to 72.81%. In 2013, the bad debt of this component was 1,894 million VND, down 401 million VND, equivalent to a decrease of 17.47%, accounting for 86.72% in the bad debt structure of the branch.

Considered by debt groups:

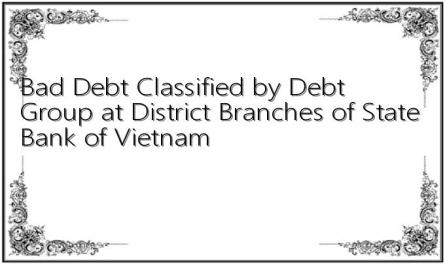

- Group 3 debt at the branch in 2011 was 688 million VND, accounting for 18.51%, in 2012 it was 748 million VND, an increase of 60 million VND with an increase rate of 8.72%. In 2013, bad debt of this group was 519 million VND, a decrease of 30.61% compared to 2012, accounting for 23.76% of total bad debt.

- Group 4 debt in 2012 was 993 million VND, an increase of 63 million VND compared to 2011 with an increase rate of 6.77%. In 2013, bad debt in this group was 405 million VND, a decrease of 588 million VND, with a decrease rate of 59.21% - a significant decrease.

- Group 5 debt accounts for the highest proportion of total bad debt. In 2011, outstanding debt in group 5 was 2,099 million VND, decreasing to 1,411 million VND in 2012, a decrease of 688 million VND, equivalent to a decrease of 32.78% compared to 2011. In 2013, group 5 debt continued to decrease to 1,260 million VND, accounting for 57.69% of total bad debt.

Chart 2.8: Bad debt classified by debt group at the district branch of NHNo&PTNT

Dien Khanh Khanh Hoa (2011-2013)

million dong

2,500

2,000

1,500

1,000

500

0

2011

2012

2013

GROUP 3 GROUP 4 GROUP 5

The cause of bad debt is due to customers facing risks in business,

Disease and crop failure led to failure to repay bank loans on time as committed.

Besides, there are some cases where the appraisal work is not strict enough.

The monitoring and supervision of loans is not timely, leading to bad debt.

However, the decrease in bad debt at the branch over the years shows more caution in assessing loan applications at the branch in the difficult economic situation, which greatly affects banking activities. However, group 5 debt accounts for the highest proportion of total bad debt in recent years, also bringing many risks of losing business capital, increasing the risk provision cost for the branch.

2.2.3 Other service activities:

- Guarantee: Guarantee sales in the period of 2013 were 122 items with the amount of

17,177 million VND, an increase of 10,369 million VND compared to 2012. Fees collected from guarantee activities were 158 million VND.

- Domestic money transfer service: 2013 turnover was 176,840 items, amount of 2,666,769 million VND, fee collected in the year was 1,289 million VND, increased compared to 2012 by 115 million VND.

- Western Union money transfer: in 2013, the branch achieved a payment turnover in USD of 232,497 USD, payment in VND of 1,982 million VND, and commission earned was 64 million VND.

- Foreign exchange trading activities with purchase turnover in 2013 of 239,261 USD, sales turnover of 239,635 USD.

- Issuing ATM cards: in 2013, the branch issued 2,557 new domestic debit cards, 51 new international debit cards and 10 new international credit cards.

- Electricity bill collection service: 2013 revenue reached 2,638 million VND.

- Credit security: in 2013, the number of insured customers was 1,337 with insured loan turnover reaching 34,918 million VND, an increase of 28,269 million VND compared to 2012.

The development of ATM cards has been carried out quite well each year, however, the number of cards issued has not yet reached the assigned plan. Customers who open cards are mainly employees at state agencies and businesses in the district who have opened accounts at the branch. Local people do not have the habit of using cards.

In payment activities, the demand for opening debit cards and credit cards is still low. Other service activities have slow development and low revenue.

2.2.4 Business performance results:

Table 2.8: Business performance results at NHNo&PTNT branch

Dien Khanh district, Khanh Hoa (2011-2013)

Unit: million VND

INDICATORS

2011 | 2012 | 2013 | 2012/2011 | 2013/2012 | ||||

+/- | % | +/- | % | |||||

Total income | 89,723 | 88,596 | 74,483 | -1.127 | -1.26 | -14.113 | -15.93 | |

In there | + Loan interest income | 45,513 | 38,673 | 20,788 | -6.840 | -15.03 | -17.885 | -46.25 |

+ Capital transfer fee | 41,043 | 46,144 | 39,421 | 5.101 | 12.43 | -6.723 | -14.57 | |

+ Service fee | 1,720 | 1,993 | 2,297 | 273 | 15.87 | 304 | 15.25 | |

Total cost (excluding wage) | 63,746 | 65,755 | 52,331 | 2.009 | 3.15 | -13.424 | -20.42 | |

In there | + Deposit interest payment | 53,561 | 56,416 | 43,946 | 2,855 | 5.33 | -12,470 | -22.10 |

+ Loan interest payment | 3.905 | 2,458 | 1,318 | -1.447 | -37.06 | -1.140 | -46.38 | |

+ Risk provision credit risk | 869 | 1.001 | 317 | 132 | 15.19 | -684 | -68.33 | |

Difference between revenue and expenditure (not included) salary calculation) | 25,977 | 22,841 | 22,152 | -3.136 | -12.07 | -689 | -3.02 | |

Maybe you are interested!

