Customers often care about and consider when deciding to use the bank's services. SCB is a latecomer in the credit card business, so SCB's fee and interest rate policies must have more incentives and be more competitive than banks that already have a market share in order to attract customers.

Benefit factor: is the second factor that positively affects the decision to use credit cards at SCB, with β 1 = 0.186; meaning that when the assessment of the benefits that credit card services at SCB bring increases by one unit, the probability of deciding to use will increase by 0.186. Customers are interested in using credit cards, in addition to the fact that it is a modern means of payment, it also brings many benefits to customers, showing superiority over other forms of payment. Therefore, in addition to the benefits of credit card characteristics in general, SCB must constantly increase card utilities and have preferential policies when using payment to maximize benefits for customers, attracting customers to use credit cards at SCB.

Bank image factor: besides the factors of product and service characteristics, the bank image and brand are the next factors that customers are interested in, with β 7 = 0.182; meaning that when the evaluation of SCB's image and brand increases by one unit, the probability of deciding to use it will increase by 0.182. Currently, SCB is on the path to rebuilding its image and brand after the merger, so this factor is even more important when SCB enters a new market.

Convenience factor: Along with the benefit factor, the convenience factor is also considered by customers when using credit cards, with β 2 = 0.140; meaning that when the assessment of the convenience that SCB credit cards bring increases by one unit, the probability of deciding to use them will increase by 0.140. Currently, credit cards are considered by issuing banks and customers as a modern means of payment, so in addition to the benefits it brings, the convenience of using SCB credit cards is also an issue that customers often care about.

Marketing policy factor: according to the model results, this is the least important factor in influencing the decision to use the card at SCB. However, for SCB, the credit card is a newly issued product, so this is the first important factor to provide information about the product and determine the distribution channel to customers. Based on this information, customers will consider and evaluate the above factors to make a decision to use, with β 6 = 0.110; meaning that if SCB's marketing policies increase by one unit, the probability that customers will decide to use will increase by 0.110.

Β 1 = +0.186

Β 2 = +0.140

Β 5 = +0.357

Β 6 = +0.110

Decision to use

(SUPPLY)

Β 7 = +0.182

Cost (CHIP)

Demographic composition

Gender (GT), Age (DT), Marital status (HN), Occupation (NN), Education level (TĐ) and Income (TN)

Benefits (Benefits)

Convenience

Marketing Policy (MAR)

Bank Image (HANH)

Figure 2.3: Results of the research model after adjustment

2.2.3.4 T-test and Anova

One – sample T-test

Use T-test to compare the mean values of the components of the influencing factors to the mid-scale score value (No opinion = 3) to evaluate customers' feelings when evaluating these factors.

The test results show that, according to the current assessment of the study, customers' perception of the factors affecting the decision to use credit cards at SCB is not high, with a significance level of Sig = 0.000 in all variables (including 5 variables), although the average results are higher than the midpoint of the scale but do not reach the value of Agree = 4 in the survey questionnaire.

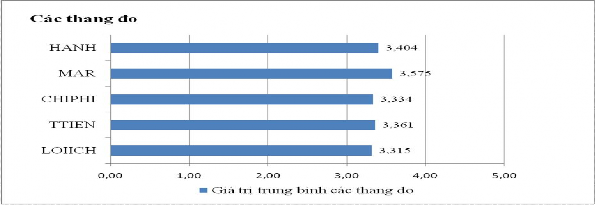

Table 2.13: Average values of factors affecting composition

Mean parameter test

Test value = 3 | ||||

Factor | Average value | Statistics | Significance level | Standard deviation |

LOIICH | 3,315 | 8,946 | 0.000 | 0.6867 |

TTIEN | 3,361 | 10,456 | 0.000 | 0.6722 |

CHIPHI | 3,334 | 10,191 | 0.000 | 0.6383 |

MAR | 3,575 | 17,840 | 0.000 | 0.6283 |

HANH | 3,404 | 10,953 | 0.000 | 0.7181 |

Maybe you are interested!

-

Factors affecting the debt repayment ability of corporate customers at Vietnam Joint Stock Commercial Bank for Investment and Development - Long An Branch - 1

Factors affecting the debt repayment ability of corporate customers at Vietnam Joint Stock Commercial Bank for Investment and Development - Long An Branch - 1 -

Factors affecting customer satisfaction with the quality of international money transfer services at Dong A Commercial Joint Stock Bank - 1

Factors affecting customer satisfaction with the quality of international money transfer services at Dong A Commercial Joint Stock Bank - 1 -

Factors affecting customer loyalty to international payment services at Asia Commercial Joint Stock Bank - 12

Factors affecting customer loyalty to international payment services at Asia Commercial Joint Stock Bank - 12 -

Factors affecting card acceptance of Kien Long Joint Stock Commercial Bank - 18

Factors affecting card acceptance of Kien Long Joint Stock Commercial Bank - 18 -

Factors affecting the decision of customers to deposit savings at Asia Commercial Joint Stock Bank - 1

Factors affecting the decision of customers to deposit savings at Asia Commercial Joint Stock Bank - 1

(Source: Appendix 09 – T-test and ANOVA)

In which, the highest customer rating is currently the Marketing policy component (MAR) which is rated at 3.575; but the impact level of this factor on customer satisfaction according to the regression model is the lowest (5th) and the component rated lowest by customers is benefits (LOIICH) at 3.315. According to the regression model results, customers are most interested in the cost factor (CHPHI) but the rating level of this factor is low at 3.334. The remaining factors are also above the middle of the scale and there is not much difference. Thus, customers do not highly rate the factors that influence the decision to use credit cards at SCB.

(Source: Appendix 09 – T-test and ANOVA)

Figure 2.4: Graph showing the average values of the scales

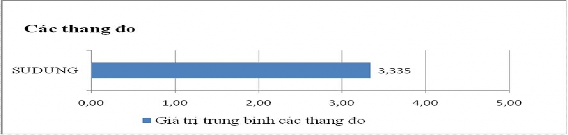

Similarly, using T-test to compare the mean value of the decision to use with the midpoint of the scale (No opinion = 3) to evaluate the ability of customers to decide to use the card, the results show that the ability of customers to use credit cards at SCB is not high, with the significance level Sig = 0.000. The mean score of the decision to use is 3.335 points, greater than the midpoint of the scale but has not reached the value of Agree = 4, showing that the ability of customers to decide to use credit cards at SCB is low.

Table 2.14: Mean values of the decision scale used

Mean parameter test

Test value = 3 | ||||

Factor | Average value | Statistics | Significance level | Standard deviation |

SUDUNG | 3,335 | 10,280 | 0.000 | 0.6350 |

(Source: Appendix 09 – T-test and ANOVA)

(Source: Appendix 09 – T-test and ANOVA)

Figure 2.5: Graph showing the average value of the decision scale used

Test for the difference between two population means (Independent sample T-test)

- Hypothesis H 11 : There is a difference between existing and non-existing customers of SCB in the decision to use credit cards at SCB.

Table 2.15: Independent sample T-test results

Group Statistics

SCB's customers | N | Mean | Std. Deviation | Std. Error Mean | |

SUDUNG | Are not | 90 | 3,2083 | ,64830 | ,06834 |

Have | 290 | 3,3741 | ,62677 | ,03681 |

Independent Samples Test

Levene's Test for Equality of Variances | t-test for Equality of Means | |||||||

F | Sig. | t | df | Sig. (2- tailed) | Mean Difference | Std. Error Difference | ||

SUDU NG | Equal variances assumed | 0.095 | ,758 | -2,175 | 378 | 0.030 | -,1658 | ,07625 |

Equal variances not assumed | -2,136 | 144,380 | 0.034 | -,1658 | ,07762 | |||

(Source: Appendix 09 – T-test and ANOVA)

The Sig result in Levene's test is 0.758>0.05, the variance between the two customer groups is not different, so we consider the next t-test result in the Equal variances assumed section. The Sig value in the t-test is 0.030<0.05; thus, hypothesis H 11 is accepted, meaning that there is a difference between existing customers of SCB and non-existing customers of SCB in the decision to use credit cards at SCB. In which, existing customers of SCB are more likely to decide to use credit cards at SCB (average value is 3.374 points).

- Hypothesis H 12 : There is a difference between men and women in the decision to use credit cards at SCB

Table 2.16: Independent sample T-test results

Group Statistics

Sex | N | Mean | Std. Deviation | Std. Error Mean | |

SUDUNG | Male | 149 | 3,3087 | ,60221 | ,04934 |

Female | 231 | 3,3517 | ,65602 | ,04316 |

Independent Samples Test

Levene's Test for Equality of Variances | t-test for Equality of Means | |||||||

F | Sig. | t | df | Sig. (2- tailed) | Mean Difference | Std. Error Difference | ||

SUDU NG | Equal variances assumed | 1,855 | ,174 | -,644 | 378 | ,520 | -,04301 | ,06677 |

Equal variances not assumed | -,656 | 334,989 | ,512 | -,04301 | ,06555 | |||

(Source: Appendix 09 – T-test and ANOVA)

The Sig result in Levene's test is 0.174 >0.05, the variance between the two genders is not different, so we consider the next t-test result in the Equal variances assumed section. The Sig value in the t-test is 0.520>0.05, so the hypothesis H 12 is rejected, meaning there is no difference between men and women in the decision to use credit cards at SCB.

One way ANOVA test

- Hypothesis H 13 : There is a difference in age, education, occupation and income in the decision to use credit cards at SCB.

Table 2.17: One way test - ANOVA

Variable group

calculate

Homogeneity of variance test | ANOVA | |||

Levene statistics | Sig. | F | Sig. | |

Age | 2,216 | 0.086 | 0.565 | 0.638 |

Level | 2,593 | 0.076 | 0.375 | 0.687 |

Job | 0.740 | 0.565 | 0.480 | 0.750 |

Income | 1,066 | 0.363 | 0.309 | 0.819 |

(Source: Appendix 09 – T-test and ANOVA)

According to Table 2.19 and Appendix 09, we see that the results of the homogeneity test for the qualitative variable groups of age, education, occupation and income are all insignificant (Sig. > 0.05). This result shows that the assumption of homogeneity of variance for these variable groups is accepted. Next, in the ANOVA test results for the variable groups of age, education, occupation and income, Sig. > 0.05, so we reject the hypothesis H 13, which means that there is no difference in the decision to use credit cards at SCB of customers classified by age, education, occupation and income.

2.2.3.5 Significance and conclusion of research model

This is the first applied study on the impact of factors influencing the decision to use credit cards at SCB. The study has identified a scale of important factors affecting customers in deciding to use credit cards at SCB, including 7 components with 29 observed variables. These are: Benefits (LOIICH), convenience (TTIEN), security (ATBM), ease of use (DESD), cost (CHIPHI), marketing policy (MAR) and bank image (HANH). The scale was tested to meet the requirements of value, reliability and suitability of the model.

However, the regression test results show that only 5 factors are accepted as statistically significant: Benefits (LOIICH), Convenience (TTIEN), Cost (CHIPHI), Marketing Policy (MAR) and Bank Image (HANH), corresponding to 5 accepted hypotheses: H 1, H 2, H 5, H 6, H 7. The regression model after adjustment is re-tested to be suitable for the characteristics of credit card services at SCB, bringing practical significance to the bank in the strategy of building credit card products and services and distributing them to the market. The study has tested the relationship between the decision to use and factors of product utility, service, price, marketing policy, bank image... the level of influence of each factor so that the bank has a suitable strategy with the purpose of increasing the rate of customers using card services at SCB. The factor that most strongly influences the decision to use a credit card at SCB is the cost factor (including credit card interest rates and service fees), followed by the benefit factor.

The study shows that the average value of customers' decision to use credit cards at SCB is 3.335 points, higher than the midpoint of the 5-point Likert scale but not high and has not reached the Agree value of 4 in the survey questionnaire. This shows that the possibility of customers using credit cards at SCB is not high, possibly because the policy features of SCB credit cards are not really attractive to customers. The rate of customers who decide to use (average value of 4 or more) is only 22.1%. The research results also show that the factor that most strongly affects the decision to use credit cards at SCB is the cost factor (including credit card interest rates and service fees), followed by the benefit factor when using credit cards.

The results of the model survey are relatively consistent with the theory of model building and analysis of the current situation in qualitative research. In theory and practice, the factors identified by the model all have an impact on customers' decision to use credit cards at SCB. At the same time, they are also factors that show the advantages and disadvantages of SCB's competitive advantage. However, some factors in theory and practice have an impact on the decision to use cards, but the survey results on the sample size of the study have not reached statistical significance, such as: ease of use and security.

The results of this study can also be extended to determine factors influencing customers' choice of other products and services such as payment cards, insurance services, online payment services, etc. However, when applying this study to different types of products and services, adjustments and additions are needed to suit the characteristics of each specific product and service.