The branch classified debts in accordance with the regulations of the State Bank; increased risk provisions, and handled and recovered nearly VND 7,000 billion of bad debts for VAMC.

In 2018, Vietnam Joint Stock Commercial Bank for Industry and Trade still had VND13,426 billion in special bonds issued by VAMC, of which VND2,230 billion had been set aside as a provision. The number of special bonds at the end of 2018 was 5.4 times higher than at the end of 2017. Previously, according to the semi-annual audited financial statements of 2018, by the end of June 2018, the bank no longer held any special bonds issued by VAMC. At the end of 2018, the total bad debt on the balance sheet at Vietnam Joint Stock Commercial Bank for Industry and Trade was VND13,691 billion, an increase of 53% compared to the beginning of the year.

Treatment by DPRRTD

Among the above measures, the most used measure is handling with the DPRRTD fund. This measure accounts for 73% of the total measures applied by the Vietnam Joint Stock Commercial Bank for Industry and Trade.

The funds set aside for DPRR can only be used in the following cases: (1) the customer is an organization or enterprise that is dissolved or bankrupt according to the provisions of law; an individual dies or goes missing; (2) the debts have been classified as bad debts in the "potentially lost" group. For debts that are frozen pending the Government's settlement, the bank can use the reserve to handle RRTD.

The principle of using DPRR to handle debt is: DPRR of each debt is used to handle that debt, auctioning off collateral to collect debt. After using DPRR to handle debt, the bank continues to monitor debt collection in the "off-balance sheet" account. After having enough documents proving that all debt collection measures have been used but without results, and must be approved by the Ministry of Finance and the State Bank to use DPRR.

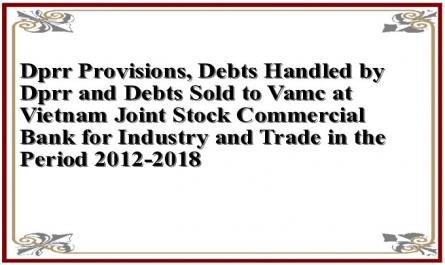

Table 3.12 Provisions for bad debts, Debts handled by bad debts and Debts sold to VAMC at Vietnam Joint Stock Commercial Bank for Industry and Trade in the period 2012-2018

Target

Provision for contingency funds (billion VND) | Bad debt (on balance sheet) (billion VND) | DPRR provision/Bad debt (NX coverage ratio) (%) | Bad debt ratio (on balance sheet) (%) | Debt is paid off by DPRR and sold to VAMC (billion VND) VND) | |

2012 | 4,229 | 4,890 | 86.48 | 1.47 | 20,868 |

2013 | 4.203 | 3,770 | 111.49 | 1.00 | 26,378 |

2014 | 3,931 | 4,905 | 80.14 | 1.12 | 30,351 |

2015 | 3.241 | 4,942 | 65.58 | 0.92 | 37,406 |

2016 | 3.019 | 6,741 | 44.78 | 1.02 | 40,514 |

2017 | 3,614 | 9.011 | 40.10 | 1.14 | 46,809 |

2018 | 4,960 | 13,690 | 36.23 | 1.58 | 13,426 |

Maybe you are interested!

-

Perfecting the Operations of Asset Management Companies of Vietnamese Credit Institutions to Promote the Purchase and Handling of Bad Debts

Perfecting the Operations of Asset Management Companies of Vietnamese Credit Institutions to Promote the Purchase and Handling of Bad Debts -

Handling of Civil Debts of Private Business Owners and Partners in Partnership Companies

Handling of Civil Debts of Private Business Owners and Partners in Partnership Companies -

Status of Provisioning and Using Credit Risk Provisions

Status of Provisioning and Using Credit Risk Provisions -

Table Showing the Ratio of Dprr/Total Bad Debt of Branches in the Period 2012 - 2014

Table Showing the Ratio of Dprr/Total Bad Debt of Branches in the Period 2012 - 2014 -

Concept, Characteristics, Role of Securitization of Bad Debts of Commercial Banks

Concept, Characteristics, Role of Securitization of Bad Debts of Commercial Banks

(Source: Financial and management report of Vietnam Joint Stock Commercial Bank for Industry and Trade

period 2012-2018)