-

Solution Group on Bad Debt Monitoring and Handling Violations of Vietnam's Commercial Banking System

Solution Group on Bad Debt Monitoring and Handling Violations of Vietnam's Commercial Banking System -

Limiting social insurance debt of businesses by applying sanctions Case study of businesses in Thanh Xuan district, Hanoi city - 12

Limiting social insurance debt of businesses by applying sanctions Case study of businesses in Thanh Xuan district, Hanoi city - 12 -

Views on Bad Debt of Commercial Banks:

Views on Bad Debt of Commercial Banks: -

The Impact of Bad Debt on the Operations of Credit Institutions

The Impact of Bad Debt on the Operations of Credit Institutions -

Bad Debt Management Vietnam Joint Stock Commercial Bank for Industry and Trade

Bad Debt Management Vietnam Joint Stock Commercial Bank for Industry and Trade

(Source: Branch's business performance summary report

Bank for Agriculture and Rural Development of Dien Khanh district, Khanh Hoa)

Total revenue and total non-salary expenses have decreased over the years due to the decrease in lending interest rates and capital mobilization interest rates according to the roadmap of the State Bank.

Total revenue in 2012 was VND 88,596 million, down VND 1,127 million at a rate of

down 1.26% compared to 2011, in 2013 it decreased sharply to 74,483 million VND, down

14,113 million VND, a decrease of 15.93% compared to 2012.

Total non-salary expenses have fluctuated over the years. In 2012, the total expenditure was VND65,755 million. Although the branch tried to cut spending on unnecessary activities, expenses still increased, specifically VND2,009 million compared to 2011, mainly due to an increase in interest payments on deposits of VND2,855 million due to increased mobilized capital. In 2013, expenses decreased to VND52,331 million, partly due to higher interest rates.

The decrease in interest expense on deposits and the cost of credit risk provision also decreased.

significantly reduced.

The decrease in income combined with fluctuating costs over the past 3 years has caused the branch's profits to decrease. The output interest rate is still high while the economy is still facing many difficulties, causing businesses and production households to reduce production and not boldly borrow from banks. Meanwhile, the branch has not fully utilized the mobilized capital while having to pay interest on the mobilized capital, causing the difference between revenue and expenditure in 2012 to decrease sharply to 3,136 million VND, equivalent to a decrease of 12.07%, but in 2013 the value decreased less, decreasing by 689 million VND, equivalent to a decrease of 3.02%.

Although the economic and financial situation in recent years has been unfavorable and has encountered many difficulties, the branch has made great efforts to complete the tasks of the superior bank.

Chart 2.9: Business performance at the branch

million dong

NHNo&PTNT Dien Khanh district, Khanh Hoa (2011-2013)

100,000

90,000 | ||

80,000 | ||

70,000 | ||

60,000 | ||

50,000 | ||

40,000 | ||

30,000 | ||

20,000 | ||

10,000 | ||

0 | ||

2011 2012 | 2013 | |

Total income | Total cost (excluding salaries) | Difference between income and expenditure (excluding salary) |

2.3 Analysis of the current status of consumer lending activities at the branch of NHNo&PTNT, Dien Khanh district, Khanh Hoa:

2.3.1 Legal basis for consumer lending at the branch of NHNo&PTNT Dien Khanh district, Khanh Hoa:

Pursuant to Decision No. 1627/2001/QD-NHNN dated December 31, 2001 of the Governor of the State Bank of Vietnam on promulgating regulations on lending by credit institutions to customers; Decision No. 28/2002/QD-NHNN dated January 11, 2002; Decision No. 127/2005/QD-NHNN dated February 3, 2005 and Decision No. 783/2005/QD-NHNN dated May 31, 2005 of the Governor of the State Bank of Vietnam on supplementing a number of articles of Decision No. 1627/2001/QD-NHNN.

The State Bank of Vietnam (SBV) issued Circular 01/2009/TT-NHNN providing guidance on agreed interest rates of credit institutions for lending capital needs for living purposes.

Pursuant to the charter of organization and operation of the Vietnam Bank for Agriculture and Rural Development issued together with Decision No. 117/QD - BOD - NHNo dated June 3, 2002 of the Board of Directors of the Vietnam Bank for Agriculture and Rural Development approved by the Governor of the State Bank in Decision No. 571/QD - NHNN dated June 5, 2002.

