. At the same time, on December 11, 2015, PBoC announced the proportion of currencies in the currency basket. Accordingly, the RMB measure will be priced according to the currency basket of 12 currencies, in which the proportion of major trading partners is the main (USD: 26.4%, EUR: 21.39%, JPY: 14.68% and HKD: 6.55%). In January 2017, China increased the number of currencies in the basket to 24 and the weights were calculated specifically for each currency (Table 2.3).

Table 2.3. Structure and proportion of currencies in the currency basket to calculate the exchange rate of the Chinese Yuan (RMB)

TT

Coin | Proportion (%) | TT | Coin | Proportion (%) | |

1. | USD | 22.40 | 13. | THB | 2.91 |

2. | EUR | 16.34 | 14. | ZAR | 1.78 |

3. | JPY | 11.53 | 15. | KRW | 10.77 |

4. | HKD | 4.28 | 16 | AED | 1.87 |

5. | GBP | 3.16 | 17. | SAR | 1.99 |

6. | AUD | 4.40 | 18. | HUF | 0.31 |

7. | NZD | 0.44 | 19. | PLN | 0.66 |

8. | SGD | 3.24 | 20. | DKK | 0.40 |

9. | CHF | 1.71 | 21. | SEK | 0.52 |

10. | CAD | 2.15 | 22. | NOK | 0.27 |

11. | MYR | 3.75 | 23. | TRY | 0.83 |

12. | RUB | 2.63 | 24. | MXN | 1.69 |

Maybe you are interested!

-

Competitiveness of Vietnam's international travel businesses after Vietnam joins the World Trade Organization WTO - 2

Competitiveness of Vietnam's international travel businesses after Vietnam joins the World Trade Organization WTO - 2 -

Vietnam - Cambodia trade relations after Vietnam joined the World Trade Organization (WTO) - 2

Vietnam - Cambodia trade relations after Vietnam joined the World Trade Organization (WTO) - 2 -

Promoting Vietnam's service exports as a member of the World Trade Organization WTO - 23

Promoting Vietnam's service exports as a member of the World Trade Organization WTO - 23 -

Assessment of the World Trade Organization's Dispute Settlement Mechanism for Developing Countries

Assessment of the World Trade Organization's Dispute Settlement Mechanism for Developing Countries -

Opportunities and Challenges of International and Regional Economic Integration for Vietnam's Foreign Trade

Opportunities and Challenges of International and Regional Economic Integration for Vietnam's Foreign Trade

Source: Zhang Bin, RMB Exchange Rate: Moving Towards a Floating Regime [209]

However, compared to the early period, the RMB/USD central rate is determined in a simpler way. Before the opening of the interbank foreign exchange market each day, the China Foreign Exchange Trading Center will collect quotes from rate-setting organizations, use them as the basis for calculating the central rate, eliminate the highest and lowest quotes, and then determine the RMB/USD central rate of that day. Meanwhile, at present, the RMB central rate for currencies such as EURO, HKD, CAD is determined by the China Foreign Exchange Trading Center based on the RMB/USD central rate and the USD rate for these currencies in the international foreign exchange market at 9:00 a.m. each day. The central rate of RMB for the remaining foreign currencies such as GBP, JPY, RUB, MYR... is still determined by the China Foreign Exchange Trading Center based on the average of quotes from rate-setting organizations at the time before the opening of the interbank foreign exchange market.

Diversifying the fluctuation range of the central exchange rate: PBoC does not stipulate a common fluctuation range for all central exchange rates with currencies in the basket of currencies used to calculate the daily exchange rate, but divides it into many different levels.

In 2016, the spot exchange rates of the exchange rate groups in the interbank market, the RMB/USD exchange rate can fluctuate within the range of + 2% of the central rate of RMB/USD, the RMB/MYR and RMB/RUB exchange rates fluctuate within the range of + 5% of the central rate of RMB/MYR, RUB; while the exchange rate fluctuation range of the remaining foreign currencies is + 3% of the central rate.

Regarding the RMB/USD exchange rate traded at commercial banks, in previous years, the daily exchange rate at Chinese banks was controlled by the PBoC, based on the regulations on the margin difference between foreign exchange buying and selling rates, specifically: First, the difference between the lowest transfer buying rate and the highest transfer selling rate must not exceed 1% of the central rate; Second, the difference between the lowest cash buying rate and the highest cash selling rate must not exceed 4% of the central rate; Third, the difference between the highest selling rate and the lowest buying rate must include the central rate. However, since July 2014, the above regulation has been relaxed, accordingly, banks in China are allowed to proactively price foreign exchange buying and selling based on the market supply and demand and their pricing capabilities without being subject to the PBoC's management limits.

In 2019, in theory, China's exchange rate mechanism is a managed floating exchange rate mechanism, but before June 2018, the International Monetary Fund (IMF) classified China's exchange rate mechanism as a pegged exchange rate mechanism with an adjustment range, and from June 22, 2018 to present, it is an Other managed exchange rate mechanism.

In summary, China's exchange rate management mechanism is quite flexible, ensuring that foreign currency supply is maintained regularly, aiming at the goal of sustainable economic development. China strives to make the RMB a freely convertible currency and is determined not to sharply devalue the currency but only gradually adjust it according to the roadmap. China maintains a flexible exchange rate management mechanism, combining devaluation at necessary times, combined with reform of the foreign exchange management mechanism, which has increased foreign currency reserves and made it the world's largest foreign currency reserve.

2.4.2. Thailand's experience

Before the Asian Financial Crisis (AFC) in 1997-1998, Thailand maintained a fixed exchange rate mechanism, anchoring the Baht to a basket of currencies of its trading partners (including the USD at 80% of its value). The currency crisis in 1997-1998 forced the Bank of Thailand (BOT) to use a large source of foreign exchange reserves (FERs) to intervene. In addition, the situation of domestic financial institutions borrowing short-term foreign loans to invest in long-term real estate was very common. Therefore, on July 2, 1997, the Thai government was forced to strongly devalue the Baht, the exchange rate increased from 25.61 USD/Baht to 47.25 USD/Baht and also in July 1997, the BOT announced the switch to a managed floating exchange rate mechanism and the goal of monetary policy was to control inflation (core inflation target). The result of this change in monetary policy and exchange rate management helped Thailand stabilize the macro economy, stabilize prices and promote economic growth. However, managing monetary policy by volume (anchored to money supply) has disadvantages such as: instability between money supply and economic growth, uncertain credit growth, posing risks to the financial sector... Therefore, in May 2000, the BOT switched to operating monetary policy according to inflation targeting. Inflation targeting plays a key role in monetary policy, while exchange rates are flexibly adjusted, avoiding shocks to the economy.

The Bank of Thailand established the Monetary Policy Committee (MPC) to help implement the inflation targeting monetary policy mechanism. The MPC's task is to establish monetary policy to stabilize prices and economic growth, announce the expected annual inflation rate and based on the actual situation, this core inflation is allowed to fluctuate from 0.5-3.5%. The transition to this new monetary policy mechanism - inflation targeting monetary policy helps Thailand adapt promptly to domestic and foreign fluctuations, while ensuring a stable inflation rate over a long period of time. During this period, the Baht sometimes depreciated by 40% and had a trade surplus [1].