Table 3.12 shows that the provision for provisioning and the bad debt on the balance sheet of Vietnam Joint Stock Commercial Bank for Industry and Trade in the period of 2012-2018 were relatively stable. However, in 2016 and 2017, the provision for provisioning decreased compared to previous years, and in 2018 it was 4,960 billion VND (an increase of 1.36% compared to 2017), while the bad debt on the balance sheet all fluctuated and increased, in 2017 it was 9,011 billion VND, especially in 2018 it increased dramatically to 13,690 billion VND. Therefore, the coverage ratio of bad debt on the balance sheet in the years 2012-2018 almost tended to decrease, less than 100% value, the biggest decrease was in 2018 reaching 1.85%. This shows that from 2012 to 2018, for every 100 VND of bad debt on the balance sheet, the bank's provision for risk loss was reduced. (In 2015, for every 100 VND of bad debt on the balance sheet, the bank set aside 65.58 VND of risk loss; in 2016, for every 100 VND of bad debt on the balance sheet, the bank set aside 44.78 VND of risk loss; in 2017, for every 100 VND of bad debt on the balance sheet, the bank set aside 40.10 VND of risk loss, but in 2018, for every 1 VND of bad debt on the balance sheet, the bank set aside 36.23 VND of risk loss). Thus, the level of risk loss provision of the bank is increasingly reduced to the level of safety for the bank's capital fluctuations.

In addition, the debt handled by DPRR and debt sold to VAMC in the period 2012-2017 increased, even in 2017 it was approximately double that of 2012, however the bad debt ratio including XLDP debt and debt sold to VAMC was quite stable, fluctuating around 5.59% to 6.55%. In 2018, the Bank still had 13,426 billion VND of special bonds issued by VAMC, of which 2,230 billion VND had been provisioned. The number of special bonds at the end of 2018 was 5.4 times higher than at the end of 2017. Previously, according to the semi-annual audited financial statements of 2018, by the end of June 2018, the Bank no longer held any special bonds issued by VAMC. At the end of 2018, the total bad debt on the balance sheet at the bank was 13,691 billion VND, an increase of 53% compared to the beginning of the year.

In addition, Vietnam Joint Stock Commercial Bank for Industry and Trade also implements the following debt settlement measures (based on the actual situation of the borrower):

Solution 1: Hire an external debt collection service:

Applicable in cases where hiring an external debt collection service is more effective than the bank's own debt collection.

Conditions of application: The Bank shall only employ an external debt collection service in cases where it is deemed necessary and more effective than conventional debt collection such as: urging and coordinating with customers to sell assets, requesting the handover of assets, filing a lawsuit, etc., but the debt has not/cannot be recovered, and the debt processing time is prolonged. Therefore, it is necessary to choose a debt collection option through a debt collection service.

For debts in group 2, the Branch submits to TSC for approval the implementation of debt collection services, in accordance with actual conditions and situations.

For bad debts, XLRR debts, debts sold to VAMC: Branches shall hire debt collection services according to the Bank's authority at each period.

Measure 2: File a lawsuit

Vietnam Joint Stock Commercial Bank for Industry and Trade files a lawsuit in Court in case the creditor's rights and legitimate interests of the bank are violated:

+ Customers with bad debt, debt that has been processed and recorded off-balance sheet at the bank and are determined to have a source of debt repayment (source from collateral and other sources) but intentionally delay and do not cooperate in repaying the bank;

+ Customers do not acknowledge their debt to the bank; customers show signs of fraud; abscond; individuals die or go missing with assets but the related obligated person does not cooperate in paying the bank debt;

+ Customers have many creditors disputing assets and income;

+ Other cases where the Bank deems it necessary to initiate a lawsuit.

Measure 3: Request to open bankruptcy proceedings for the enterprise

Vietnam Joint Stock Commercial Bank for Industry and Trade requests to open bankruptcy proceedings for enterprises in the following cases:

+ Businesses with prolonged losses and no longer able to recover;

+ Measures have been applied but the debt cannot be recovered due to the business's prolonged losses;

+ Debt without collateral;

+ The order, procedures and documents for requesting enterprise bankruptcy are implemented according to the Regulations.

bankruptcy law

Measure 4: Request the State and Government to provide resources for debt settlement or debt cancellation

Vietnam Joint Stock Commercial Bank for Industry and Trade requests the State and Government to provide resources for debt settlement or debt cancellation in the following cases: Based on the subjects and approval of the Government and the State Bank of Vietnam on supporting resources for off-balance sheet debt settlement or debt cancellation for one or several customers with outstanding debt at the bank, in accordance with the subjects considered by the State Bank of Vietnam, submit to the Government for resources for debt settlement or debt cancellation.