Vietnam Bank for Agriculture and Rural Development issued Decision No. 666/QD-HDQT-TDHo dated June 15, 2010, with regulations on lending to customers in the Vietnam Bank for Agriculture and Rural Development system.

And other documents of Vietnam Bank for Agriculture and Rural Development (Agribank) on lending

consumer loan

According to document No. 1090/NHNo-TD of NHNo&PTNT, Khanh Hoa province branch, regarding: Guidance on implementing loans to serve personal needs without collateral, debt repayment source from salary, allowances and other income paid by the working unit.

Because the Dien Khanh District Bank for Agriculture and Rural Development (DNNPTNT) of Khanh Hoa is a branch under the Khanh Hoa Province Bank for Agriculture and Rural Development (Khanh Hoa Province Bank for Agriculture and Rural Development), all lending activities are carried out in accordance with the directives of the superior bank, namely the Khanh Hoa Province Bank for Agriculture and Rural Development (Khanh Hoa Province Bank for Agriculture and Rural Development).

2.3.2 Regulations on lending activities of the branch of the Bank for Agriculture and Rural Development of Dien Khanh district, Khanh Hoa:

2.3.2.1 Consumer lending process implemented at NHNo&PTNT branch

Dien Khanh district, Khanh Hoa:

Control

loan

Loan Controller

Decide on handling measures through inspection and supervision

Loan Approver

Loan Approval

Diagram 2.3: CVTD process implemented at the branch of NHNo&PTNT, Dien Khanh district, Khanh Hoa:

Receive and guide customers on loan applications

Appraisal of loan conditions

Prepare loan appraisal report

Loan Appraiser

TSBD warehouse

TSBĐ warehouse export

Dealer

- Accounting for imported fixed assets

- Loan disbursement.

- Profile management.

Check and monitor loans

Collect interest and principal

Release of collateral

Manager

loan

Storekeeper

Proposed measures for handling through inspection and supervision

The loan approval process must go through 3 independent stages:

- Loan appraiser (applicant)

- Loan Controller

- Loan approver

The consumer loan approval process at the Bank for Agriculture and Rural Development of Dien Khanh district, Khanh Hoa is as follows:

Receive and guide customers on loan application: Appraisal officer

responsible

- Guide customers to create profile

- Compare and receive documents

Appraisal of loan conditions: The appraisal officer is responsible for:

- Check the validity and legality of loan documents and loan purposes

- Investigate, collect, and synthesize information about customers and loan options.

- Find information through the National Credit Information Center - CIC, check transaction history and evaluate the customer's credit relationship with the branch as well as with other banks and credit institutions.

- Analyze and evaluate loan customers regarding legal capacity and ability

civil conduct and financial capacity

- Appraisal of plans to serve living needs and debt repayment ability

- Appraisal of assets securing loans

Prepare loan appraisal report: Loan appraisal officer must prepare loan appraisal report, which specifies the results of the appraisal process, proposes to grant or deny the loan. Propose loan amount, interest rate, loan term and other contents about the loan or reasons for refusing to grant the loan.

Loan Control: The loan controller is the Head (Deputy Head) of the Business Planning Department at the center, or the Head of the credit team at the transaction offices. The loan controller controls the legality, validity, and completeness of the loan application, controls the content of the appraisal report of the staff.

assess and recommend granting or denying the loan or requesting further clarification on the loan.

Loan approval: The person who approves the loan is the Branch Director (Deputy Director), the Transaction Office Director (Deputy Director). The person who approves the loan will base on the loan file, appraisal report, credit council meeting minutes (if any) to decide whether to grant the loan or not, or request further reports on the loan.

In case the loan exceeds the authority, the loan approver shall

Loan agreement and presentation to superior bank.

The maximum time limit for appraisal and approval of consumer loans is from

From the date of receipt of complete documents, the required information is as follows:

- Short and medium term loans: maximum 3 working days.

- Long term loans: up to 7 working days

Once the loan is approved, the administrator is responsible for notifying the customer of the competent authority's decision to grant or deny the loan.

For approved loans, the loan manager prepares the credit contract and loan guarantee contract; proposes loan disbursement; enters and updates data in the loan file into the system, ensuring that the paper file and the file on IPCAS match.

Disbursement: After the documents have been completed and meet the disbursement conditions, they will be transferred to the teller to carry out the loan disbursement procedures according to the regulations of the Vietnam Bank for Agriculture and Rural Development. The teller is responsible for receiving and managing the documents handed over by the credit department and accounting for the following operations: mortgage, lending, debt collection, interest collection, fees, and mortgage release.

Checking and supervising loans: The bank has the responsibility and right to check and supervise the process of borrowing, using loans and repaying debts of customers to urge customers to properly and fully implement the commitments agreed in the credit contract and loan guarantee contract. Specifically: