Polatoglu & Ekin (2001)[140] investigated Turkish consumers' acceptance of e-banking services and found three attributes that have a strong influence on the quality of e-banking services: reliability, access, and savings.

In addition, Broderick & Vachirapornpuk (2002)[46], using data from 160 observations from 55 passages in documents posted by the e-banking community on bulletin boards, developed a model of perceived service quality in the e-banking sector. The authors identified the following five main criteria and considered them to have a fundamental influence on perceived service quality by customers: customer expectations of the service, bank image and reputation of the service provider, aspects of the service setup, actual difficulty of the service, and customer involvement. The authors also noted that among these criteria, the service setup and customer involvement criteria had the most direct impact on service evaluation.

Flavian, Tores & Guinaliu (2004)[76] found that four criteria, namely speed of service access, service provided, security, and bank reputation, were recognized to have built the image of e-banking and the quality of e-banking services.

Jayawardhena (2004)[94] identified four quality criteria such as website interface, trust, attention, and reliability using the modified SERVQUAL scale.

Yang and Fang (2004)[169] argue that traditional service quality criteria, such as competence, courtesy, cleanliness, comfort, and friendliness, are no longer relevant to online sales; whereas other criteria, such as reliability, responsibility, and assurance, are important for both traditional and e-service quality.

Similarly, Bauer & Hammerschmidt (2005)[33] proposed six criteria for the service quality of e-banking portals: security, reliability, additional services, added value, transaction support, and responsiveness.

In addition, Siu & Mou (2005)[152] adapted e-SERVQUAL to measure e-banking service quality in Hong Kong. The authors used factor analysis to identify four dimensions of reliability, ease of use, security, and troubleshooting. Among these four dimensions, the effectiveness was found to be similar to the original study of the e-SERVQUAL model, and the remaining dimensions were newly created.

Based on open-ended interviews, Maenpaa (2006)[117] reviewed a wide range of literature and quantitative analysis, developing seven dimensions of e-banking service quality: convenience, security, status, additional features, personal finance, investment, and exploration. The researcher further suggested that banks offering e-banking services need to focus more on the growing consumer group of young people, who are seen as promising for the future.

Pikkarainen et al. (2006)[139] focused on the performance of e-banking services based on a computer user satisfaction perspective. The authors argued that three criteria - content, ease of use, and accuracy - are a solid basis for measuring computer user satisfaction in e-banking. The authors concluded that there is a strong relationship between the criteria and overall satisfaction in e-banking.

Within the scope of the thesis, the author uses the concept of overall quality of e-banking services (Jun & Cai, 2001[100]; Yang et al., 2004[169]), this concept comprehensively evaluates the overall quality of e-banking services including three aspects: online customer service quality is measured by four attributes: tangible, reliability, responsiveness and understanding (Jun & Cai, 2001[100]); online information system quality (Jun & Cai, 2001[100]) is measured by ease of use, accuracy, security, content and aesthetics; banking service product quality (quantity of services, additional services, free utilities, functions necessary for customers, service features that customers need) (Jun & Cai, 2001[100], Yang et al., 2004[169]).

2.4. Customer satisfaction

Customer satisfaction is an important premise for creating customer loyalty. Satisfaction is the customer's response to the fulfillment of desires (Oliver, 1993)[142], is the customer's response to the difference between desires and the level of perception after using a product or service (Tse & Wilton, 1988)[160]. Satisfaction is a person's emotion, which is the joy or disappointment from comparing the results received from a product or service with their expectations (Kotler, 2000[82]; Jamal and Kamal, 2002[92]). Customer satisfaction is a psychological process of evaluating the results received compared to expectations (Egan, 2004)[68].

Customer satisfaction can lead to customer retention and thus profitability for an organization (Jamal & Kamal 2002[92]; Egan, 2004[68]).

According to Parasuraman et al. (2005)[136], there are some differences between service quality and customer satisfaction, the basic difference is the issue of "cause and effect". Meanwhile, Zeithalm (2001)[172] believes that customer satisfaction is affected by many factors: service quality, product quality, situational factors, price, personal factors.

Although there is a relationship between service quality and satisfaction (Cronin & Taylor, 1992[57]; Spreng & Makoy, 1996[156]), few studies have focused on examining the extent to which service quality dimensions explain satisfaction, especially for specific service industries (Lassar & associates, 2000[106]).

According to Gummerus et al. (2004)[85], customer satisfaction is positively correlated with loyalty in traditional services and is a measure of a firm's performance. In the online environment, satisfaction has a stronger impact on loyalty than in the real world, because searching for alternative providers is much more costly in the real world.

In Vietnam, satisfaction has been studied by a number of authors in different fields such as in education by Nguyen Thanh Long (2006) [15], Vu

Tri Toan (2007)[19]; in the banking sector by authors Le Van Huy (2007)[7], Hoang Xuan Bich Loan (2008)[3]; in the mobile telecommunications sector by authors Thai Thanh Ha and Ton Duc Sau (2007)[18]... Studies have also used original models from prestigious studies in the world to develop, clarify differences and apply in the context of Vietnam. Research by Hoang Xuan Bich Loan (2008)[3] in the banking sector uses the European model to evaluate expectations, perceived quality, value and satisfaction with: reliability, responsiveness, information accessibility and staff skills. Thai Thanh Ha and Ton Duc Sau (2007)[18] use Oliver's (1980)[131] "Expectation - Confirmation" theory to evaluate the level of satisfaction of customers using telecommunications services. The authors' research results have determined that the factors "customer perception of the call" have the strongest impact on satisfaction; other factors such as staff professionalism, registration location, etc. have weaker impacts. However, like other studies, this study does not analyze in depth the impact of factors in the correlation structure of satisfaction but only analyzes the impact of satisfaction on customer loyalty.

Oliver's (1980) expectancy-disconfirmation theory[131] is widely used in consumer behavior theory to study satisfaction, repeat behavior, and service marketing. The satisfaction model can be applied in B2C as well as B2B markets.

Nowadays, in the context of increasingly fierce competition, customer satisfaction can be considered as a significant success for businesses because customer satisfaction can lead to customer retention and bring profits to businesses.

In short, it can be defined: "Customer satisfaction is an emotional state in which customers' needs and expectations about the values/benefits of products and services are met, lower, equal or higher than expectations, leading to loyalty and repeat purchase behavior of the business's products and services" .

2.5. Customer loyalty

Loyalty is a term that is often used and abused. Despite its widespread use, the term has not been defined by authors, leading to a lack of uniformity in marketing theories. The common assumption is that loyalty can be translated into numerous repeat purchases from the same supplier over a period of time (Dick & Basu, 2001[64]).

Customer loyalty and profitability are closely related. Increased profits from customer loyalty result from reduced marketing costs, increased sales, and reduced operating costs because loyal customers are less likely to switch to another product when prices change and they tend to buy more than other customers (Reichheld & Sasser, 1990[143]; Fornell, 1992[75]).

There are three common approaches to studying customer loyalty: the attitudinal approach, the behavioral approach, and the mixed approach. The mixed approach takes into account both “behavioral” and “attitudinal” variables, to create its own concept of customer loyalty.

Loyal attitude

“Attitudinal loyalty” is the sum of customers’ preferences and purchase preferences that determine the level of loyalty (Egan, 2004[68]). “Attitudinal” loyal customers are less likely to accept negative brand information than other customers (Ahluwali et al., 1999[20]), are less motivated to seek alternative services even when they are disappointed (Dick and Basu, 2001)[64], and tend to quickly and aggressively promote positive service features, use additional services, and accept fair prices (Gremler and Brown 1999)[82].

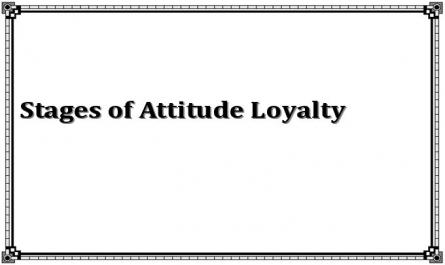

Some studies suggest that the attitudinal approach to loyalty consists of three parts: cognitive, emotional, and visceral. Cognitive loyalty is the first stage of the loyalty formation process and is based on beliefs or recent knowledge and experience, including product/service/price characteristics. Loyalty

The second stage of loyalty is emotional, characterized by emotional preferences for the product or service, represented by a positive association or attitude toward the brand, all of which can be derived from satisfaction: “I buy because I like it” (Oliver, 1993)[132]. The third stage is visceral loyalty, which is considered behavioral intention and characterized by repeat purchase behavior and specific brand commitment. In addition to the three attitudinal loyalty stages above, Oliver (1993)[132] points out the action loyalty stage. Customers have a desire to overcome obstacles to repeat purchase behavior of the product/service. Each stage of attitudinal loyalty is characterized by different repeat purchase behaviors:

Table 2.1: Stages of attitudinal loyalty

Stage 1 Awareness

Stage 2 Emotion | Stage 3 Instinct | Phase 4 Action | |

Accessibility, trust, centrality, clarity. | Emotions, moods, primary affects, satisfaction. | Transfer cost change, expect | Repeat buying behavior, overcoming barriers. |

Maybe you are interested!

-

Factors affecting customer loyalty to international payment services at Asia Commercial Joint Stock Bank - 12

Factors affecting customer loyalty to international payment services at Asia Commercial Joint Stock Bank - 12 -

Solutions to increase individual customer loyalty at Vietnam Joint Stock Commercial Bank for Industry and Trade by 2018 - 2

Solutions to increase individual customer loyalty at Vietnam Joint Stock Commercial Bank for Industry and Trade by 2018 - 2 -

Assessing the impact of brand equity on customer loyalty: an empirical study at BIDV Bank, Thua Thien Hue branch - 1

Assessing the impact of brand equity on customer loyalty: an empirical study at BIDV Bank, Thua Thien Hue branch - 1 -

Relationship marketing factors affecting customer loyalty to Vietnam Joint Stock Commercial Bank for Investment and Development in Ho Chi Minh City - 2

Relationship marketing factors affecting customer loyalty to Vietnam Joint Stock Commercial Bank for Investment and Development in Ho Chi Minh City - 2 -

Factors affecting customer loyalty to retail banking services at Dong A Commercial Joint Stock Bank, District 5 branch - 2

Factors affecting customer loyalty to retail banking services at Dong A Commercial Joint Stock Bank, District 5 branch - 2

Source: According to Oliver (1999)

Behavioral loyalty

“Loyalty behavior” is often reflected in the quantity of purchases, frequency of purchases, and switching to a brand (Allen and Meyer, 1990[23]; Oliver, 1993[132], Rauyruen & Miller, 2007)[142].

Tucker (1964)[161] argued that past repeat purchase behavior of a product/brand represents loyalty. Behavioral loyalty research focuses on patterns of repeat purchase behavior as an expression of loyalty. The three main components of behavioral measures include: rate, routine, and likelihood of purchase. Behavioral loyalty is viewed as repeat purchase behavior, based on purchase history (emphasizing past behavior rather than future behavior demonstrates that behavioral measures define brand loyalty within the context of purchase actions).

These measures are easier to collect than attitudinal measures. However, focusing solely on the behavioral part of loyalty may overestimate the actual part because some customers are compulsive about repurchasing a brand or using a distribution channel. Behavioral loyalty can be influenced by many factors, including product availability.

Mixed loyalty

Mixed loyalty reflects the strength of attitudes and the high or low level of behavior related to repeat purchases, according to which 4 scenarios can occur according to the matrix below:

Table 2.2: Attitude - repeat purchase behavior matrix

Repeat purchase behavior | |||

High | Short | ||

Attitude relate to | Strong | True loyalty | Latent Loyalty |

Weak | False loyalty | Unfaithful | |

Source: According to Dick & Basu (1994)

True loyalty: characterized by strong involvement and high repeat purchase behavior. This is the scenario most preferred by managers.

False loyalty: can lead to repeat purchase behavior despite negative attitudes. This scenario may be based on habit and is not related to positive attitudes. False loyalty is defined similarly to the concept of inertia. Customers can abandon a brand easily when they receive an alternative.

Latent loyalty: low repeat purchase behavior despite favorable attitudes. This scenario may be caused by intermediate factors such as distribution problems or high prices. If these barriers are removed, the purchase will occur. This is the concern of marketers.

Disloyal: customers have no preference or repeat purchase behavior for the product.

Thus, studies by scholars have approached the loyalty of

customer loyalty in three aspects: attitudinal loyalty, behavioral loyalty, and mixed loyalty. In which, mixed loyalty is ultimately a combination of attitudinal loyalty and behavioral loyalty. Customer loyalty can manifest in many different forms:

Attitudinal loyalty is often expressed in three forms: commitment, trust, and word of mouth:

Commitment: is a central concept in the development of relationship marketing. Commitment can be defined as a motive to continue to maintain a partnership. The concept originating from sociology suggests that commitment is a stable behavior of an individual even when he or she has other options (Becker, 1960)[36]. Therefore, commitment can affect the proportion of a brand in a product category in total purchases. Commitment is related to attitudinal loyalty and is defined as “a promise or personal commitment to one’s brand choice within a product category” (Lastovicka & Gardner, 1979)[107]. There are differences in the way high- and low-commitment customers approach information. For different brands, high-commitment customers tend to defend the brand when the brand is attacked (Burmkrant & Unnava, 2000)[26]. So it can be said that commitment is an expression of loyalty.

Trust: is a decisive factor for a successful relationship between parties and is considered a manifestation of loyalty. Rauyreuen (2007)[142] defines trust as the belief in a party's promise and will fully perform its obligations in an exchange relationship. Trust gives customers a sense of security when a partner meets their expectations. In order for customers to trust a company and thereby form a long-term relationship, customers must feel secure in their transactions with the company. Therefore, trust is the result of trust in a trustworthy party, in other words, to gain customer loyalty, a company must first gain their trust. Trust has a positive impact on loyalty.

Word of mouth : involves the process of transmitting information from customers' personal experiences with products and services. Word of mouth is an important factor.