Measure 5: Debt cancellation/debt settlement XLRR

Vietnam Joint Stock Commercial Bank for Industry and Trade shall write off/discharge bad debts in the following cases: Debts for which the Bank has used provisions for bad debts are being recorded in off-balance sheet accounts for a minimum period of 05 years or more and for which the Bank has taken all measures to recover the debt but has not been able to recover.

3.3.3.3 Current status of inspection, supervision and handling of violations

Inspection, supervision and violation handling work is carried out regularly and continuously by Vietnam Joint Stock Commercial Bank for Industry and Trade through specific activities in 2018 as follows:

- Inspect and supervise the business operations of the Joint Stock Commercial Bank for Industry and Trade.

Vietnam Trade, implementation of the Resolution of the General Meeting of Shareholders:

Through internal management reports of Vietnam Joint Stock Commercial Bank for Industry and Trade

and independent reports of members of the inspection and supervision board have carried out inspection and supervision on a regular and continuous basis. On a monthly or ad hoc basis, representatives of the inspection and supervision board have attended all meetings of the Board of Directors and meetings of the Executive Board to grasp information, exchange, discuss, and present independent opinions on the shortcomings, limitations, and risks in the operations of the Vietnam Joint Stock Commercial Bank for Industry and Trade and specific recommendations to the Board of Directors and the General Director.

- Review policy documents, consider Resolutions/Decisions of

Board of Directors, General Director:

The Inspection and Supervision Board reviews internal policy documents issued by the Board of Directors and the General Director, reviews the Resolutions/Decisions of the Board of Directors through internal reports, conducts internal inspections from the results of monitoring activities, and conducts periodic or ad hoc internal audits. Through review and consideration, it is found that the documents, policies, and Resolutions/Decisions of the Board of Directors and the General Director are basically in accordance with the provisions of law and the Charter of Vietnam Joint Stock Commercial Bank for Industry and Trade.

- Review monitoring reports and audit reports of the Internal Audit Department:

Based on periodic internal audit reports and reports on the results of each internal audit at units in the system, issues discovered through audits, recommendations and proposals of the internal audit department are all reviewed, evaluated and included in the report sent to the Board of Directors at regular meetings in 2018 and included in the written recommendation/proposal sent directly to the Chairman of the Board of Directors and the General Director.

- Monitor the implementation of the restructuring plan associated with bad debt settlement:

In 2018, implementing the direction of the State Bank, the Board of Directors and the Executive Board of Vietnam Joint Stock Commercial Bank for Industry and Trade completed and submitted to the State Bank the Restructuring Plan associated with bad debt settlement for the period 2016-2020. On November 27, 2018, the Governor of the State Bank issued Decision No. 2337/QD-NHNN approving a number of contents on the objectives, solutions and roadmap for implementing the Restructuring Plan associated with bad debt settlement for the period 2016-2020 of Vietnam Joint Stock Commercial Bank for Industry and Trade (Decision No. 2337) and on December 15, 2018. The Board of Directors of Vietnam Joint Stock Commercial Bank for Industry and Trade issued Resolution No. 456/NQ-HDB-HNCT44 (Resolution 456) approving the specific implementation plan of the Bank and in December 2018, the Bank immediately carried out a number of tasks related to bad debt settlement solutions for a number of large customers in accordance with the approved Plan.

As of December 31, 2018, based on Decision 2337 and Resolution 456, Vietnam Joint Stock Commercial Bank for Industry and Trade has basically implemented the requirements on solutions and implementation roadmap set out for 2018 of the Restructuring Plan associated with bad debt settlement. (Report on the performance results of the Board of Supervisors of Vietinbank in 2018)

3.3.3.4 Current status of reporting on bad debt management results at Vietnam Joint Stock Commercial Bank for Industry and Trade

Vietnam Joint Stock Commercial Bank for Industry and Trade builds an information and reporting system to serve bad debt management activities, ensuring that bad debt management activities have a complete database to serve comprehensive and effective management requirements and meet the bank's bad debt management requirements.

As soon as bad debt is identified based on the collected data, depending on the nature, level of bad debt and the Bank's hierarchy at each time, the unit that generates bad debt and/or the Management Board of bad debt prepares a report on bad debt. The purpose of these reports is to assess the impact of bad debt and propose solutions to minimize it for the Bank.

Periodically (at least monthly, annually) and when necessary, the bad debt control department prepares and sends directly a written report on bad debt to the members of the Board of Directors, the Board of Members, the Supervisory Board and the Board of General Directors. The current status of preparing the Bad Debt Management Results Report at the Bank complies with the State Bank's Report. In addition to basing on the overdue debt repayment period of over 90 days, bad debt identification can be recognized through quantitative and qualitative signs ( see Appendix 5 ) to assess the likelihood of risk and the customer's ability to repay.

The report on bad debt management results includes: General report on bad debt management results; Report and evaluation of bad debt management results (including some basic indicators: Total outstanding credit balance as of the end of the year; Bad debt ratio at the increasing, decreasing level and ensuring compliance with regulations; Overdue debt ratio on total outstanding debt; Minimum capital safety ratio as of the end of the year, compared to the prescribed level). Each bank branch prepares a report on bad debt management results on time and not later than the bank's regulations.

3.4 Assessment of the current status of bad debt management of Vietnam Joint Stock Commercial Bank for Industry and Trade

3.4.1 Achievements and causes

3.4.1.1 Results achieved

The bad debt management activities of Vietnam Joint Stock Commercial Bank for Industry and Trade in the period of 2012-2018 have had positive changes in all aspects. Bad debt management is carried out based on specific and detailed documents. Bank staff strictly implement the regulations and rules in bad debt management, which is demonstrated by the fact that the bank has almost no violations in bad debt management. In addition, the activities of controlling and preventing bad debt, measuring and classifying bad debt are also actively implemented by the bank and in accordance with the process.

* On the development and promulgation of policies, strategies for bad debt management and bad debt management processes

Develop and issue policies, strategies and procedures for credit risk management

In general, QLNX in particular is increasingly improved. 96.92% (63/65 votes) rated it as very good (According to the results of in-depth interviews - in content 2 - question number 2, appendix 4)

Decision No. 215/2017/QD-HDQT-NHCT dated March 15, 2017 "Decision promulgating the Regulation on credit approval authority in the system of Vietnam Joint Stock Commercial Bank for Industry and Trade" is built on the basis of applying Circular 39/2016/TT-NHNN on Regulations on lending activities of credit institutions and foreign bank branches to customers with the goal of ensuring strictness in the credit granting process of the bank.

Decision No. 506/2014/QD-HĐQT -NHCT35, issued on May 27, 2014, regulating the classification of assets, the level of provision, the method of provisioning for risk management and the use of provisions to handle risks in the operations of the Vietnam Joint Stock Commercial Bank for Industry and Trade, is built on the Basel II foundation and smoothly combines Circular 02/2013/TT-NHNN, Circular 09/2014/TT-NHNN dated March 18, 2014 on amending and supplementing a number of articles of Circular 02/2013/TT-NHNN. Decision No. 506/2014/QD-HĐQT -NHCT35 aims to ensure that the classification of provisions is scientific and accurate, avoiding the situation of "misplacing arising debts".

The NH's policy document system is catching up with international practice when it is issued and built at 5 levels: (i) Overall policy framework, (ii) Specific policies, (iii) Directive documents, instructions for policy implementation, (iv) General implementation process, (v) Detailed process for each product to ensure the overall consistency and effectiveness of the policy document system.

In late 2017-2018, Vietnam Joint Stock Commercial Bank for Industry and Trade continued to build a risk-weighted asset (RWA) calculation system that meets the methodological requirements on data structure, algorithms and risk-weighted asset calculation methods according to Circular 41/2016/TT-NHNN.

In addition, banks share experiences in integrated risk management and internal capital adequacy assessment (ICAAP), operational risk management... at seminars organized by the State Bank, the Banking Association or proactively implemented by banks.

By the end of 2017-2018, Vietnam Joint Stock Commercial Bank for Industry and Trade was ready to meet the capital calculation methodology for key risks including: Credit risk, operational risk and market risk. In addition, the method of measuring and managing liquidity risk and interest rate risk on the bank book according to international practices and in accordance with the State Bank has been applied to date.

*About the organizational model of bad debt management apparatus

The advantages in the new organizational model of the State Bank of Vietnam according to Decision No. 20/NHNN will create an important premise to continue innovating inspection and supervision activities towards getting closer to international practices and standards and in accordance with reality.

Development of the banking industry in the new period.

The organizational model of the bad debt management apparatus of Vietnam Joint Stock Commercial Bank for Industry and Trade is increasingly perfect . 95.38% (62/65 votes) rated it as very effective (According to the results of in-depth interviews - in content 3 - question number 3, appendix 4).

The bank's credit risk management model in the period 2012-2018 according to the centralized model was built closely following and in line with international practices and in line with the development of the Vietnamese banking system and Vietnam Joint Stock Commercial Bank for Industry and Trade.

Vietnam Joint Stock Commercial Bank for Industry and Trade has always been proactive in researching to innovate and create in the process of applying Basel II standards to bad debt management activities and has initially succeeded in its governance structure when the Bank researched and completed the project of the 3-ring control model according to international practices.

In the third quarter of 2015, Vietnam Joint Stock Commercial Bank for Industry and Trade has performed well in its governance and management. From there, clearly separating responsibilities for risk management (QLRR) between the rings; enhancing overall strength in QLRR, especially QLNX from the transaction level to the entire governance framework; minimizing dispersion in risk data; ensuring control of all key areas of the bank. Accordingly, QLNX work is proactively carried out by the bank with close coordination from QLNX units in 3 rings, from the establishment, monitoring to proactive identification of key risks that have been deployed by the bank, helping to provide appropriate QLNX solutions.

One of the successes in developing the QLNX solution at Vietnam Joint Stock Commercial Bank for Industry and Trade is the construction of the Risk Profile Management System. This system helps identify the scope and level of risk to have appropriate control measures and action plans. At the end of 2018, Vietnam Joint Stock Commercial Bank for Industry and Trade continued to build the Risk-Weighted Asset (RWA) Calculation System to meet the methodological requirements on data structure, algorithms and methods of calculating risk-weighed assets according to Circular 41/2016/TT-NHNN.

The focus of risk management and bad debt management in the next phase of Vietnam Joint Stock Commercial Bank for Industry and Trade is to complete the Basel II program according to the bank's plan and apply it to management and operations. In particular, the important goal is to complete the items to comply with Circular No. 41/2016/TT-NHNN, dated December 30, 2016, regulating capital safety ratios for banks and foreign bank branches.

Vietnam Joint Stock Commercial Bank for Industry and Trade has applied a new credit risk management model according to Decision 808/2018/QD-HDQT-NHCT9 dated December 28, 2018 of Vietnam Joint Stock Commercial Bank for Industry and Trade.

Vietnam Joint Stock Commercial Bank for Industry and Trade has applied ICAAP to evaluate risk-adjusted performance and will apply it in the coming time, fully preparing.

conditions to ensure the Basel II implementation roadmap is consistent with the requirements of the State Bank. Basel II requires high quantitative requirements on minimum capital to be complied with to help banks have enough tolerance for all types of risks.

Vietnam Joint Stock Commercial Bank for Industry and Trade has successfully built and applied an internal credit rating system as a foundation for credit granting activities based on quantifying all qualitative and quantitative factors of customers. This is also one of the important points to be noted in the process of converting the management model according to Basel II.

* On the organization of bad debt management activities.

The credit risk management activities of Vietnam Joint Stock Commercial Bank for Industry and Trade have been implemented synchronously throughout the system and have had clear changes. 93.84% (61/65 votes) assessed the implementation of credit risk management activities through measurement as quite good (According to the results of in-depth interviews - in content 4 - question 4, appendix 4). Specifically, measurement through: Internal credit rating system, measurement indicators, risk warning; Credit risk early warning system; Automatic debt reminder system; Debt classification system; Internal credit rating indicator set according to Basel II standards; Debt classification system according to regulations of the State Bank of Vietnam;

Risk management has been promoted and implemented synchronously throughout the system and has had remarkable changes. Promoting the effectiveness of the 3-line protection model, ensuring business activities are in the right direction, safe and in compliance with legal regulations. The task of the Bank is to help popularize the culture of risk management, raise awareness of compliance throughout the system, and fully prepare the conditions to ensure the Basel II implementation roadmap is in line with the requirements of the State Bank. Therefore, Vietnam Joint Stock Commercial Bank for Industry and Trade has gradually approached both qualitative and quantitative debt classification.

- Control and prevention

Through the results of expert interviews on control activities and reporting of QLNX at Vietnam Joint Stock Commercial Bank for Industry and Trade, 92.3% (60/65 votes) said that the Bank has performed this control role relatively well (according to the results of expert interviews - in content 5 - question number 5, appendix 4).

Vietnam Joint Stock Commercial Bank for Industry and Trade has formed the habit of forecasting debts that are likely to turn bad to be more proactive in credit approval and credit treatment for customers on this list. The industry reporting system has been operating stably as a tool to support the system's portfolio management and credit granting.

Vietnam Joint Stock Commercial Bank for Industry and Trade has upgraded and enhanced the capacity of its internal inspection and audit apparatus. Accordingly, it has centralized and consolidated the internal inspection department at the Head Office, and established internal inspection points in regions nationwide.