assessment. Although this external source of information is often more diverse than internal sources of information, it is less reliable. Therefore, MB needs to have a reasonable plan to collect information from outside.

4.2.2. Complete the appraisal content

4.2.2.1. Cash flow statement analysis

Currently, to assess the financial situation of enterprises in general, banks have focused on analyzing the basic contents including: general assessment of financial situation through balance sheet, business performance report and analysis of financial criteria groups. Although the assessment content is relatively complete, to analyze and evaluate more clearly the financial situation of SMEs, the analysis of cash flow statement cannot be ignored.

Cash flow statement provides information about the cash flow of the business during the accounting period. Through the cash flow statement, CVTĐ will analyze the cash flow of the business.

Maybe you are interested!

-

Identify Rating Levels and Rating Scales

zt2i3t4l5ee

zt2a3gstourism,quan lan,quang ninh,ecology,ecotourism,minh chau,van don,geography,geographical basis,tourism development,science

zt2a3ge

zc2o3n4t5e6n7ts

of the islanders. Therefore, this indicator will be divided into two sub-indicators:

a1. Natural tourism attractiveness a2. Cultural tourism attractiveness

b. Tourist capacity

The two island communes in Quan Lan have different capacities to receive tourists. Minh Chau Commune is home to many standard hotels and resorts, attracting high-income domestic and international tourists. Meanwhile, Quan Lan Commune has many motels mainly built and operated by local people, so the scale and quality are not high, and will be suitable for ordinary tourists such as students.

c. Time of exploitation of Quan Lan Island Commune:

Quan Lan tourism is seasonal due to weather and climate conditions and festivals only take place on certain days of the year, specifically in spring. In Quan Lan commune, the period from April to June and from September to November is considered the best time to visit Quan Lan because the cultural tourism activities are mainly associated with festivals taking place during this time.

Minh Chau island commune:

Tourism exploitation time is all year round, because this is a place with a number of tourist attractions with diverse ecosystems such as Bai Tu Long National Park Research Center, Tram forest, Turtle Laying Beach, so besides coming to the beach for tourism and vacation in the summer, Minh Chau will attract research groups to come for tourism combined with research at other times of the year.

d. Sustainability

The sustainability of ecotourism sites in Quan Lan and Minh Chau communes depends on the sensitivity of the ecosystems to climate changes.

landscape. In general, these tourist destinations have a fairly high level of sustainability, because they are natural ecosystems, planned and protected. However, if a large number of tourists gather at certain times, it can exceed the carrying capacity and affect the sustainability of the environment (polluted beaches, damaged trees, animals moving away from their habitats, etc.), then the sustainability of the above ecosystems (natural ecosystems, human ecosystems) will also be affected and become less sustainable.

e. Location and accessibility

Both island communes have ports to take tourists to visit from Van Don wharf:

- Quan Lan – Van Don traffic route:

Phuc Thinh – Viet Anh high-speed boat and Quang Minh high-speed boat, depart at 8am and 2pm from Van Don to Quan Lan, and at 7am and 1pm from Quan Lan to Van Don. There are also wooden boats departing at 7am and 1pm.

- Van Don - Minh Chau traffic route:

Chung Huong high-speed train, Minh Chau train, morning 7:30 and afternoon 13:30 from Van Don to Minh Chau, morning 6:30 and afternoon 13:00 from Minh Chau to Van Don.

f. Infrastructure

Despite receiving investment attention, the issue of infrastructure and technical facilities for tourism on Quan Lan Island is still an issue that needs to be resolved because it has a direct impact on the implementation of ecotourism activities. The minimum conditions for serving tourists such as accommodation, electricity, water, communication, especially medical services, and security work need to be given top priority. Ecotourism spots in Minh Chau commune are assessed to have better infrastructure and technical facilities for tourism because there are quite complete and synchronous conditions for serving tourists, meeting many needs of domestic and foreign tourists.

3.2.1.4. Determine assessment levels and assessment scales

Corresponding to the levels of each criterion, the index is the score of those levels in the order of 4, 3, 2, 1 decreasing according to the standard of each level: very attractive (4), attractive (3), average (2), less attractive (1).

3.2.1.5. Determining the coefficients of the criteria

For the assessment of DLST in the two communes of Quan Lan and Minh Chau islands, the students added evaluation coefficients to show the importance of the criteria and indicators as follows:

Coefficient 3 with criteria: Attractiveness, Exploitation time. These are the 2 most important criteria for attracting tourists to tourism in general and eco-tourism in particular, so they have the highest coefficient.

Coefficient 2 with criteria: Capacity, Infrastructure, Location and accessibility . Because the assessment area is an island commune of Van Don district, the above criteria are selected by the author with appropriate coefficients at the average level.

Coefficient 1 with criteria: Sustainability. Quan Lan has natural and human-made ecotourism sites, with high biodiversity and little impact from local human factors. Most of the ecotourism sites are still wild, so they are highly sustainable.

3.2.1.6. Results of DLST assessment on Quan Lan island

a. Assessment of the potential for natural tourism development

For Minh Chau commune:

+ Natural tourism attractiveness is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined as average (2 points) and the coefficient is quite important (coefficient 2), then the score of Capacity criterion is 2 x 2 = 4.

+ Exploitation time is long (4 points), the most important coefficient (coefficient 3) so the score of the Exploitation time criterion is 4 x 3 = 12.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is assessed as good (3 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 3 x 2 = 6 points.

The total score for evaluating DLST in Minh Chau commune according to 6 evaluation criteria is determined as: 12 + 4 + 12 + 4 + 4 + 6 = 42 points

Similar assessment for Quan Lan commune, we have the following table:

Table 3.3: Assessment of the potential for natural ecotourism development in Quan Lan and Minh Chau communes

Attractiveness of self-tourismof course

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

CommuneMinh Chau

12

12

4

8

12

12

4

4

4

8

6

8

42/52

Quan CommuneLan

6

12

6

8

9

12

4

4

4

8

4

8

33/52

b. Assessment of the potential for humanistic tourism development

For Quan Lan commune:

+ The attractiveness of human tourism is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined to be large (3 points) and the coefficient is quite important (coefficient 2), then the score of the Capacity criterion is 3 x 2 = 6.

+ Mining time is average (3 points), the most important coefficient (coefficient 3) so the score of the Mining time criterion is 3 x 3 = 9.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points.

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is rated as average (2 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 2 x 2 = 4 points.

The total score for evaluating DLST in Quan Lan commune according to 6 evaluation criteria is determined as: 12 + 6 + 6 + 4 + 4 + 4 = 36 points.

Similar assessment with Minh Chau commune we have the following table:

Table 3.4: Assessment of the potential for developing humanistic eco-tourism in Quan Lan and Minh Chau communes

Attractiveness of human tourismliterature

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Quan CommuneLan

12

12

6

8

9

12

4

4

4

8

4

8

39/52

Minh CommuneChau

6

12

4

8

12

12

4

4

4

8

6

8

36/52

Basically, both Minh Chau and Quan Lan localities have quite favorable conditions for developing ecotourism. However, Quan Lan commune has more advantages to develop ecotourism in a humanistic direction, because this is an area with many famous historical relics such as Quan Lan Communal House, Quan Lan Pagoda, Temple worshiping the hero Tran Khanh Du, ... along with local festivals held annually such as the wind praying ceremony (March 15), Quan Lan festival (June 10-19); due to its location near the port and long exploitation time, the beaches in Quan Lan commune (especially Quan Lan beach) are no longer hygienic and clean to ensure the needs of tourists coming to relax and swim; this is also an area with many beautiful landscapes such as Got Beo wind pass, Ong Phong head, Voi Voi cave, but the ability to access these places is still very limited (dirt hill road, lots of gravel and rocks), especially during rainy and windy times; In addition, other natural resources such as mangrove forests and sea worms have not been really exploited for tourism purposes and ecotourism development. On the contrary, Minh Chau commune has more advantages in developing ecotourism in the direction of natural tourism, this is an area with diverse ecosystems such as at Rua De Beach, Bai Tu Long National Park Conservation Center...; Minh Chau beach is highly appreciated for its natural beauty and cleanliness, ranked in the top ten most beautiful beaches in Vietnam; Minh Chau commune is also home to Tram forest with a large area and a purity of up to 90%, suitable for building bridges through the forest (a very effective type of natural ecotourism currently applied by many countries) for tourists to sightsee, as well as for the purpose of studying and researching.

Figure 3.1: Thenmala Forest Bridge (India) Source: https://www.thenmalaecotourism.com/(August 21, 2019)

3.2.2. Using SWOT matrix to evaluate Quan Lan island tourism

General assessment of current tourism activities of Quan Lan island is shown through the following SWOT matrix:

Table 3.5: SWOT matrix evaluating tourism activities on Quan Lan island

Internal agent

Strengths- There is a lot of potential for tourism development, especially natural ecotourism and humanistic ecotourism.- The unskilled labor force is relatively abundant.- resource environmentunpolluted, still

Weaknesses- Poorly developed infrastructure, especially traffic routes to tourist destinations on the island.- The team of professional staff is still weak.- Tourism products in general

quite wild, originalintact

general and DLST in particularalone is monotonous.

External agents

Opportunity- Tourism is a key industry in the socio-economic development strategy of the province and Van Don economic zone.- Quan Lan was selected as a pilot area for eco-tourism development within the framework of the green growth project between Quang Ninh province and the Japanese organization JICA.- The flow of tourists and especially ecotourism in the world tends toincreasing

Challenge- Weather and climate change abnormally.- Competition in tourism products is increasingly fierce, especially with other localities in the province such as Ha Long, Mong Cai...- Awareness of tourists, especially domestic tourists, about ecotourism and nature conservation is not high.

Through summary analysis using SWOT matrix we see that:

To exploit strengths and take advantage of opportunities, it is necessary to:

- Diversify products and service types (build more tourism routes aimed at specific needs of tourists: experiential tourism immersed in nature, spiritual cultural tourism...)

- Effective exploitation of resources and differentiated products (natural resources and human resources)

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s3 { color: #0D0D0D; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -3pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -2pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -1pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s10 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s12 { color: black; font-family:Symbol, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s13 { color: black; font-family:Wingdings; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s14 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s16 { color: black; font-family:Cambria, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s17 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s18 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s19 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s20 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; } div.maincontent .s21 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 11pt; } div.maincontent .s22 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s23 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s24 { color: #212121; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex

Identify Rating Levels and Rating Scales

zt2i3t4l5ee

zt2a3gstourism,quan lan,quang ninh,ecology,ecotourism,minh chau,van don,geography,geographical basis,tourism development,science

zt2a3ge

zc2o3n4t5e6n7ts

of the islanders. Therefore, this indicator will be divided into two sub-indicators:

a1. Natural tourism attractiveness a2. Cultural tourism attractiveness

b. Tourist capacity

The two island communes in Quan Lan have different capacities to receive tourists. Minh Chau Commune is home to many standard hotels and resorts, attracting high-income domestic and international tourists. Meanwhile, Quan Lan Commune has many motels mainly built and operated by local people, so the scale and quality are not high, and will be suitable for ordinary tourists such as students.

c. Time of exploitation of Quan Lan Island Commune:

Quan Lan tourism is seasonal due to weather and climate conditions and festivals only take place on certain days of the year, specifically in spring. In Quan Lan commune, the period from April to June and from September to November is considered the best time to visit Quan Lan because the cultural tourism activities are mainly associated with festivals taking place during this time.

Minh Chau island commune:

Tourism exploitation time is all year round, because this is a place with a number of tourist attractions with diverse ecosystems such as Bai Tu Long National Park Research Center, Tram forest, Turtle Laying Beach, so besides coming to the beach for tourism and vacation in the summer, Minh Chau will attract research groups to come for tourism combined with research at other times of the year.

d. Sustainability

The sustainability of ecotourism sites in Quan Lan and Minh Chau communes depends on the sensitivity of the ecosystems to climate changes.

landscape. In general, these tourist destinations have a fairly high level of sustainability, because they are natural ecosystems, planned and protected. However, if a large number of tourists gather at certain times, it can exceed the carrying capacity and affect the sustainability of the environment (polluted beaches, damaged trees, animals moving away from their habitats, etc.), then the sustainability of the above ecosystems (natural ecosystems, human ecosystems) will also be affected and become less sustainable.

e. Location and accessibility

Both island communes have ports to take tourists to visit from Van Don wharf:

- Quan Lan – Van Don traffic route:

Phuc Thinh – Viet Anh high-speed boat and Quang Minh high-speed boat, depart at 8am and 2pm from Van Don to Quan Lan, and at 7am and 1pm from Quan Lan to Van Don. There are also wooden boats departing at 7am and 1pm.

- Van Don - Minh Chau traffic route:

Chung Huong high-speed train, Minh Chau train, morning 7:30 and afternoon 13:30 from Van Don to Minh Chau, morning 6:30 and afternoon 13:00 from Minh Chau to Van Don.

f. Infrastructure

Despite receiving investment attention, the issue of infrastructure and technical facilities for tourism on Quan Lan Island is still an issue that needs to be resolved because it has a direct impact on the implementation of ecotourism activities. The minimum conditions for serving tourists such as accommodation, electricity, water, communication, especially medical services, and security work need to be given top priority. Ecotourism spots in Minh Chau commune are assessed to have better infrastructure and technical facilities for tourism because there are quite complete and synchronous conditions for serving tourists, meeting many needs of domestic and foreign tourists.

3.2.1.4. Determine assessment levels and assessment scales

Corresponding to the levels of each criterion, the index is the score of those levels in the order of 4, 3, 2, 1 decreasing according to the standard of each level: very attractive (4), attractive (3), average (2), less attractive (1).

3.2.1.5. Determining the coefficients of the criteria

For the assessment of DLST in the two communes of Quan Lan and Minh Chau islands, the students added evaluation coefficients to show the importance of the criteria and indicators as follows:

Coefficient 3 with criteria: Attractiveness, Exploitation time. These are the 2 most important criteria for attracting tourists to tourism in general and eco-tourism in particular, so they have the highest coefficient.

Coefficient 2 with criteria: Capacity, Infrastructure, Location and accessibility . Because the assessment area is an island commune of Van Don district, the above criteria are selected by the author with appropriate coefficients at the average level.

Coefficient 1 with criteria: Sustainability. Quan Lan has natural and human-made ecotourism sites, with high biodiversity and little impact from local human factors. Most of the ecotourism sites are still wild, so they are highly sustainable.

3.2.1.6. Results of DLST assessment on Quan Lan island

a. Assessment of the potential for natural tourism development

For Minh Chau commune:

+ Natural tourism attractiveness is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined as average (2 points) and the coefficient is quite important (coefficient 2), then the score of Capacity criterion is 2 x 2 = 4.

+ Exploitation time is long (4 points), the most important coefficient (coefficient 3) so the score of the Exploitation time criterion is 4 x 3 = 12.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is assessed as good (3 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 3 x 2 = 6 points.

The total score for evaluating DLST in Minh Chau commune according to 6 evaluation criteria is determined as: 12 + 4 + 12 + 4 + 4 + 6 = 42 points

Similar assessment for Quan Lan commune, we have the following table:

Table 3.3: Assessment of the potential for natural ecotourism development in Quan Lan and Minh Chau communes

Attractiveness of self-tourismof course

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

CommuneMinh Chau

12

12

4

8

12

12

4

4

4

8

6

8

42/52

Quan CommuneLan

6

12

6

8

9

12

4

4

4

8

4

8

33/52

b. Assessment of the potential for humanistic tourism development

For Quan Lan commune:

+ The attractiveness of human tourism is determined to be very attractive (4 points) and the most important coefficient (coefficient 3), so the score of the Attractiveness criterion is 4 x 3 = 12.

+ Capacity is determined to be large (3 points) and the coefficient is quite important (coefficient 2), then the score of the Capacity criterion is 3 x 2 = 6.

+ Mining time is average (3 points), the most important coefficient (coefficient 3) so the score of the Mining time criterion is 3 x 3 = 9.

+ Sustainability is determined as sustainable (4 points), the important coefficient is the average coefficient (coefficient 1), so the score of the Sustainability criterion is 4 x 1 = 4 points.

+ Location and accessibility are determined to be quite favorable (2 points), the coefficient is quite important (coefficient 2), the criterion score is 2 x 2 = 4 points.

+ Infrastructure is rated as average (2 points), the coefficient is quite important (coefficient 2), then the score of the Infrastructure criterion is 2 x 2 = 4 points.

The total score for evaluating DLST in Quan Lan commune according to 6 evaluation criteria is determined as: 12 + 6 + 6 + 4 + 4 + 4 = 36 points.

Similar assessment with Minh Chau commune we have the following table:

Table 3.4: Assessment of the potential for developing humanistic eco-tourism in Quan Lan and Minh Chau communes

Attractiveness of human tourismliterature

Capacity

Mining time

Sustainability

Location and accessibility

Infrastructure

Result

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Point

DarkMulti

Quan CommuneLan

12

12

6

8

9

12

4

4

4

8

4

8

39/52

Minh CommuneChau

6

12

4

8

12

12

4

4

4

8

6

8

36/52

Basically, both Minh Chau and Quan Lan localities have quite favorable conditions for developing ecotourism. However, Quan Lan commune has more advantages to develop ecotourism in a humanistic direction, because this is an area with many famous historical relics such as Quan Lan Communal House, Quan Lan Pagoda, Temple worshiping the hero Tran Khanh Du, ... along with local festivals held annually such as the wind praying ceremony (March 15), Quan Lan festival (June 10-19); due to its location near the port and long exploitation time, the beaches in Quan Lan commune (especially Quan Lan beach) are no longer hygienic and clean to ensure the needs of tourists coming to relax and swim; this is also an area with many beautiful landscapes such as Got Beo wind pass, Ong Phong head, Voi Voi cave, but the ability to access these places is still very limited (dirt hill road, lots of gravel and rocks), especially during rainy and windy times; In addition, other natural resources such as mangrove forests and sea worms have not been really exploited for tourism purposes and ecotourism development. On the contrary, Minh Chau commune has more advantages in developing ecotourism in the direction of natural tourism, this is an area with diverse ecosystems such as at Rua De Beach, Bai Tu Long National Park Conservation Center...; Minh Chau beach is highly appreciated for its natural beauty and cleanliness, ranked in the top ten most beautiful beaches in Vietnam; Minh Chau commune is also home to Tram forest with a large area and a purity of up to 90%, suitable for building bridges through the forest (a very effective type of natural ecotourism currently applied by many countries) for tourists to sightsee, as well as for the purpose of studying and researching.

Figure 3.1: Thenmala Forest Bridge (India) Source: https://www.thenmalaecotourism.com/(August 21, 2019)

3.2.2. Using SWOT matrix to evaluate Quan Lan island tourism

General assessment of current tourism activities of Quan Lan island is shown through the following SWOT matrix:

Table 3.5: SWOT matrix evaluating tourism activities on Quan Lan island

Internal agent

Strengths- There is a lot of potential for tourism development, especially natural ecotourism and humanistic ecotourism.- The unskilled labor force is relatively abundant.- resource environmentunpolluted, still

Weaknesses- Poorly developed infrastructure, especially traffic routes to tourist destinations on the island.- The team of professional staff is still weak.- Tourism products in general

quite wild, originalintact

general and DLST in particularalone is monotonous.

External agents

Opportunity- Tourism is a key industry in the socio-economic development strategy of the province and Van Don economic zone.- Quan Lan was selected as a pilot area for eco-tourism development within the framework of the green growth project between Quang Ninh province and the Japanese organization JICA.- The flow of tourists and especially ecotourism in the world tends toincreasing

Challenge- Weather and climate change abnormally.- Competition in tourism products is increasingly fierce, especially with other localities in the province such as Ha Long, Mong Cai...- Awareness of tourists, especially domestic tourists, about ecotourism and nature conservation is not high.

Through summary analysis using SWOT matrix we see that:

To exploit strengths and take advantage of opportunities, it is necessary to:

- Diversify products and service types (build more tourism routes aimed at specific needs of tourists: experiential tourism immersed in nature, spiritual cultural tourism...)

- Effective exploitation of resources and differentiated products (natural resources and human resources)

div.maincontent .p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent p { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; margin:0pt; } div.maincontent .s1 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s2 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 13pt; } div.maincontent .s3 { color: #0D0D0D; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s4 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s5 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s6 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -3pt; } div.maincontent .s7 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -2pt; } div.maincontent .s8 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; vertical-align: -1pt; } div.maincontent .s9 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s10 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s11 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s12 { color: black; font-family:Symbol, serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s13 { color: black; font-family:Wingdings; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s14 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s15 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 9pt; vertical-align: 5pt; } div.maincontent .s16 { color: black; font-family:Cambria, serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s17 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 14pt; } div.maincontent .s18 { color: #080808; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s19 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s20 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 10pt; } div.maincontent .s21 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: bold; text-decoration: none; font-size: 11pt; } div.maincontent .s22 { color: black; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; text-decoration: none; font-size: 11pt; } div.maincontent .s23 { color: black; font-family:"Times New Roman", serif; font-style: italic; font-weight: normal; text-decoration: none; font-size: 14pt; } div.maincontent .s24 { color: #212121; font-family:"Times New Roman", serif; font-style: normal; font-weight: normal; tex -

Concept of Financial Capacity of Commercial Banks

Concept of Financial Capacity of Commercial Banks -

Criteria for Evaluating the Efficiency of Deposit Mobilization Activities of Commercial Banks

Criteria for Evaluating the Efficiency of Deposit Mobilization Activities of Commercial Banks -

Analysis of financial capacity and some solutions to improve financial capacity at Vietnam Telecommunications Technology Investment and Development Joint Stock Company - 5

Analysis of financial capacity and some solutions to improve financial capacity at Vietnam Telecommunications Technology Investment and Development Joint Stock Company - 5 -

Criteria for Evaluating Bad Debt Management of Commercial Banks

Criteria for Evaluating Bad Debt Management of Commercial Banks

The purpose of analyzing a business's cash flow statement is to help banks assess the sustainability of the business's past cash flow, its ability to generate cash, and the suitability of cash flow to the business's business strategy.

CVTĐ needs to assess the main sources of cash receipts and cash expenditures from business activities, investment activities or financial activities. The main sources of cash for a business can change according to its growth stage. The main source of cash is from business activities if the business is in the growth stage. If the net cash flow from business activities is negative, the business needs to borrow or issue shares to finance the shortfall. If the business has good business opportunities, the cash flow is used for investment activities. If the business is in the start-up or growth stage, the cash flow from business activities can be negative because of the need for investment to grow the business.

The content of the analysis of the business's cash flow statement is as follows:

Overview of cash flow statement analysis

+ Evaluate whether the business's net cash flow is positive or negative. In case the business's net cash flow is negative, CVTĐ needs to analyze carefully.

Person: The business is expanding its production and business activities or is really short of money, the business's ability to pay has problems.

+ The trend of a business's past net cash flow is stable, increasing or decreasing, which can indicate the ability to create idle money to expand operations.

+ Identify the basic sources of cash generation and cash use from the business's operations. A business's cash flow is considered good when the cash flow from operating activities is positive and covers enough capital costs.

Cash flow analysis must be placed in the context of the current and future business of the enterprise because sometimes high values reflect trouble rather than advantage. A business that is experiencing slow growth or a market downturn may have relatively strong cash flow because it has no need for fixed asset investment or short-term capital. Conversely, a business that is growing strongly may have negative cash flow because it needs to invest heavily to support growth. In this case, CVTD needs to assess the interplay between the positive side of positive cash flow and the risk that this positive level cannot be maintained in the future and vice versa, the negative side of negative cash flow as well as the good prospects that current investment activities will bring benefits and positive cash flow in the future for the enterprise.

The tasks that CVTĐ needs to perform when analyzing general cash flow include:

- Analysis of net cash flow from operating activities: CVTĐ determines the main components of net cash flow from operating activities. Analyze the reasons why net cash flow from operating activities is positive or negative. If it is negative, it may be due to reasons such as: the newly established business is in the development stage and needs investment money, due to losses in business activities, due to ineffective asset management, etc. If the cash flow from operating activities is negative, the business will have to use money from financial activities (borrowing or issuing additional capital) to make up for the shortfall. This is not always easy to do. If this situation persists, it shows that the business is having difficulty with payment issues, including debt repayment.

- Compare net cash flow from operating activities with pre-tax profit and net revenue to see if the trend is in the same direction or opposite direction over the years. If the trend is opposite, it may be due to the low quality of the business's revenue, poor ability to generate cash, and profits generated are only on the books.

- Analysis of net cash flow from investing activities: evaluates the business's asset purchases and cash investments. If the business is making large capital investments, it is necessary to consider which source of cash is used to offset (from operating activities or from financing activities).

- Analysis of net cash flow from financial activities: assess whether the enterprise has excess or shortage of cash, thereby assessing the capital mobilization policy (indirect mobilization from financial institutions through receiving loans and paying off loans, direct mobilization from owners through receiving contributed capital or returning contributed capital) and the enterprise's dividend payment policy.

Cash flow ratio analysis

In addition to the general analysis of the cash flow statement, banks should add some financial indicators based on the cash flow statement including:

Indicators reflecting performance :

The results of production and business activities viewed from the perspective of cash flow of the enterprise are related to the amount of money generated from the use of assets, equity or the amount of money generated with the level of revenue or profit. Specific ratios include:

(1) Cash flow to net revenue ratio: this criterion reflects how much net cash from operating activities is generated by each dollar of net revenue from sales and services during the period.

Cash flow to sales =

This ratio shows the ability of the company to generate cash from its revenue. A company's revenue is growing but its cash flow from operations is not growing is a sign of risk. Changes in the company's sales conditions or debt policy are reflected in this ratio.

(2) Cash flow to total assets ratio: this ratio shows how much each dong of assets in the period brings in on average from business activities.

Cash flow to total assets =

- Cash flow to equity ratio: this ratio measures the efficiency of equity in generating net cash from operating activities.

Cash flow to equity =

- Cash flow to net operating profit ratio: reflects the ability of operating activities to generate cash. Since net operating profit may include income from financial activities, this profit can be adjusted for income and expenses from financial activities.

Cash flow on net operating profit =

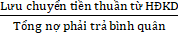

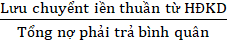

Ratios reflecting solvency:

- Debt coverage ratio: reflects the financial risk and financial leverage of the enterprise in general from the cash flow perspective. This ratio shows how much of the enterprise's debt is guaranteed to be paid by the amount of cash generated from operating activities.

Ability to pay =

- Current debt ratio: indicates the ability to pay short-term debt with cash flow from the business's operations. For companies in the manufacturing and trading sectors with healthy financial status, this ratio is usually equal to or greater than 40%.

Short-term debt repayment capacity =

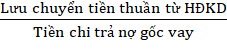

- Debt repayment capacity ratio: measures the ability to repay loans with cash from operating activities.

Ability to repay principal =

- Interest coverage ratio: the value of this ratio shows how many times the cash flow before tax and interest is greater than the interest payable by the business.

Ability to pay interest

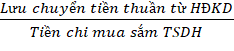

- Reinvestment capability ratio: indicates the ability to invest in long-term assets with cash from the business's operations. The higher this ratio is, the easier it is for the business to invest in purchasing fixed assets and other long-term assets. If this ratio is less than 1, the business must mobilize more money from financial activities for investment.

Reinvestment potential =

4.2.2.2. Notes when evaluating and analyzing some criteria

In analyzing the profitability of an enterprise, the coefficients showing the profitability such as ROA, ROE all use the entire profit before tax or profit after tax of the enterprise to calculate. If based only on pure numbers, this analysis sometimes does not tell the nature of the enterprise's profit generated from which activities, whether it is suitable for the development orientation of the enterprise and whether it is sustainable. In the current economic conditions, many SMEs operate in many industries. Sometimes there are times when businesses that are not the strength of the enterprise bring in large profits; for example, in the profit structure of a manufacturing enterprise, the profit from buying and selling raw materials accounts for a large proportion or a trading enterprise has a higher profit from securities trading than from traditional business activities... In essence, these sources of profit are unusual and unsustainable. Therefore, when analyzing and evaluating CVTĐ, it is necessary to clarify in order to be able to give more accurate results and predictions.

For SMEs that borrow capital and whose operations are seasonal and whose assets fluctuate greatly, calculating financial ratios based on average data calculated simply by averaging the beginning and end of the period (for example: average assets, average receivables, average inventories, etc.) will be very inaccurate and will not accurately reflect the business's operations. Therefore, for these businesses, through historical data and quick reporting data at many points in time, CVTĐ can determine a more accurate average figure. From there, the analysis results will more accurately reflect the financial situation of the business.

Although the profit after tax index on the income statement and the undistributed profit on the financial statement are closely related, they are not consistent because the income statement is of a period nature while the financial statement is of a point in time nature.

When considering the profit after tax/revenue (or profit after tax/equity), banks need to pay attention to additional factors that indirectly affect the profit after tax of SMEs to have a more accurate view of the financial strength of enterprises that have credit relationships with banks.

4.2.3. Completing the appraisal process

The appraisal process is a set of specific steps that guide the appraisal of business assets. Building a scientific and reasonable appraisal process will greatly support the appraisal staff, providing methodical, scientific and highly consistent analysis results throughout the system, while saving time and implementation costs.

Currently, the appraisal work at MB still depends heavily on the appraisers themselves and there is no high level of consistency among branches. Appraisers often passively wait until they receive the financial statements provided by the enterprise to conduct the appraisal or periodically re-appraise but only as a formality and not in a systematic and detailed manner, leading to untimely analysis and outdated results, not keeping up with the developments of the enterprise, and the appraisal results are of little value.

MB needs to quickly develop a specific and detailed process for appraising NLTC of SMEs borrowing capital from banks across the system as a basis for guidance.

for officers to perform appraisal tasks. The process has specific regulations on corporate financial appraisal as follows:

- Regulations on the periodic time for conducting appraisal: should be once every 3 months to keep up with and grasp changes in the financial situation of the borrowing enterprise as well as the continuous fluctuations of the business environment to make decisions on granting credit or deciding on appropriate credit adjustment.

- Regulations on the time to start the appraisal: the time to start the appraisal should not be applied when receiving the financial statements of the enterprise as it is now, but the time should be clearly specified, it should be 2 months after the end of the fiscal year for 1-year reports and 1 month for 6-month reports. In case the enterprise does not have official settlement data or is waiting for audit/approval results from superiors, it can temporarily use the express report for appraisal. When there are approval, audit results or official data, adjustments and additional analysis can be made.

- Specific regulations on analysis objectives, implementation steps, implementation time, appraisal content and responsibilities of officers participating in appraisal. These must be specified in criteria, list of questions to ask businesses, specific forms to calculate... to apply consistently. When the appraisal of NLTC for SMEs borrowing capital has been specifically carried out according to a unified process, the results achieved will certainly be more scientific, systematic and accurate.

4.2.4. Perfecting the organization of appraisal work

Strengthening the analysis and evaluation of enterprises is an important factor that directly determines the success of the appraisal results of NLTC of enterprises borrowing capital from banks. Therefore, MB needs to soon have solutions to overcome the shortcomings in the implementation of this work to facilitate the work of CVTĐ, thereby improving the quality of appraisal of NLTC of enterprises.

First, specialize business management by industry, by business field, by loan term and by stages of the credit process.

The fact that CVTĐ is having to carry out all stages of the customer appraisal process except for the appraisal of fixed assets at the branches is very disadvantageous for MB because currently

SMEs account for a large proportion of banks' loan portfolios, and these enterprises operate in a variety of industries and sectors with their own advantages, difficulties, and levels of accuracy and complexity of financial statements. Even a competent CVTĐ cannot have a deep understanding of all sectors. Therefore, in order for appraisal work to be highly effective, it is necessary to assign staff in a specialized direction.

Assign CVTĐ by industry and field of activity

First, to implement this solution, MB needs to compile statistics on all types of businesses that MB has credit relationships with. Then, classify them by industry such as: agriculture, industry, trade, services. These large industries are divided into smaller business groups such as garment, footwear, transportation, construction, etc. For each type or group of SMEs, MB will assign a group of CVTĐ to directly manage depending on the size of the business. If assigned according to this model, CVTĐ will understand the business situation as well as the development trend of the type of business they are in charge of, and know more about the regulations, policies, and priorities of the State and locality for that industry. This not only facilitates CVTĐ in the process of appraising businesses, improving the quality of analysis and evaluation of businesses, but also facilitates managers in managing the status of each loan.

Assign CVTĐ according to the term of each loan

Assigning the term of each loan is very necessary because short, medium and long-term loans have different levels of complexity. Long-term loans are often used to implement investment projects with very long durations, sometimes up to decades, so the level of potential risk complexity is very high. This requires CVTĐ to have many years of experience, with good sensitivity to be able to anticipate unusual fluctuations that can be detrimental to the project during implementation, thereby minimizing risks for MB. Therefore, MB needs to assign good and experienced staff to manage medium and long-term loans, while young staff with not really solid professional qualifications will take on short-term loans to implement business plans or installment credit. With this solution, MB will take advantage of